Main points of 42nd GST council Meeting by video conferencing

The 42nd GST Council met by video conference under the directorship of Union Finance & Corporate Affairs Minister Smt NirmalaSitharaman. Union Minister of State for Finance & Corporate Affairs Shri Anurag Thakur, along with State & UT Finance Ministers and senior officers of the Ministry of Finance & States / UTs, also attended the conference.

Result of the 42nd GST Council meeting by video conferencing is proposed :

The cessation of compensation is expanded beyond a transitional duration of 5 years. As specified in the GST(CS) Act, 2017, ending in June 2022. The act is updated accordingly.

Existing GSTR-1/3B return filing procedure will be extended to 31st Mar 2021.

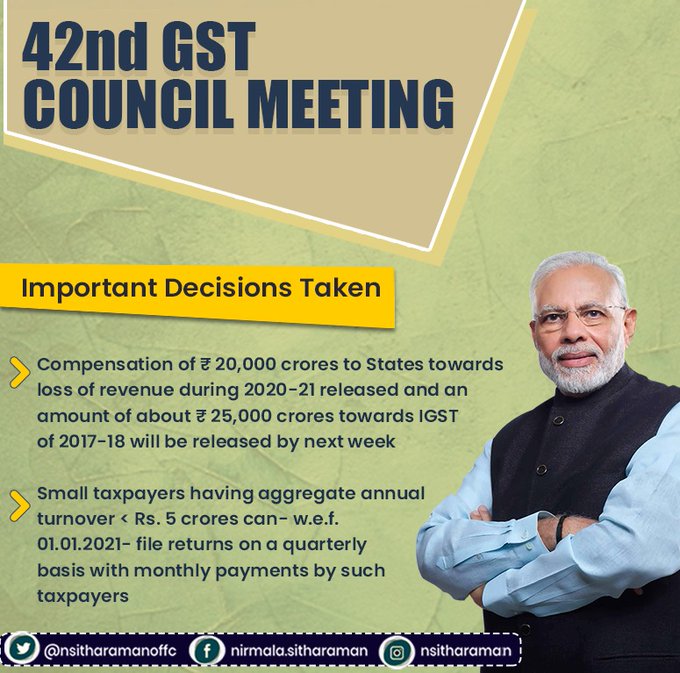

Taxpayers with aggregate turnover less than 5 crores are permitted from 1st January 2021 onwards to file returns (both FORM GSTR-1 and FORM GSTR-3B) on a quarterly basis in an approved bank account connected with the registrant’s PAN & Aadhaar. Even so, in the first two months of the year, these taxpayers would have to pay at least 35 percent of the last quarter’s net cash tax liability by using the auto-generated challan and adjustment should be made for the balance in the third month of the year while filing the return.

For the submission of refund claims, Refund to be paid/disbursed on an approved bank account connected with the registrant’s PAN & Aadhaar with effect from 1st Jan 2021. DSC is no longer compulsory. It can also be signed through Aadhaar authentication.

To promote satellite launching services by new start-ups, the ISRO provided satellite launch service, Antrix corporation ltd. and NSIL will be excluded.

With effect from 1st April 2021, the provision for disclosing HSN codes / SAC in tax invoices and Type GSTR-1 has been updated as follows-

Aggregate turnover more than or equal to Rs. 5 Crore

4 digit of HSN/SAC

Aggregate Turnover less than Rs. 5 Crore

6 digit of HSN/SAC

For other categories of suppliers notified soon

8 digit of HSN/SAC

www.carajput.com; 42 GST council meeting

The CG will disburse to the States tonight the reimbursement cess collection, amounting to Rs. 20,000 crores, against the tax shortfall for FY 2020-21.

In addition, the state’s share of the FY 2017-18 IGST collection, amounting to approximately. 25,000 crores, to be disbursed by next week as well.

Another conference to reach the official notice will be held on 12 October 2020 in regard to payments to States with a revenue deficit.

The existing form GSTR-1/3B system is to be expanded till 31 March 2021 and the GST regulation is to be changed to make this system the default return filing system. Additionally, payment of tax will be made monthly through challan.

FORM GSTR-3B output tax obligation is auto-populated on the basis of FORM GSTR-1 filed by the taxpayer.

FORM GSTR-3B input tax credits are auto-populated on the basis of FORM GSTR-2B filed by monthly filers’.

With effect from 1st April 2021

FORM GSTR-3B ‘ input tax credit is auto-populated on the basis of FORM GSTR-2B filed by quarterly filers.

FORM GSTR-1 is compulsory to be filed before FORM GSTR-3B in order to ensure the auto-population system as stated earlier.

Amendment to the CGST Rules: Multiple amendments to the CGST Rules and FORMS, including requirements for the provision of Nil FORMCMP-08 via SMS, have been proposed.

Note:- In this notice, the decisions of the GST Council were submitted in simple language for easier interpretation. The same effect will be granted to notifications/circulars from the Gazette that alone has the force of law.

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}