Page Contents

| BASIS | SECTION 194Q | SECTION 206C(1H) |

| OBLIGATION | BUYER | SELLER |

| TURNOVER LIMIT TO DETERMINE APPLICABILITY | PREVIOUS YEAR TURNOVER/ GROSS RECEIPTS OF BUYER EXCEEDS 1 0CR | PREVIOUS YEAR TURNOVER/ GROSS RECEIPTS OF SELLER EXCEEDS 10CR |

| EFFECTIVE DATE | 1ST JULY, 2021 | 1ST OCTOBER 2020 |

| THRESHOLD LIMIT | PURCHASE IN EXCESS OF 50 LACS FROM EACH SELLER DURING THE YEAR | SALE IN EXCESS OF 50 LACS TO EACH BUYER DURING THE YEAR |

| TIME OF DEDUCTION/ COLLECTION | BILL OR PAYMENT WHICHEVER IS EARLIER | AT THE TIME OF RECEIPT |

| PRESCRIBED RATE | 0.10% | 0.10% |

| HIGHER RATE WHERE PAN IS NOT AVAILABLE | 5% | 5% |

| RETURN FORM | 26Q | 27EQ |

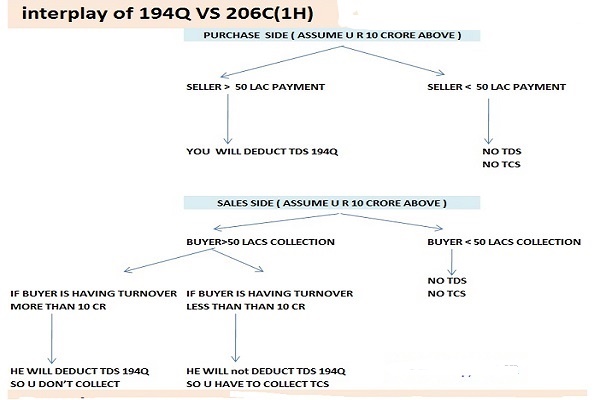

In case, a transaction falls within the ambit of both the sections- 194Q and 206C(1H), the following treatment be done –

| SITUATION | TDS/ TCS APPLICABLE PROVISION |

| TURNOVER IN PRECEDING FY BUYER >10 CR, SELLER<10CR | 194Q: BUYER TO DEDUCT TDS |

| TURNOVER IN PRECEDING FY BUYER <10 CR, SELLER>10CR | 206C(1H): SELLER TO COLLECT TCS |

| TURNOVER IN PRECEDING FY BUYER >10 CR, SELLER>10CR | 194Q: BUYER TO DEDUCT TDS |

| TURNOVER IN PRECEDING FY BUYER <10 CR, SELLER<10CR | NOTHING APPLICABLE |

| ADVANCE PAID BY BUYER ON OR AFTER 1ST JULY 2021 | 194Q WILL BE APPLICABLE AS TRIGGER POINT FOR 1 94Q IS EARLIER OF PAYMENT OR CREDIT OF SUCH SUM TO THE SELLER |

| ADVANCE PAID BY BUYER ON OR BEFORE 30TH JUNE 2021 | SELLER WILL COLLECT TCS ON SUCH TRANSACTION U/S 206C(1H), SINC THE TRIGGER POINT FOR DEDUCTION OF TDS IS PAYMENT OR CREDIT WHICHEVER IS EARLIER. THUS, TDS DEDUCTED U/S 194Q SHALL NOT BE APPLICABLE WHERE PAYMENTS ARE MADE BEFORE 30TH JUNE 2021. |

Before the introduction of sections 194Q and 206C(1H), sales and purchases of products were out of the purview of TDS/ TCS. However, now Form 26 AS is further audit evidence to verify/ confirm the numerous revenues and buy of products transactions.

Under clause 34a of the shape 3CD, where auditor is required to investigate overall TDS/ TCS compliances by the assessee, detailed reconciliation may need to run for these newly added sections.

In case of non-compliances with the provisions of these sections, disallowances, interest and penalty will be welcomes by the taxpayer.

Auditors are required to diligently consider the identical for creation of provision for taxes within the books of account and also for the calculation of income tax liability and its consequent impacts in deferred taxes.

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}