Page Contents

The existing COVID-19 pandemic affects not only public health but also the financial system as a whole. Public safety measures in place, although necessary are a huge hit to the economy’s liquidity flow leading to serious problems such as unemployment, a failure of the supply chain, a sudden drop in demand, unavailable inventories, etc.

The government provides various relief and relaxation measures to boost businesses and the economy. In the same sense, the MCA has postponed from FY 2019-20 to FY 2020-21 the applicability of the Companies (Auditor’s Report) Order, 2020 [CARO 2020].

The Statutory auditor’s report (CARO 2020) shall include the following statement on the below matters, which are mentioned below:

In cases where the answer given by the Statutory auditor to any of the above requirements is unfavorable or negative, The auditor’s report shall then also set out the basis for such unfavorable or qualified response.

In addition, in cases in which the auditor is unable to give an opinion on any defined issue, the report shall state such fact together with the purposes why the auditor can not give an opinion on the same.

To improve the scope of the audit, the CARO 2020 was published by the MCA in consultation with the NFRA. It contains a list of topics that the relevant companies are obliged to report on.

CARO 2020 applies to all St. Audits beginning on or after 1 April 2020 which relates to the financial year 2019-20. The order applies to all companies covered under CARO 2016. Accordingly, the order requires all companies except the following companies which have been expressly prohibited from their jurisdiction:

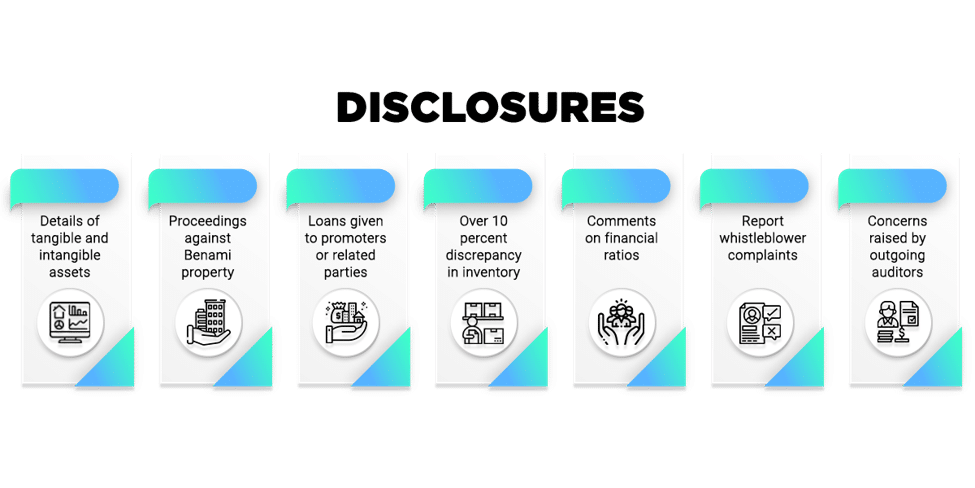

Reporting over maintenance of records of Intangible assets has been specifically added.

Leased Immovable property is specifically excluded from the reporting over the holding of title deeds in the Company’s name. If owned Immovable property is not held in the Company’s name, Dispute status and details of the registered owner need to be reported.

In the case of EPP revaluation, the auditor must determine that the same has been achieved on the basis of the Reported Interest survey. Changes ought to be recorded if 10% or more of the adjustments are made in the WDV.

Inconsistencies recognized by management with an effect of 10% or more of the inventory value need to be reported.

In the case that the Corporation has a working capital limit of more than INR 5 Crores depending on the security of the current assets (e.g. Stock, Debtors), the auditor must report that the regular filings (e.g. Financial Accounts, Debtors Listing) made with the lender are in compliance with the books.

The auditor must disclose whether or not any income has been returned under the Income Tax Act, 1961 and the same has been duly accounted for in the books of accounts.

The auditor must determine that the company is considered to be a “Willful defaulter.”

Information on the removal of term loans from allowable use needs to be published.

Data has been given on how short-term loans have been used for long-term purposes.

The auditor must comment on all money taken to meet the commitments of the community business.

Reporting on loans received by the Firm was made on the basis of the commitment of shares issued by the Firm to shareholders, Joint ventures, and associates.

Fraud reporting has been extended to fraud against the Company by any person rather than by officers or employees in the past.

The fraud report issued by the auditors in the form of ADT-4 to CG should be reported.

The auditor has to record his evaluation of “Whistle Blower” allegations.

The auditor must report whether the internal audit system exists within the company and whether or not the internal audit reports have been considered.

The particulars of the proceedings (pending/initiated) under the Benami Law need to be published.

Details of consolidated companies with qualifications or adverse reactions in the CARO report must be reported along with the Paragraph Number of the auditor with the audit report on Consolidated Financial Activities.

The auditor must report on the conduct of financial activities of an NBFC nature by the company without valid Certificates and reporting.

The auditor will document whether the Company has suffered CASH LOSS during the current AND preceding financial year and the volume of such cash loss.

The resignation of the statutory auditor and the causes, problems with him duly considered by the incoming auditor or not; must be published.

The goals of the Organization to meet its Existing Obligations on the basis of percentages, maturity and plans for execution must be stated.

The Auditor will disclose that the unexpended amount has been allocated to the designated fund within 6 months of the end of the fiscal year and whether or not the pending project balance has been moved to a special account. (Amendment itself under the Corporations Act, not yet told in 2013).

Popular blog:-

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

HRA Exemption under Old Tax Regime: New Rules Effective from 1 April 2026 Salaried Employees & HRA: New Rules Effective… Read More

{kind=link}

{kind=link}

{kind=link}