Page Contents

Foreign companies planning to set up their business operations in India need to start a liaison office. The main purpose of starting a liaison office is to explore possible business opportunities in India by gathering relevant business information.

This helps the companies to develop a business strategy to tap the existing business potential in India. A liaison office also acts as a marketing channel to provide business information about the parent company and its products to the prospective clientele in India.

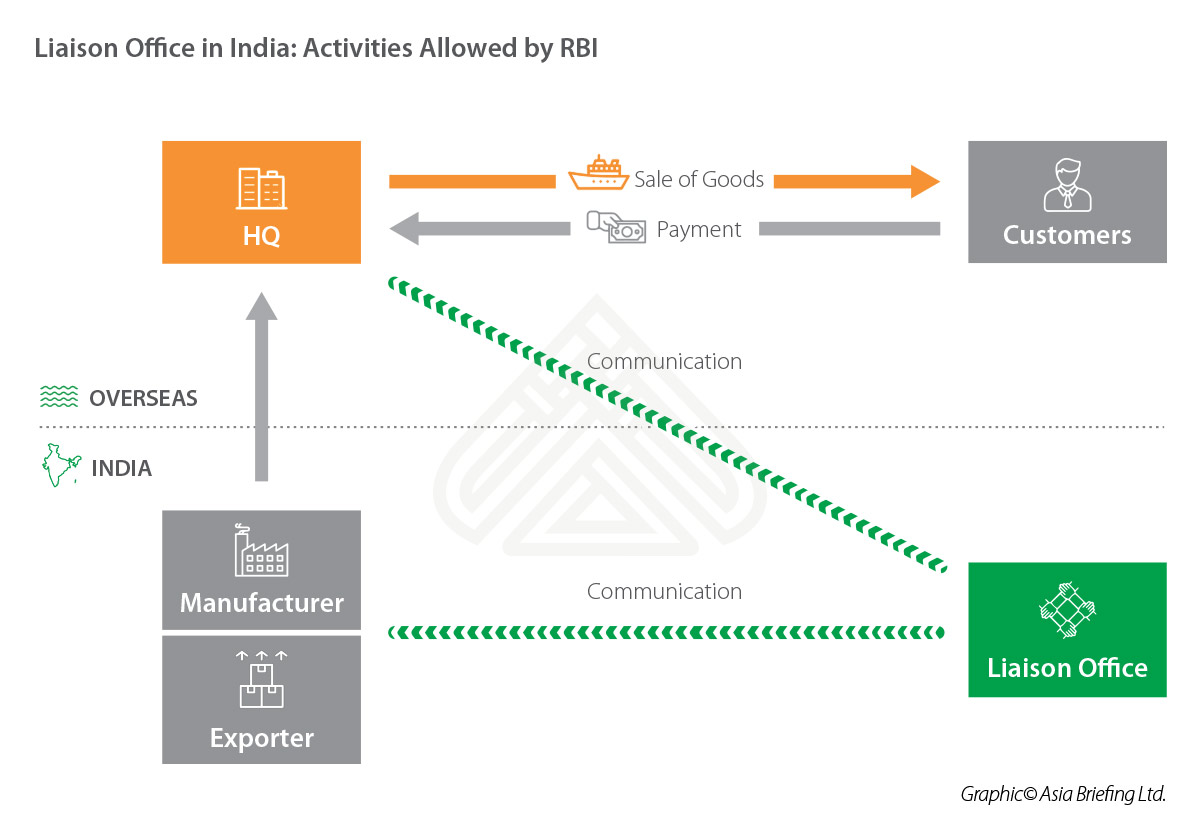

As the name suggests the Liaison office is set up by a foreign company in India to carry out the liaison activity for its business. The company cannot have any revenue for the Indian Liaison office.

It has to meet all its expenses of the Indian office through remittances from the Head office. The Liaison office is not allowed to earn any income in India

liaison office is suitable for a foreign company to test and understand the Indian market, as it does not allow the companies to do business but just to be in the market and understand the Indian market or carry out the Research & Development activities or to understand the problem of existing clients of the company and serve them better.

Application for Liaison office Licenses is approved by the RBI , but as per the recent changes, the applications for Liaison office are routed through the A.D i.e Authorized Dealers.

Due to this the timeline for setting up the liaison office has increased tremendously. Further, the documentation required for the same has also increased.

Currently as per the RBI Requirement the application for the branch office and Liaison office is submitted through the Authorized dealer. The authorized dealer means the various institution having banking licenses.

The applicant of the Branch/Liaison office has to opt for the any of the Authorized Dealer , it is always preferable for the company to opt for the same authorized dealer as it is dealing in the home country.

NOTE – THE ABOVE LIST IS NOT EXHAUSTIVE AND MAY DIFFER DEPENDING UPON THE REQUIREMENT FROM THE AUTHORISED DEALER.

Every Liaison office registered with RBI shall get itself registered with the Ministry of Corporate Affairs, It is a registration by the Liaison office as an establishment of a foreign company in India.

On such registration, a CIN i.e. Corporate Identity Number is allotted by the Registrar of Companies. The following documents shall be filled with the Registrar of Companies :-

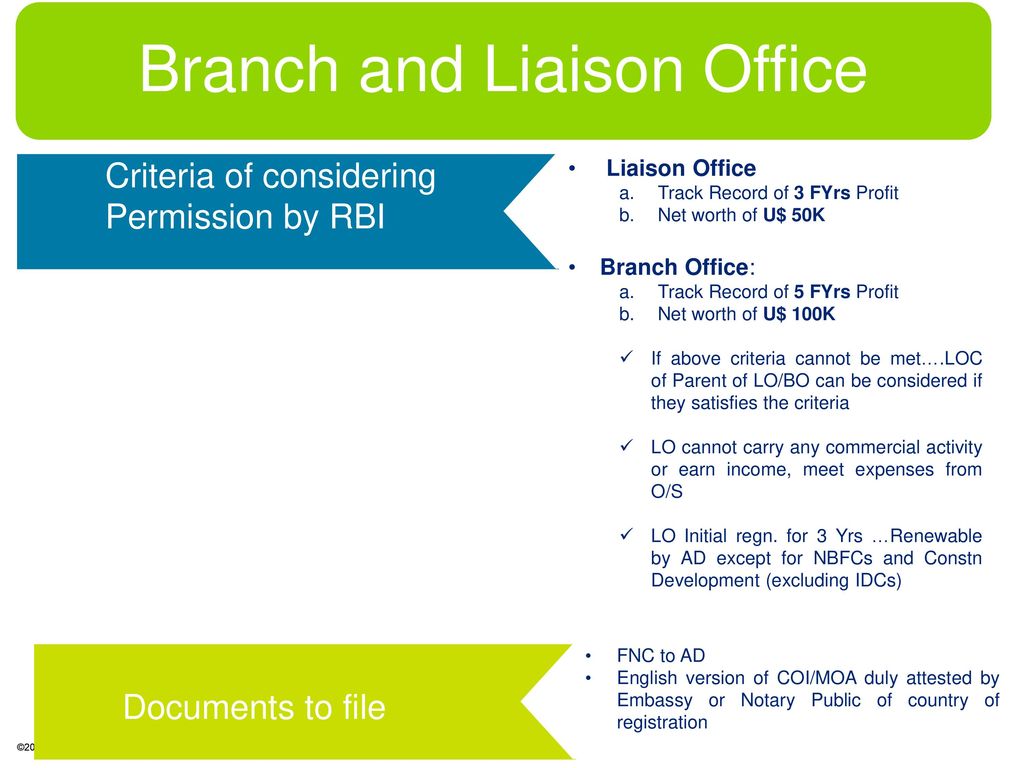

Generally, the Liaison office licenses is given for three years, if at any time the Company plans to close the Liaison office setup in India it shall file the necessary documents with the Authorized Dealer, and the application for the closure shall be forwarded by the Authorized Dealer.

Foreign companies can set up Liaison/Branch Offices in India after obtaining approval from Reserve Bank of India.

Reserve Bank of India has given general permission to foreign companies to establish Project Offices in India subject to certain conditions.

A Liaison office can carry on only liaison activities, i.e. it can act as a channel of communication between Head Office abroad and parties in India. It is not allowed to undertake any business activity in India and cannot earn any income in India.

Expenses of such offices are to be met entirely through inward remittances of foreign exchange from the Head Office abroad. The role of such office is therefore, limited to collecting information about possible market opportunities and providing information about the Company and its products to the prospective Indian customers.

The companies desirous of opening a liaison office in India may make an application in form FNC-1 along with the documents mentioned therein to Foreign Investment Division, Foreign Exchange Department, Reserve Bank of India, Central office Mumbai.

Permission to set up such offices is initially granted for a period of 3 years and this may be extended from time to time by the Regional Office in whose jurisdiction the office is set up. Liaison/ Representative offices have to flee an Activity Certificate on an annual basis from a Chartered Accountant to the concerned Regional Office of the Reserve Bank of India, stating that the Liaison office has undertaken only those activities permitted by Reserve Bank of India.

Foreign companies are granted projects in India by Indian entities. General Permission has been granted by Reserve

Bank of India Vide Notification No. FEMA 95/ 2003-RB dated July 2, 2003 to foreign companies to open Project

Office/s in India provided they have secured from an Indian company, a contract to execute a project in India, and

or bank in India for the project.

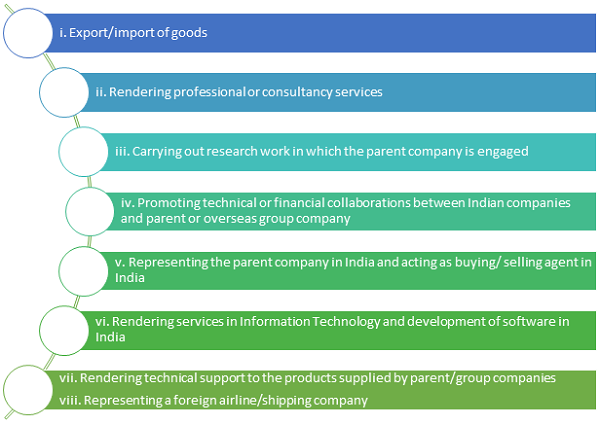

Reserve Bank permits companies engaged in manufacturing and trading activities abroad to set up Branch Office

in India for the following purposes:

A foreign company planning to set up business operations in India may:

An Indian company may receive Foreign Direct Investment under the two routes as given under:

Foreign investment is reckoned as FDI only if the investment is made in equity shares , fully and mandatorily Convertible preference shares and fully and mandatorily convertible debentures with the pricing being decided Upfront as a figure or based on the formula that is decided upfront. Any foreign investment into an instrument issued

By an Indian company which:

The FDI policy provides that the price/ conversion formula of convertible capital instruments should be determined upfront at the time of issue of the instruments.

The price at the time of conversion should not in any case be lower than the fair value worked out, at the time of issuance of such instruments, in accordance with the extant FEMA regulations [the DCF method of valuation for the unlisted companies and valuation in terms of SEBI (ICDR)Regulations, for the listed companies].

An Indian company issuing shares /convertible debentures under FDI Scheme to a person resident outside India

shall receive the amount of consideration required to be paid for such shares /convertible debentures by:

(i) Inward remittance through normal banking channels.

(ii) Debit to NRE / FCNR account of a person concerned maintained with an AD category I bank.

(iii) Conversion of royalty / lump sum / technical know how fee due for payment or conversion of ECB, shall be treated as consideration for issue of shares.

(iv) conversion of import payables / pre incorporation expenses / share swap can be treated as consideration for issue of shares with the approval of FIPB.

(v) debit to non-interest bearing Escrow account in Indian Rupees in India which is opened with the approval from AD Category – I bank and is maintained with the AD Category I bank on behalf of residents and non-residents towards payment of share purchase consideration.

If the shares or convertible debentures are not issued within 180 days from the date of receipt of the inward remittance or date of debit to NRE / FCNR (B) / Escrow account, the amount shall be refunded.

Further, Reserve Bank may on an application made to it and for sufficient reasons permit an Indian Company to refund / allot shares for the amount of consideration received towards issue of security if such amount is outstanding beyond the period of 180 days from the date of receipt.

FDI is prohibited under the Government Route as well as the Automatic Route in the following sectors:

iii) Gambling and Betting

vii) Housing and Real Estate business (except development of townships, construction of residential/commercial premises, roads or bridges to the extent viii) Trading in Transferable Development Rights (TDRs).

viii) Manufacture of cigars , cheroots, cigarillos and cigarettes , of tobacco or of tobacco substitutes.

Any Foreign Entity looking for an office in India as a sourcing division or to facilitate export or to test the Indian market with a prospective business venture to improve the relations with the authorities and business community or to have the presence in the country from worldwide business outlook, Liaison Office (LO) is the best option.

A Liaison Office or a Representative Office can undertake only liaison activities, which means that it can act as a channel of communication between the Head Office (out of India) and parties in India.

It is not allowed to undertake any commercial activity in India. As there is no income of Liaison Office of its own, its expenses are to be met entirely through inward remittances from the parent company outside India received in Convertible Foreign Exchange.

Establishment of Liaison Office/Representative Office in India is governed by Reserve Bank of India (RBI) together with Ministry of Finance, Government of India.The rules and regulations in respect to Liaison Offices are framed under Foreign Exchange Management Act, 1999 and Circulars/Notifications issued by RBI from time to time.There are 2 routes to establish a Liaison Office in India:

If the industry the Foreign Entity is in, comes in the specified industries for 100% automatic route of investment as per Foreign Direct Investment Policy then the Liaison Office will be approved by the Reserve Bank of India.

If the industry the Foreign Entity is in, doesn’t come in 100% automatic route and Non Profit and Non-Government Organization, then the Liaison Office will be approved by Reserve Bank of India in consultation of the Ministry of Finance, Government of India.

In addition to above, Reserve Bank of India has prescribed eligibility criteria for Foreign Entities to apply for Liaison Office. The application of Foreign Entities satisfying the below criteria will be processed:

The other prerequisites of Liaison Office application are to have a designated manager of the proposed Liaison Office and a prospective office space of the proposed Liaison Office which can be provided by consultants who help the foreign entities in applying for LO as part of their services which is called Virtual Office or Service Office Services.

The Application has to be made to RBI through Authorized Dealer Category-1 Bank in India. RBI will allot a UIN (Unique Identification Number) on approval of the application. Once approved the intimation has to be given to Registrar of Companies (ROC) and Director General of Police (DGP).

An application has to be sen to the Income Tax Department to allot Permanent Account Number (PAN).

A Liaison office has to do minimal annual compliances as compared to other forms of business in India.

As annual compliance, an annual activity certificate issued by a Practicing Chartered Accountant at the end of March 31, need to be submitted to the Authorized Dealer Category-1 Bank, Directorate General of Income Tax (International Taxation), concerned Registrar of Companies and Director General of Police, on or before 30th September of each financial year (In India the Financial Year is April to March) including audited receipts and payments account.

Approval is generally given for a period of 3 years and extension is granted on the basis of

For establishing an additional office, a fresh application duly signed by an authorized signatory of the foreign entity is filed to Reserve Bank of India with a justification to open additional office and identify one of the offices as a nodal office to co-ordinate the activities of all offices.

Liaison Offices are very popular forms of business in India for a long time. However, the issue of the taxability of liaison offices still looms over the foreign entities and is not free from ambiguity.

To capture the entities in tax clutches, tax authorities have been contending that the liaison offices are transgressing the list of permitted activities and constitute the company’s permanent establishment in India.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances; Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@carajput.com or call at 9555-555-480

Overview on Amendments to the IBBI Liquidation Regulations (2026) The document proposes major changes to India's liquidation framework under the… Read More

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}