Income Tax Act requires that any payments made by a resident to a non-resident be disclosed and required to provide 15CA & 15CB Certificate in India.

The objective of deducting taxes at source and reporting them afterward is to ensure that taxes are collected in a timely manner. Form 15CA is a declaration submitted by the person remitting the money, stating that any payments made to the non-resident have been taxed.

Form 15CB, on the other hand, is a certificate given by a Chartered Accountant certifying that the provisions of the Double Taxation Avoidance Agreement and the Income Tax Act were followed in regard to tax deductions while making payments. It contains the following items:

Payment details and nature made to a non-resident.

Section 195 of the Income Tax Act must be followed.

The Double Taxation Avoidance Agreement’s applicability.

Rate of TDS deducted.

Generally, 15CA CB is not necessary to make a payment abroad in the event that costs fall below the defined limit. That’s because you’re a member of the Remittee. In the case of rent charged to NRIs / foreign vendors, Pursuant to Section 195 of the Income Tax Act 1961,

Why Form 15CA and Form 15CB :

any person liable for making a payment to non-residents shall subtract TDS at the rates in place from the payments rendered or credits granted to non-residents.

RBI also requires that, with the exception of such personal remittances that have been expressly removed, no remittances should be rendered to a non-resident without sending an undertaking in Form 15CA followed by an accountant’s certificate in Form 15CB, Remember that this is

Individuals making payments for bills/invoices must apply Form 15CA to the income tax portal each time before paying for the excess of expenses.

In fact, if the cumulative amount to be made each year reaches Rs 5 lakh, the Remitter must receive Form 15CB from the Chartered Accountant.

When you make a payment to a foreign seller, it is your duty to figure out if the Remittee is an NRI. This makes it easier for you to subtract TDS for the invoice to be received and to comply with the Income Tax Act.

Aim of this undertaking and credential is to raise taxes as the remittance is made because it will not be practicable for the non-residents to reclaim the tax at a later date.

The format of the undertaking to be registered electronically in Form 15CA and the format of the Accountant’s certificate in Form 15CB were notified vide Rule 37BB of the Income Tax Rules 1962

Forms 15CA and 15CB are of considerable interest nowadays. We professionals at least have to issue one Form 15CB on a routine basis and the 15CA form is also to be generated on behalf of the professional. Form 15CA is a Remitter Certification that is used as a method for collecting data about transfers that are taxable in the hands of non-resident users.

Authorized Dealers / Banks are now becoming more cautious in ensuring that all these Forms are collected by them before they are remitted, as now, in accordance with the revised Rule 37BB,

they are expected to file Form 15CA obtained from the remitter, with the income tax authority for any proceedings under the Income Tax Act and also with the revised FEMA Guidelines released. In this regard, as per the updated RBI Guidelines,

The latest guidelines to register electronic forms 15CA and 15CB are valid as of 1 April 2016. The comprehensive procedure for filing the form as per requirement is focused on new laws that follow.

The income tax department has updated the rules governing the preparation and delivery of Form 15CA and Form 15CB (see previous Form 15CB regulations). As of 1 April 2016, updated rules became applicable.

It begins with an effective information retrieval program that the Income Tax Department will use to track foreign remittances separately and their existence to assess tax liability.

The mechanism for picking cases for scrutiny has dramatically deteriorated in modern times and without an inspection, there was no test to ensure that taxable foreign remittances were made after-tax deduction or not. So the remittance path, i.e. Banks were led to acquiring Form 15CA and Form 15CB before allowing any remittance.

RBI does not provide guidelines on the deduction of tax on international remittances at the source. The banks, therefore, encourage remitters to have these Type 15CA and 15CB even while buying imports.

Here’s an effort to render a detailed checklist/procedure for furnishing Form 15CA and Form 15CB effectively.

1 lakh penalty will apply for each non-filing default for 15CA / CB certification

Major changes in the FORM –

Form 15CA and 15CB shall NOT be needed to be submitted by a person for remittance which does not require RBI approval

List of payments of a defined nature referred to in Rule 37BB, which do not require the submission of Form 15CA and Form 15CB, has been extended from 28 to 33 including import payments

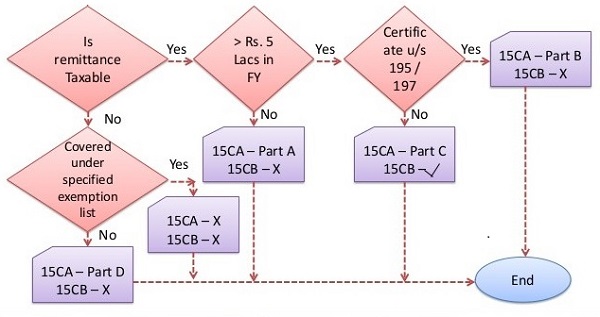

Form No. 15CB will only be needed for non-resident payments that are taxable and surpass Rs. 5 lakhs.

www.carajput.com; certificate 15ca 15 CB

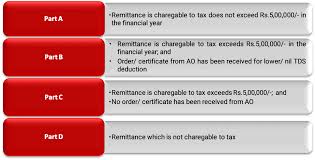

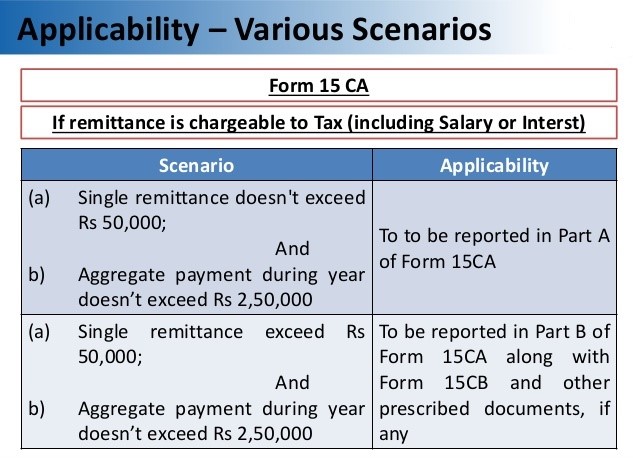

Only Part A of 15CA is required when the volume of payment or the number of these payments made during the financial year does not exceed five lakh rupees

Part B of 15CA to be filled in the event of receiving a certificate from the Assessing Officer pursuant to section 197 or an order from the Assessing Officer pursuant to subsection (2) or subsection (3) of section 195. For example, Form 15CB is not necessary if an order or certificate is obtained from AO

Part C of 15CA may be filled out after a Chartered Accountant obtains a certificate in Form No. 15CB

Part D of Type No.15CA where there is some amount not paid under the terms of the Act. For eg, Form 15CB is not needed if the remittance is not taxable

Step by step Process to File Form 15CA and 15CB all online summation with effect from April 1, 2016

We are used to helping our clients in transferring funds from India to out of India after Satisfy the sources and taxability of the fund, below four Steps for procedures which are needed to follow:

www.carajput.com; Applicability of Form 15ca 15 CB

Obtain Chartered Accountant (CA) Certificate in Form 15CB – CA must verifying (though his own procedures) the source is determining the sources of funds is the TDS is properly deducted on such source,

Submit Form 15CA online,

Needed to Submit documents to Bank where NRE accounts kept

Form 15CA

Check (cheque) or Demand Draft for the amount

Form 15CB

Request letter or Form as per respective bank’s requirement

Complete any other document, requirement, or formality

Transfer:On verification of submitted documents, Bank will process the transfer and credit the NRE account.

permanent account number availability of the remitter

Complete Main place of business of the remitter

The E-Mail address and phone no. of the remitter

Complete address, an email with the phone number of the remitter

Status (today) of the person remitter the transaction (company/ firm /other)

2. Remittance Details

Proposed date of remittance

Nature of transaction as per agreement (invoice copy to be asked from the client)

Source of fund proof (if any)

Country to and Currency in which remittance is made

Amount of remittance in Indian currency

3. Bank details of the Remitter

Name of the bank of the remitter

Details Name of the Bank with branch details

BSR code of Bank from which remittance is to be made –

4. Details of Remittee

Complete Name of the remittee :

Details of Country of the remittee (In which remittance is to be made)

Full address, email with the phone number of the remittee

Complete Main place of the business of the remittee

5. Documents from the Remittee

Form 10F duly filled by the authorized person of the remittee.

Document of Tax residency certificate from the remittee (Tax registration of the country in which remittee is registered).

Section under which order/certificate has been obtained ( if any )

6. Other details needed

Father’s name of the authorized person /signing person

Designation of the authorized person /signing person

Proof of payment of Tax on fund transfer from India,

Proposed date of remittance –

Complete name of such bank and branch –

Supporting Documents for Remittance

The digital signature of the person who required to fund Transfer,

If you’re searching for more current information on these forms, their processes, or any enforcement relevant to them, our team of experts will support you.

Penalty pursuant to Section 271-I of the Income Tax Act:

www.carajput.com; penalty-under-section-271i

Any person who fails for delaying or failing to submit Forms 15CA & 15CB to the Income-tax dept is entitled to impose a penalty of INR 1,00,000/- on the defaulter.

The penalty is also payable in the event that the person files incorrect information or files the wrong section of Form 15CA. The person shall be deemed to have defaulted until he/she has been unable to make a reasonable reason for failure to submit the form.

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}