Page Contents

Under the GST regime, business owners whose turnover exceeds Rs. 40 lakhs* (Rs. 10 lakhs for NE and hill states) are required to be registered as a normal taxable person. This registration procedure is termed the GST registration process.

Registration under the GST is compulsory for only certain companies. If the organisation sells its goods without registration under the GST, it will be an offense under the GST and severe penalties will apply.

Registration of GST typically takes approximately 2-6 business days. We’re going to help you register for GST in 3 easy steps.

*CBIC reported an increase in the threshold turnover from Rs 20 lakhs to Rs 40 lakhs. The notification shall come into force on 1 April 2019.

Goods and Services Tax (GST) Registration Services at Rajput jain and Associates helps you register your GST company and get your GSTIN.

RJA help via GST Experts will guide you on the applicability & Compliance of your corporate with GST but will register your company with GST.

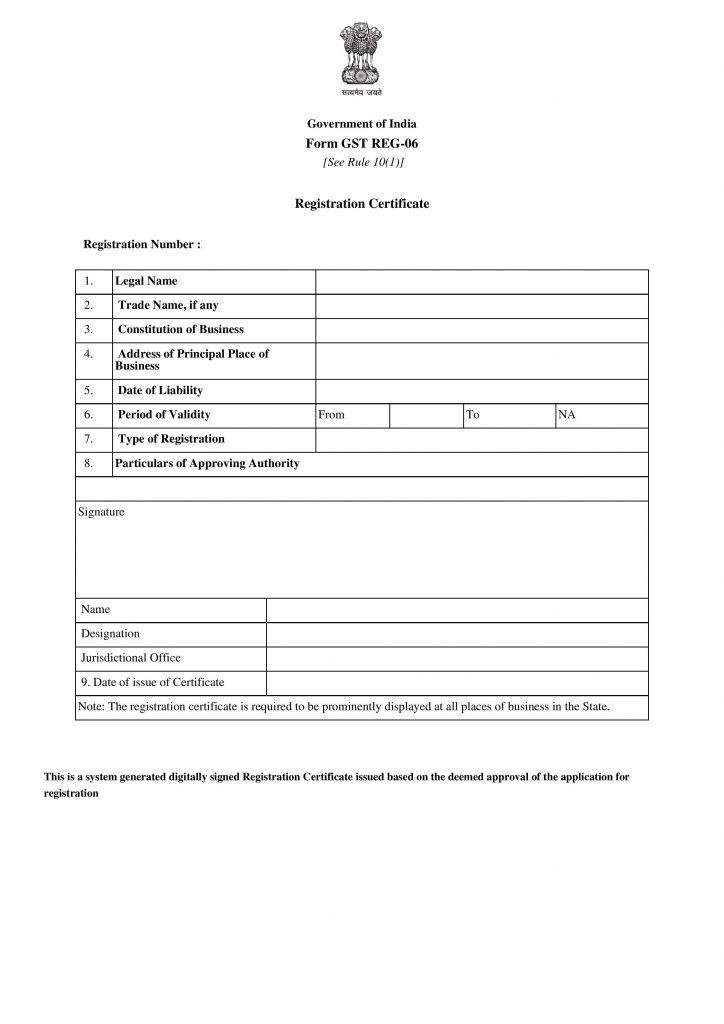

No, without login it cannot be acquired. But you can follow the following steps to easily download your GST certificate if you have login details The download of the GST Registration Certificate will take place step by step here.

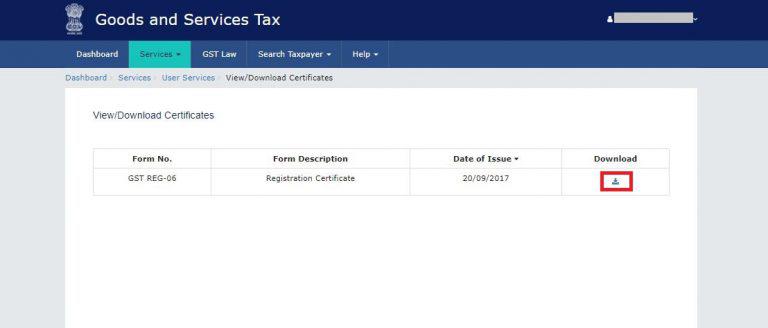

Step-by-step Process for downloading the GST Registration Certificate:

Step 1-GST Portal login.

Step 2-Go to ‘Services’ > ‘User Services’ > ‘Certificate view/download.

Step 3-Click on the icon ‘Download’

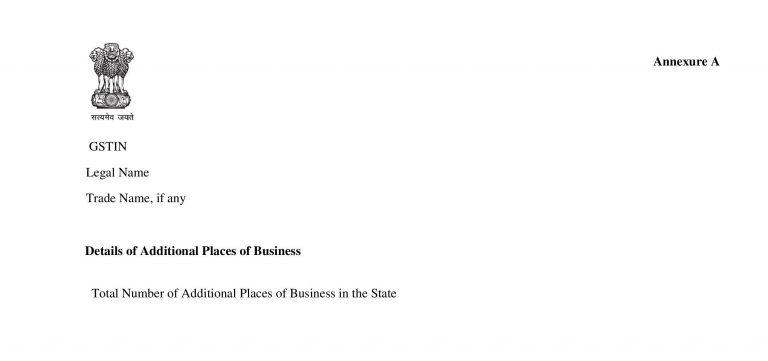

another second page is ‘Annexure A’ which provided details of any other additional place of business of the Firm.

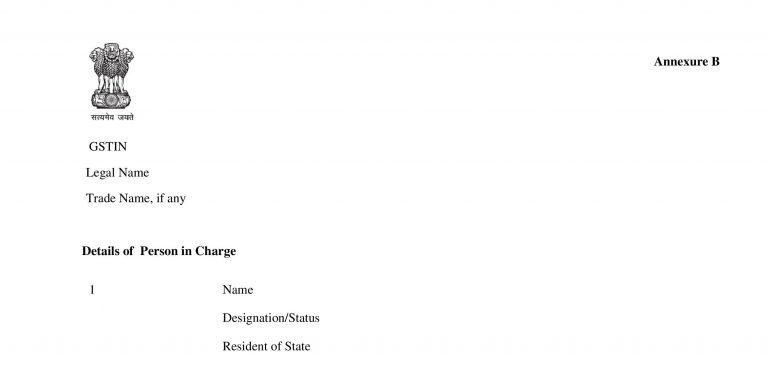

The last and third page as attached in ‘Annexure B’ has details of the person-in-charge of the business.

An offender who does not pay tax or make short payments (genuine errors) must pay a penalty of 10% of the amount of tax due, subject to a minimum of Rs.10,000.

The following seven days will be quite a challenging Phase in Rajya Sabha as GST Bill is in the critical stage as it is proposed to implement GST in April 2017.

There are several reasons which had prevented the passing of the GST Bill in the upper house. Out of these some factors were the political agendas which were hidden and other visible factors can be best understood from analyzing the following demands of the Congress Party which is right now the single largest party in the upper house.

India moved a step further to implement the GST when the government agreed on Wednesday to reduce the contentious 1% tax on manufacturing and wholly compensate the states for 5 years for all potential losses suffered after new system comes into force.

There were 3 demands of the congress party:

The government already has given its consent to 2 demands:

On the other hand, the government is not giving consent to consider the third demand to include a ceiling limit of 18% in the GST rate as it says this rate cannot be easily incorporated in the constitution.

After conducting various meetings for around a decade, by the collective efforts of experts, various organizations, and committees led by Dr. Aravind Subramanian, it was agreed to settle with RNR (Revenue Neutral Rate) the rate between 17% to 18%.

It was duly recommended by making a provision of 1% Entry tax but here the petroleum sector was outside the scope of RNR.

Revenue Neutral Rate refers to the single rate which helps in preserving the revenue at desired levels. It is that single rate that slowly gets converted into full-rate structure depending on various exemptions allowed by different policy choices made. It decides what commodities are to to be charged at a lower rate and what commodities with a higher rate.

The RNR can be clearly differentiated from the “standard rate” which is proposed to be given in the GSThttps://carajput.com/gst/gst-consultancy.php Regime which is applied to all the services and goods whose taxation policy is not clearly defined in any act or law. So, typically most if the goods and services are taxed at a standard rate,although it may be noted that it need not be a thumb rule (compulsory rule) to charge a standard rate.

So basically RNR is that rate where both state government and the central government will incur loss from the viewpoint of collection of taxes in order to earn revenue.

Popular updates:

FOR FURTHER QUERIES CONTACT US:

E: singh@carajput.com 9-555-555-480

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}