Page Contents

Basic key takeaways things Regarding Form 26QB: TDS relates to the sale of real estate/property according to the Finance Bill of 2013, where the cost of sale is equal to or greater than Rs 50,00,000.

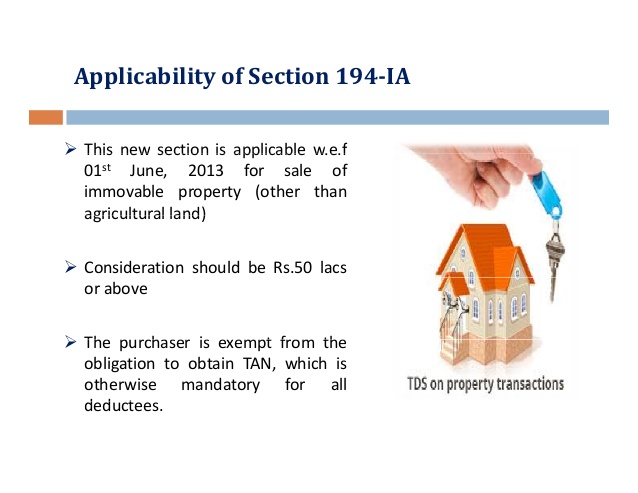

Section 194 IA of the Income Tax Act, 1961, provides that, as of 1 June 2013, the buyer can deduct tax at 1 % when making the property payment on the purchase of real estate immovable property.

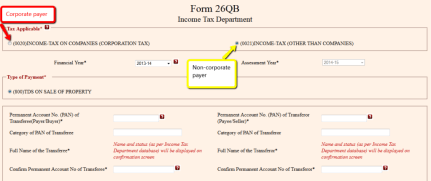

The seller will receive Form 16B for the deducted payment of TDS, while the buyer has to obtain Form 26QB as per the Income tax Act 1961.

The section of this Act deals primarily with transactions concerning the sale of immovable property, and the relevant TDS along with Form 26QB must be submitted within 30 days which are counted from the end of the month in which TDS was deducted.

For Example, if the financial transaction took place on March 14th then Form 26QB must be submitted Compulsory by April 30th of that year.

Tax Law Provide and laid down several primary regulations for selling and purchasing real estate property.

In each and every that transaction covered by Section 194-IA, if such financial transaction value is greater than Rs. 50 lakhs, the buyer, also known as the deductor, is allowed to deduct TDS.

Deductor (purchaser) under this section 194IA will be required to issue to the deductee (seller) Form 16B.

The person buying the property must deduct TDS from the overall selling valuation at the rate of 1 percent. A significant point to remember is that the purchaser, not the other party, has to subtract the TDS.

TDS shall not be deducted where the sale value is less than Rs. 50,00,000. In this event, if payment is in installments, TDS would have to be deducted from each payment.

The tax applies to the entire sum of the sale-even if the buyer or seller is more than one.

With effect from the FY 2013-14 budget, the 1 % TDS Rate deduction regulation on property sales was introduced to inspect underhanded property deals.

With effect from June 2013, the regulation stipulates that on the sale of property exceeding Rs. 50 lakhs in India, a 1 percent tax on the total sale consideration must be deducted before making the payment to the vendor.

All the specifications for Form 26QB are provided under Section 194-IA.

These are:

Points should be Buyer of Property identify:

Points should be Seller of Property identify:

Provide your PAN to the Department of Income Tax for the collection of TDS details to the Purchaser.

Check your Form 26AS Annual Tax Statement for the deduction of taxes deducted by the Buyer.

Information needed for Challan26QB:

The following details are needed when filling out the form 26QB) for Full Challan 26QB.

Related Articles

Understanding Form 16, Form 16A & Form 26AS: A Complete Guide for Taxpayers When filing your Income Tax Return (ITR),… Read More

CFO Cum whole-time director? ROC Gwalior Says No in EKI Energy Services Case Corporate governance is built on the principle… Read More

Toughest Exams in India: More Than a Test of Knowledge, A Test of Character Every year, millions of students and… Read More

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}