Page Contents

International transactions come with a lot of tax implications. And one often is absent on these Section 195 of the Income Tax Act specifies that we withhold tax on sums that are taxable under the Statute. And the banks maintain these databases for financial transactions.

Additionally, anytime we make some payment to a non-resident, the bank tests whether or not we have paid duty. So for that dimension, they depend on Chartered Accountants certificates. We are sending this information to banks with Form 15CA and CB. Type 15 CB is usually prepared and approved by CA.

This blog explains Applicability of Form 15CA and Form 15CB w.r.t Taxability under the IT Act, Overview of Section 9 and Documentation needed for Form 15CA and Form 15CB, What is necessary of Form 15CA and Form 15CB, What is Form 15CA and Form 15CB, Payment / Remittances does not require Form 15CA & Form 15CB, which requires Remitter information, Remittee information, Remittance details, Bank details of the Remittance.

Certification 15CA is the remitter’s declaration. And a method used to collect information about payments made to non-residents. Indeed the form includes the remittance information. As well as the transaction’s tax details. In fact, whether or not the invoice is subject to vat.

Registered dealers and banks are now making sure we pay taxes on purchases that are made by them. And they are asking us to request these forms before the transaction is processed. They compile those forms and exchange them with the tax authority in addition.

This actually forms part of an Income Tax Department Information Management Framework. To assess tax responsibility, it monitors the overseas remittances and their existence.

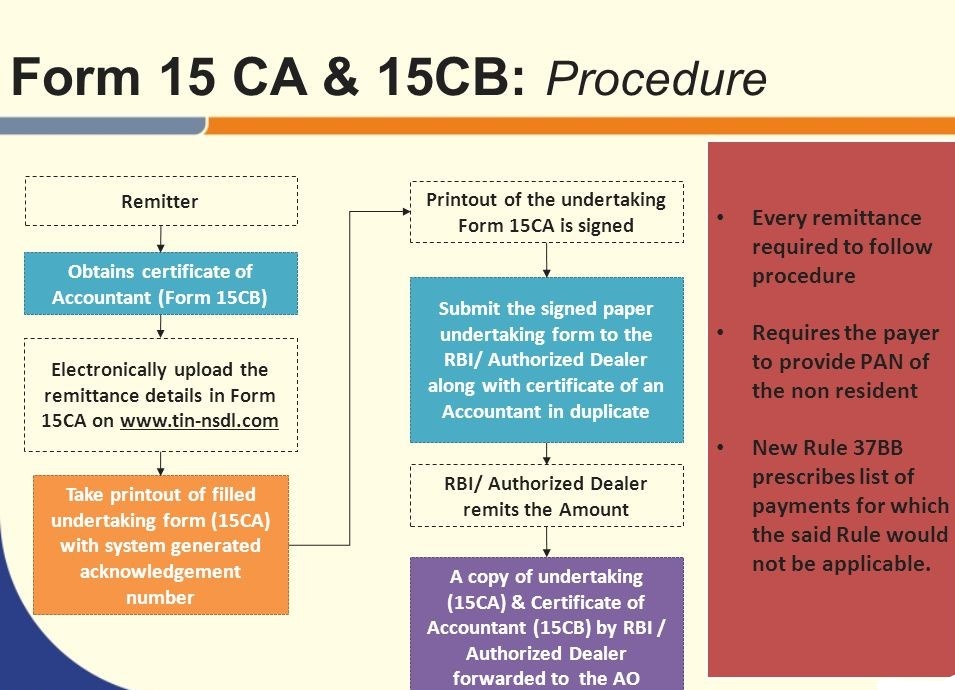

Department of Income Tax has also created an online facility to file these documents. Therefore we register Form 15CA with the IT department online. Though we are still printing and sharing the details with the bank / AD after submission online.

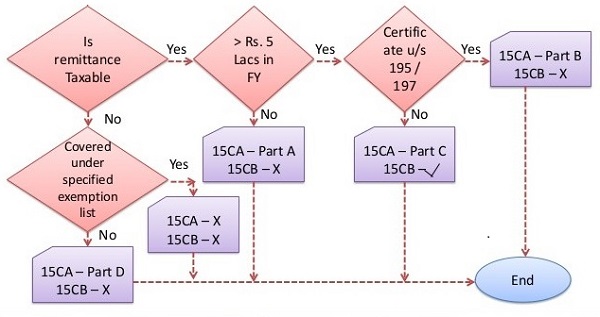

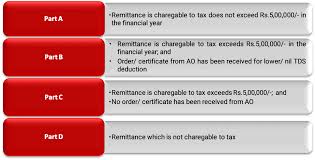

We divide form 15CA into 4 parts––

Form 15 CB is a certificate, and a Chartered Accountant is required to sign. The certificate sets down in detail the rates and taxes payable. Or in some situations, explanations why taxes are paid.

All types have basically the same material. 15CB does require registration, however. We also file Form 15CB first as its acknowledgment number is provided while filling the Form 15CA

Form 15CA & CB Applicability

Whether furnishing forms 15CA & 15CB are required for each and every foreign transaction?

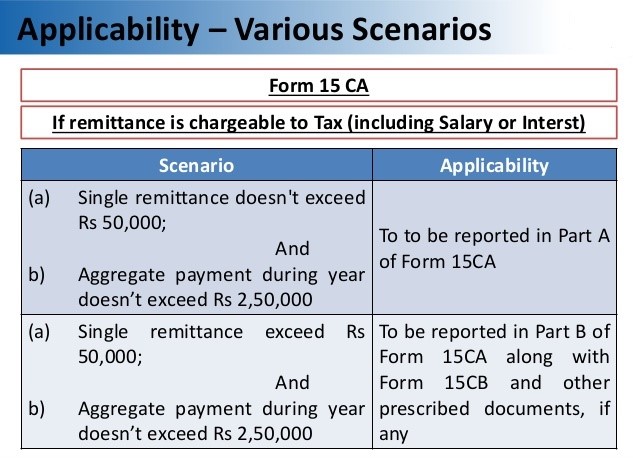

In addition, as per the Updated Income Tax Laws, we now only need Form No. 15CB for all taxable and exceeding Rs 5 lakhs payments.

The following types of transactions are not needed for the 15CA CB form:

A person responsible for making the payment to a non-resident or a foreign corporation must have the following information –

Information for these payments is provided in Part A of Form 15CA

No information is needed where The remittance is made by a person and does not need prior approval by the Reserve Bank of India [as provided for in Section 5 of the Foreign Exchange Management Act, 1999 (42 of 1999) read in Schedule III to the Foreign Exchange

Notes: We’ve heard of situations where banks are always calling for a 15CA CB even though they don’t need it. In the case of the following forms of foreign remittances (as provided for in Rule 37BB), no filing shall be made in Form 15CA and 15CB, in compliance with the Income Tax Laws. Click here for the full list.

https:/www.incometaxindia.gov.in/Rules 20Rules/103120000000007406.htm

The new rules for filing electronic forms 15CA and 15CB are valid as of 1 April 2016. The comprehensive method of filing the form according to specifications is based on new regulations. The department of income tax has updated the rules on form 15CA and formula 15CB preparedness and application (see previous Form 15CB rules). From 1 April 2016, the new rules came into effect.

We are used to assisting our clients in transferring money from India to India after Fulfilling the Fund’s origins and taxability, below four Stages for Procedures to follow:

If you are searching for more current information on these forms, their protocols or any related enforcement, our team of experts will assist you.

Any person who fails for delaying or failing to submit Forms 15CA & 15CB to the Income-tax dept is entitled to impose a penalty of INR 1,00,000/- on the defaulter. The penalty is also payable in the event that the person files incorrect information or files the wrong section of Form 15CA. The person shall be deemed to have defaulted until he/she has been unable to make a reasonable reason for failure to submit the form.

Due to technical issue of the Released recently income Tax Portal, Manual Submission of 15CA/CB to AD are allowed, AD is encouraged to accept the manual form. Later on, service will be supplied to upload such manual forms for records.

We will also assist you in setting up your business in India, including accounting, bookkeeping, payroll, auditing, valuation, secretarial compliance, trademark registration, market structuring, and consulting services. If you need support in this respect please visit www.carajput.com.

Popular blog:-

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}