Page Contents

The GST Composition Scheme is designed for small taxpayers to reduce the burden of tax enforcement. Small taxpayers do not need to file monthly GST returns, and they need to pay marginal GST at a fixed turnover rate.

Any company with an annual turnover of up to 1.5 Crore can opt for GST registration under the composition scheme.

· Manufacturer of ice cream, pan masala, or tobacco

· Businesses that supply goods through an e-commerce operator

· Relief of taxpayers providing exempt supplies

· Supplier of services other than service providers for restaurants

· Casual taxable person or non-resident taxable person

The Composition System is a simple and easy scheme for taxpayers under the GST. Small taxpayers can get rid of tiring GST required documents and pay GST at a fixed turnover rate.

Any taxpayer whose revenue is less than Rs. 1.5 crore* can opt for this scheme.*Central Board of Indirect Taxes and Customs notified the increase to the limit from Rs 1.0 Crore to Rs. 1.5 Crores.

In order to benefit from the benefits of this program, taxpayers must register on a voluntary basis. If as the case may be the taxpayer’s yearly income turnover reaches 75 lakh, it will be moved to the normal scheme. Taxpayers who are already part of the composition of GST must register on a voluntary basis under this scheme.

The tax rate or recommended for different categories of Gst Composition Scheme registered persons has been defined below:

The GST Composite Dealer in GST shall not issue a tax invoice and shall only issue a Bill of supply containing the following details:

| a) | Name, GSTIN, and address of the supplier |

| b) | a serial number not exceeding 16 characters, in one or various series, containing alphabets or numerals or special characters |

| c) | date of its issue |

| d) | Name, address, and GST Tax Identification Number or Unique Identity Number, if registered, of the recipient |

| e) | HSN Code for goods or services |

| f) | Particular of goods or services or both |

| g) | Value of supply of goods or services or both after considering discount or abatement, if any; |

| h) | a signature or digital signature of the supplier or his authorized representative |

| Composition Scheme | Regular Scheme | |

| Filling of GST Return | Composition taxpayers needed to file quarterly return. | Ordinary taxpayers needed to file the monthly return. |

| Issue of Tax Invoice | Composition taxpayers can not issue tax invoices to their clients. | Normal taxpayers can issue a tax invoice to their clients. |

| Applicable Tax Rate | Composition taxpayers need to pay nominal GST at a fixed rate of turnover, which is normally 1-5%. | The tax rate for regular taxpayers’ goods and services, which is from 0-28%. |

| Input Credit | Composition taxpayers cannot avail of ITC benefits. | Normal taxpayers can avail of ITC benefits. |

| Regular Compliance | Relaxed Compliance in order to safeguard small businessmen. | Normal compliance required. |

It focuses on the fulfillment of the conditions discussed above but the person qualified for the scheme can also opt-out of the scheme by filing an application. In the event that the Proper Officer has grounds to suspect that the taxpayer is not eligible for the scheme or has contravened any of the Rules or Actions, the Proper Officer may issue a notice of cause followed by an order rejecting the scheme.

Composition Scheme Rules under the GST specify for the submission of various forms intended for the respective purposes, followed by a deadline for the submission of the following forms:

| Form Required | The objective of filling FORM | Timeline of compliance |

| GST CMP-01 | To opt into the scheme by provisional GST Registration holder | before the appointed date or within thirty days of the said date |

| GST CMP-02 | Intimation of willingness to opt into the scheme for GST registered normal taxpayers | Prior to the commencement of FY |

| GST CMP-03 | Details of stock and inward supplies from registered and unregistered persons | Required to comply within ninety days of the exercise of the option |

| GST CMP-04 | Intimation of withdrawal from the scheme | Required to comply within seven days of the occurrence of the event |

| GST CMP-05 | Show cause notice on contravention of Rules or Act by a proper officer | On any contravention |

| GST CMP-06 | Needed to reply to show cause notice | Required to comply within fifteen days |

| GST CMP-07 | Issue of Order | Required to comply within thirty days |

| GST REG-01 | Required for Registration under GST Composition scheme | before the appointed date |

| GST ITC-01 | Details of semi-finished, inputs in stocks & finished goods | thirty days of withdrawing option |

| GST ITC-03 | Needed for intimation of ITC available | Required to comply within Sixty days of commencement of the FY. |

The person opting for the scheme must not be a casual taxable person or a non-resident taxable person. The goods kept by him in stock on the appointed date shall not be purchased from a place outside his state. Therefore the products should not be listed as:

Where taxpayers deal with unregistered individuals, the tax must be paid or no stock must be kept.

More Read:

Reasons for the Movement of Goods under the GST

Refund mechanisum under GST service export

It is not a manufacturer of products that may be notified by the Government during the preceding financial year.

Compulsory show of invoices with the words “composure of taxable persons not liable for tax on supplies”

Compulsory display of the words “Composition Taxable Citizen” on each notice and sign displayed at a prominent location

If the taxable person is not eligible for the scheme of the composition of the GST, the tax authorities may impose a penalty equal to the amount of tax on the taxable person along with his tax liability.

Be patient while using this scheme and paying taxes. The penalty shall be levied in compliance with the provisions of Section 73 or 74 where a person represents inaccurate information under the composition scheme.

All Composition Dealers who have preferred composition scheme for some time, must file GSTR 4 on a yearly basis from 01.04.2019 on.

| Quarterly Period | Timeline Dates |

| 1st Quarter – April to June 2020 | 18th July 2020 |

| 2nd Quarter – July to September 2020 | 18th October 2020 |

| 3rd Quarter – October to December 2020 | 18th January 2021 |

| 4th Quarter – January to March 2021 | 18th April 2021 |

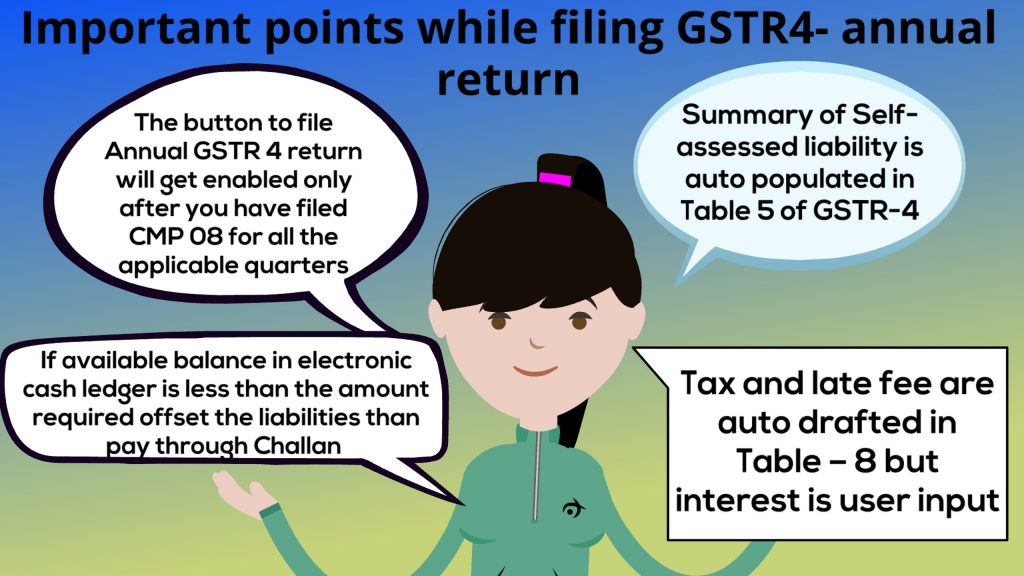

Note: Point to be considered while using offline Tool

Current features of GSTR 4 Return Form

Currently, the GSTN has agreed to encourage residents, assessors, and companies to file GSTR 4 on an annual basis. This has been achieved because of the community’s demand.

The form is also available on the site, which further eased the assessment and the taxpayers in identifying and submitting the form as per their approval.

11. Recent Council GST Meeting with regard to for Composition Traders

After filing on the GSTN Site, GSTR-4 can not be updated.

13. Is there a penalty for the late filing of GSTR 4?

A delayed fee of Rs. 200 per day shall be charged if the GSTR-4 is not filed within the due date. The cumulative late fee can not, nevertheless, exceed Rs. 5,000.

14. The basic term normally used in GSTR 4

Any person who opts for the Gst Composition Scheme shall be deemed to have opted for all places of business having the same registered PAN. Therefore you cannot want any of the places of business to be registered under the scheme.

GST Issue: Some taxpayers whose GST registration under the Composition Scheme was cancelled have reported receiving notices in Form GSTR-3A for non-filing of GSTR-4, even though they are no longer active.

GST Dept Clarification:GSTN has clarified that Form GSTR-4 is required to be filed for the financial year in which cancellation took place, irrespective of the date of cancellation. For example, if a taxpayer’s registration was cancelled on 30th September 2024, they are still required to file GSTR-4 for FY 2024–25. Failure to do so will trigger the issuance of notice in GSTR-3A.

Verify if GSTR-4 for the relevant FY has been filed. If not filed, they must immediately file GSTR-4 to avoid late fees and further legal action. If already filed and notice received in error, taxpayers may contact GST Helpdesk or raise a grievance through the GST Portal. The rules of the Gst Composition Scheme under the GST were supposed to be strict and strict for the individuals using the Composition Scheme.

Popular blog:-

SALIENT FEATURES OF NEW GST SYSTEM IN INDIA

Key points of 42nd GST council Meeting headed By FM N. Sitharaman

GSTN enable auto-populated in the E-invoice information into GST Return -1

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}