Page Contents

Moreover, in the Budget Exemptions to rule due to the amendments made in the Income-tax Act, 1961, which stipulates the below person will not be exempted from the penalty

Submit the ITR dues also ensure that interest payable on the income tax refund is calculated from April 1 of the relevant AY. In the case of belated filings, the individual loses out on some amount of interest.

“In view of the continued challenges faced by taxpayers in meeting statutory compliances due to outbreak of COVID-19, the government further extends the dates for various compliances,” said the CBDT in a statement.

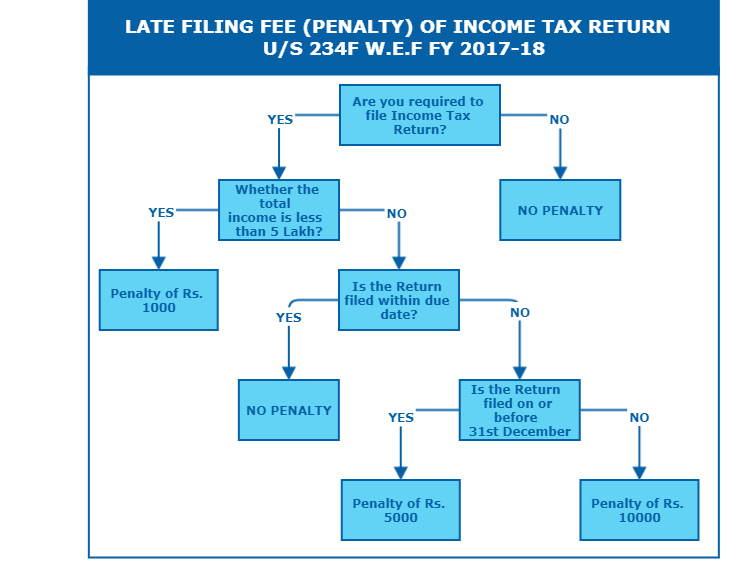

| Applicable Late Filing Fee Details as per section 234F | ||

| E- Income tac Filing Date | Total income Below INR 5 lakhs | Total income Above INR 5 lakhs |

| Up to 31st August 2020 | Rs 0 | Rs 0 |

| Between 1st September 2020 to 31st December 20 | Rs 1,000 | Rs 5,000 |

| Between 1st January 21 to 31st March 21 | Rs 1,000 | Rs 10,000 |

| ITR 1 (SAHAJ) | Individuals with Salary & interest Income only |

| ITR 2 | Individuals and HUF not having income from business/profession |

| ITR 3 | Individuals/ Hindu Undivided Families being partners in firms & not carrying out business or profession under any proprietorship |

| ITR 4 | Individuals & Hindu Undivided Families having a proprietary business or profession income |

| ITR 4S (SUGAM) | Individuals or Hindu Undivided Families having presumptive business Income |

| ITR-5 | In order for AOP & BOI, LLP, & Partnership firms to report their income and tax computation. |

| ITR-6 | Co that are registered in India use this form. |

| ITR-7 | In case entities are claiming an exemption as colleges, scientific research institutions, political parties or universities, and religious or charitable trusts, this form must be used. |

| Installments | Rate of Advance Tax | Total Liability/due under advance Tax |

|---|---|---|

| First Installments | 15 % | 4,80,000*15%= 72,000 |

| Second Installments | 45% | 4,80,000*45%= 2,16,000 |

| Third Installments | 75% | 4,80,000*75%= 3,60,000 |

| Fourth Installments | 100% | 4,80,000*100%= 4,80,000 |

three kinds of Interest payable u/s 234 as below mention hereunder :

Tax returns for AY2023-24 (The FY 2022-23 ) were original to be filed by July 31.

Please Note – All taxpayers opting for old tax regime in AY 2024-25 need to file Form 10IEA before due date of ITR Filing

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}