Page Contents

The Statement of Financial Transactions (SFT) is a document or report that provides a comprehensive overview of an entity’s financial transactions over a specific period. It is a critical component of financial reporting and is typically prepared by businesses, organizations, and government agencies to accurately depict their financial activities and position.

Section 285BA requires specified persons to report high‑value financial transactions or registered financial activities to the Income Tax Department. The objective is to strengthen the Annual Information Statement (AIS) and ensure better tax compliance. Entities covered include banks (including co‑operative banks), post offices, companies issuing shares or debentures, NBFCs, registrars/sub-registrars, Mutual fund houses and Any other persons notified. The section ensures that transactions reflecting potential taxable events are captured through an institutional reporting mechanism.

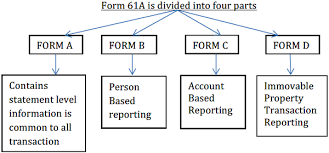

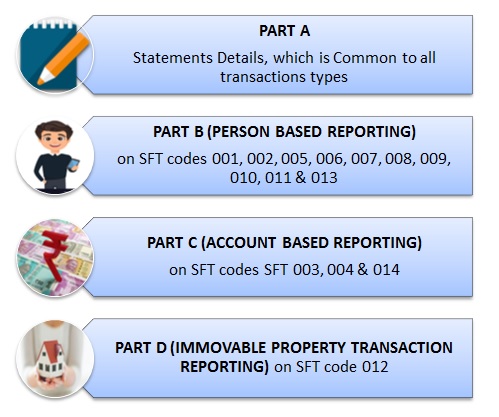

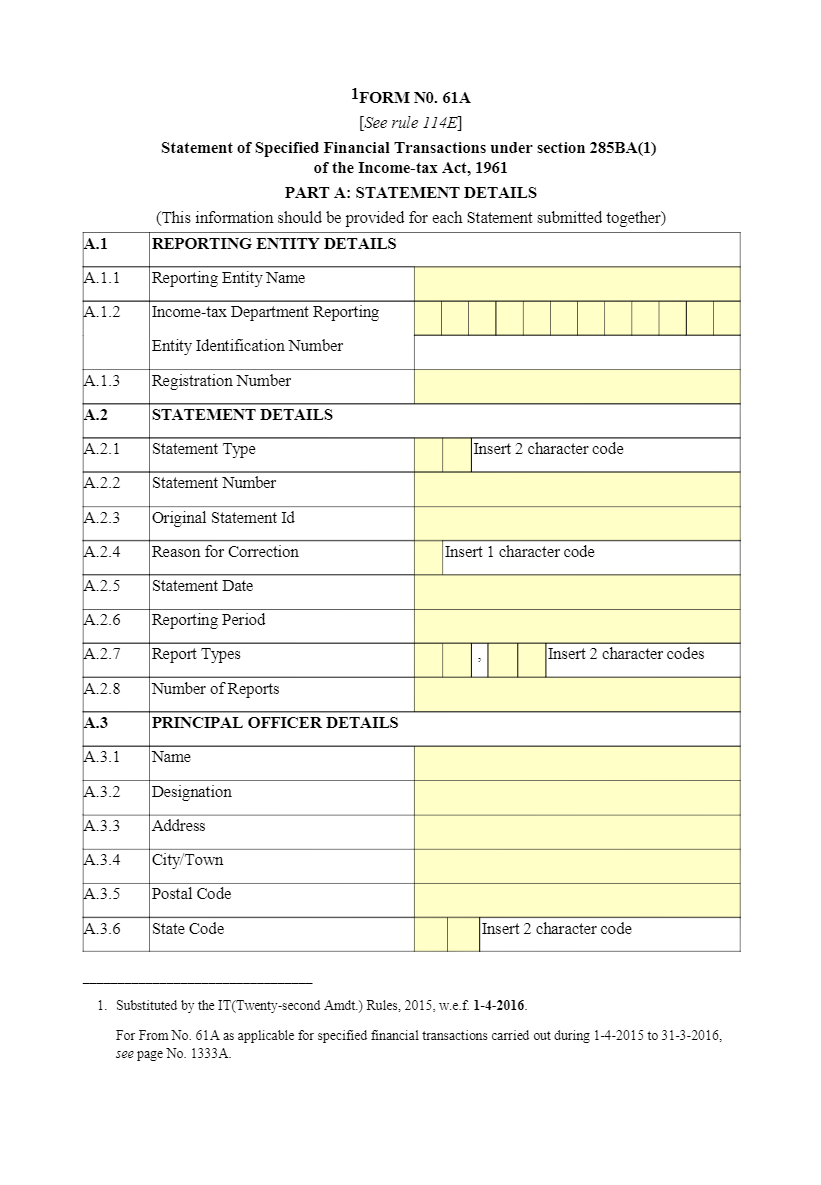

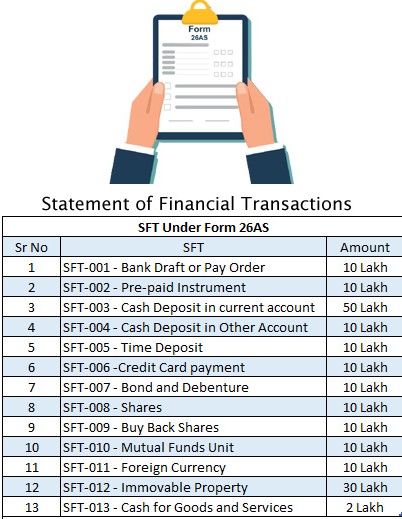

Income-tax Rules, 1962 : Rule 114E prescribes Which transactions must be reported, threshold limits, reporting format (Form 61A), and due date of filing (generally 31 May following the financial year). Following are reportable transactions under SFT—key thresholds. Below is a thematic summary of major SFT categories and limits:

| Account Type | Threshold |

|---|---|

| Current Accounts | Cash deposits or withdrawals exceeding INR 50 lakh in a FY |

| Savings Accounts | Cash deposits exceeding INR 10 lakh in a FY |

Co‑operative banks are fully covered.

| Mode of Payment | Threshold |

|---|---|

| Total annual payments | More than INR 10 lakh |

| Cash payments | More than INR 2 lakh |

All banks and credit card issuers are required to file SFT for these cases.

Reporting is required when a person acquires shares, debentures, or bonds or invests in mutual fund units amounting to ₹10 lakh or more in a financial year. This ensures visibility of large capital market investments. Reporting entities the indicative list includes banks (public, private, and co‑operative), post offices, companies issuing securities, NBFCs, mutual fund houses, sub‑registrars, and credit card issuing institutions. These institutions collectively provide financial footprints of taxpayers, enabling a complete AIS profile.

The SFT mechanism supports detection of undisclosed income, high‑value transaction tracking, cross-verification of AIS/TIS entries, and better risk evaluation for compliance enforcement. It is an integral part of the government’s financial transparency and anti‑evasion ecosystem.

The statement of financial transactions shall electronically be submitted in relation to an FY by the reporting entity with a DSC of the person responsible for verifying the declaration in Form No. 61A. The statement of financial transactions shall be submitted instantly after the FY in which the transaction is registered or registered on or before 31 May.

In case of non-furnishing of the statement of financial transactions within the due date, Total, a penalty of Rs 500/- per day from the expiry of the original due date till the due date mentioned in the notice and Rs 1,000 per day beyond the due date specified in the notice. (Reference from Section 271FA of the Act)

The penalty of Rs 50,000 will be levied on the prescribed reporting financial institution if it provides inaccurate information in the statement where:

Popular Article :More read for related blogs are:

Contact Us

You may find us via email at singh@carajput.com or by phone at +91 9555 555 480, You can contact our NRI consultant in India or NRI ITR filing services in India. We also offer income tax compliance & registration services!

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}