Page Contents

‘Electronic Invoicing’ or ‘E-invoicing’ is a mechanism in which GSTN automatically authenticates B2B invoices for further use on the Common Goods & Service Tax portal. From this portal, all invoice details will be transmitted in real-time to both the Goods & Service Tax portal and the e-way bill portal.

GSTN official sources said that, when an e-invoice is generated, a specific number will be issued to businesses that will fall below a specified unique number. These numbers should be matched by businesses with the invoices written in the GST Return and GST Taxes paid for authentication/ verification.

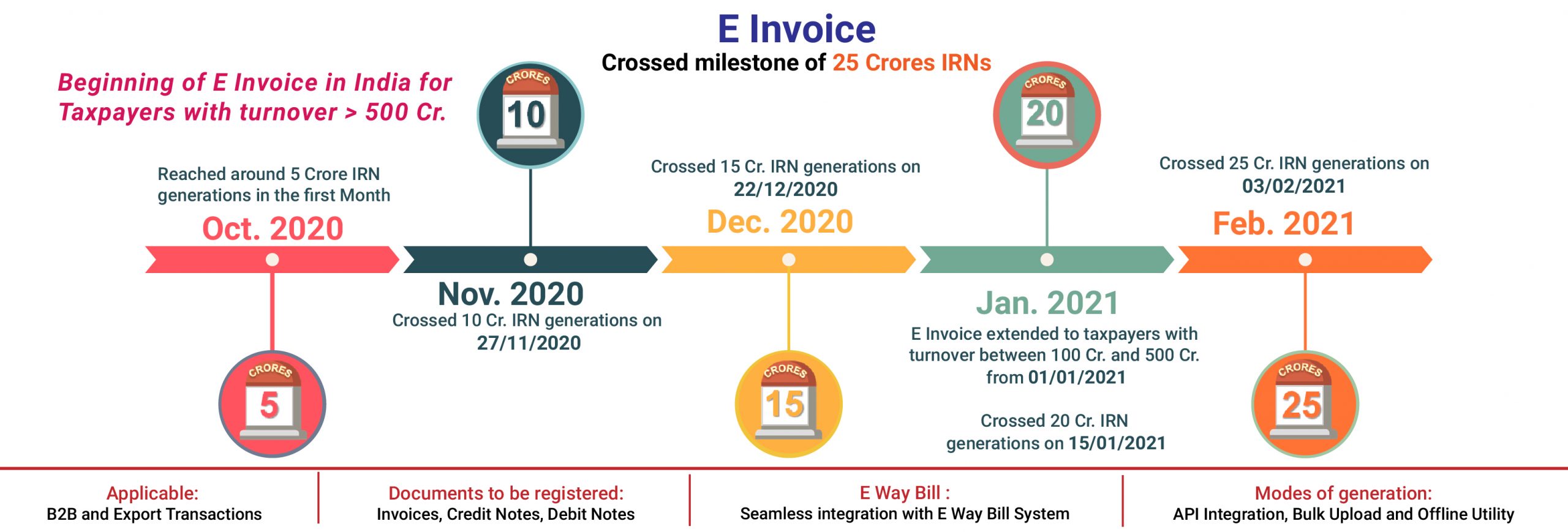

It will be compulsory for businesses to create an entire E-Invoicing under Goods & Service Tax, containing all the sales revenue. The assessee whose Sales is excess INR 500 Crore in the previous Financial Year from 2019-20, this assesse is needed to upload the E-Invoice details on the Government of India Invoice Registration Portal (IRP) with effect from 01st Oct 2020.

In consideration of the concept of E-Invoices in GST (Goods and Services Tax) some of benefits are;

Therefore, it is not a soft copy of the Goods & Service Tax (GST) invoices

Finally, the Government of India introduced the GST e-invoicing trial version of the common invoicing network, which was discussed earlier at the GST Council meeting. The GST e-invoicing would have several categories under which an e-invoice will be filled by the taxpayer on the basis of turnover and other requirements. For filing GST e-invoice vis. Govt. portal, it is compulsory that taxpayers must have a turnover of more than 500 crores.

The CBIC indicated that E-invoicing under GST is relevant for specified companies, especially those whose turnover of Excessed INR 100 Crores. As of 1 January 2021. Early this limit was the on Sales Excessed INR 500 Crores. (Notification No. 13/2020 – Central Tax, dated 21 March 2020)

In that notification, with effect from January 01, 2021, the words ‘five hundred crore ropes’ shall be replaced by the words ‘one hundred crore rupees’

The changes would impact medium-sized businesses within the e-invoicing circle. It is expected that B2B transactions will be open to the assessee as of 1 April 2021.

“The inclusion of dealers with turnover B/W INR 100-500 Cr within the E-invoicing gamut is another step towards the formalization of the Indian market. There may be some initial slowdowns in implementation, but in the long run, they are likely to result in more accountability, better tax administration, and automated tax compliance and filings,”

The GST electronic invoicing system for a business to business transactions from October 1 is mandatory for companies whose turnover is more than Rs 500 Cores.

In addition to the reform of the GST Mechanism, The GST Council has currently made a move to promote a new GST E-invoicing or electronic invoicing in a channelized manner to disclose B2B supplies to the GST Mechanism. This provision will be made on a voluntary basis with effect from January 01, 2020.

The provision will be made on a voluntary basis in effect from January 01, 2020. Like any new provision calls for a specific standard to be developed in order to accomplish the purpose in effect.

The basic standard for e-invoicing is finalized after consultations with trade/industry bodies and ICAI representatives to ensure the absolute applicability of the current e-invoicing under the GST scheme. Until now, No standard Fixed format for E-invoicing has been fixed.

The functioning of the e-invoicing is oriented in such a way that the e-invoices created by one software are controlled by another software, removing the need to re-enter the digits for a new entry.

The adoption of this specific standard will allow the seller, customer, bank or agent, or any other person concerned, to read by the computer and restrict unnecessary data, thereby minimizing errors. This is the main purpose behind improving the framework of the GST e-invoicing.

At the 37th GST Council meeting chaired by Union Finance Minister Smt. N Sitharaman, the standard of the new e-invoice system was discussed and approved, and the same scheme is published on the GST portal.

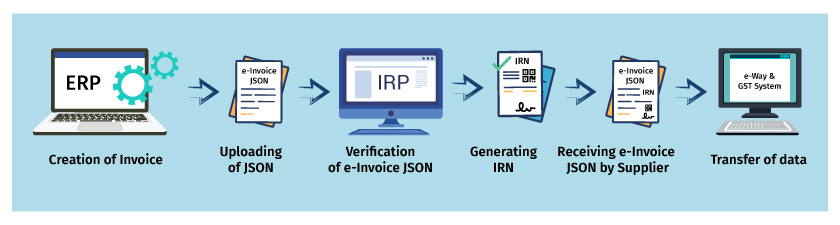

It is the duty of the taxpayer or companies to produce the invoice / s, and then send them for approval to the Invoice Registration Portal (IRP). The portal will return the invoice to the manufacturer, along with a unique reference number, digital signature, and a QR code, after successful verification. The e-invoice will also be exchanged with the corresponding buyer on the provided e-mail ID

Stage 1: Generation of an Invoice

The seller/supplier will use his / her accounting or billing software to create an invoice in the prescribed format (e-invoice schema). It must have the required details.

For each B2B invoice, the supplier’s accounting program must produce a JSON. The JSON file is imported into the IRP.

Stage 2: Generation of an IRN

The next step will be to use a standard hash-generation algorithm to create a unique invoice reference number (IRN) by the vendor.

Stage 3: Uploading the Invoice

Now the seller will upload JSON to the IRP, either directly or via 3rd party software, for each of the invoices, along with Invoice Registration Portal.

Stage 4: Sign and Authenticate

If it’s not already uploaded by the supplier, Invoice Registration Portal will validate the hash / IRN attached to JSON, or generate an Invoice Registration Portal.

Then, it verifies the file against GST’s central registry.

After complete verification, JSON will have its signature attached to the invoice and a QR code.

The earlier created hack will become the new E-invoice IRN. The e-invoice will be the unique identifier for the whole financial year.

Stage 5: Data-sharing

The data uploaded will be shared with both the E-way bill & GST program.

Stage 6: Download E-invoice

The GST Portal will forward the digitally signed JSON with IRN and QR code back to the seller. The E-invoice is also sent to the customer on their registered email I d.

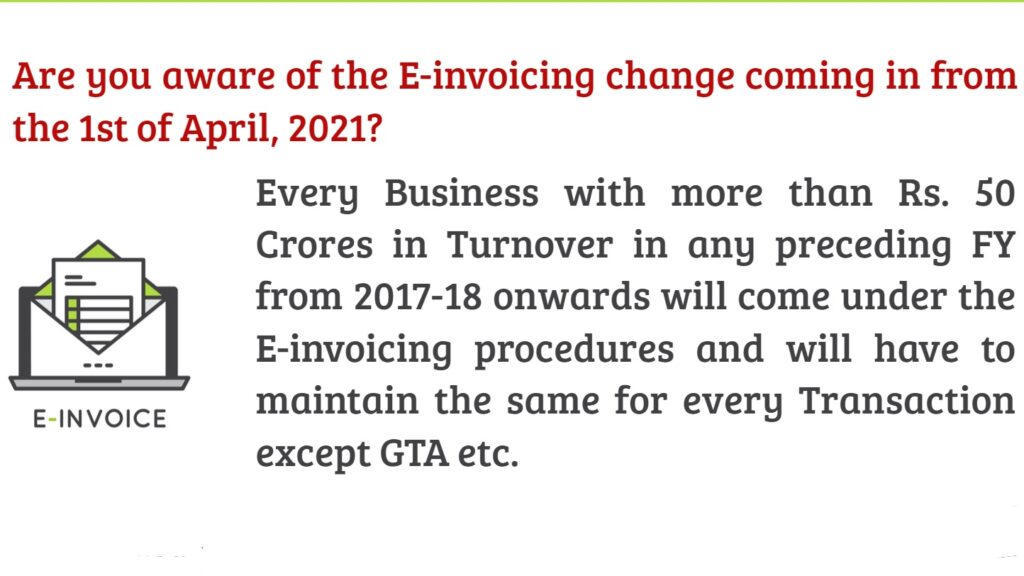

CBIC has issued the attached Notification (Notification No. 5/2021 dt. 08th March 2021), in which the e-invoicing requirement threshold limit has been reduced from Rs.100 Crores to Rs.50 Crores with effect from 1st April 2021. Hence, effective from 1st April, 2021, all GST registered dealers whose aggregate turnover exceeds Rs.50 Crores in any of the preceding financial years starting from 2017-18, shall comply with the requirement of E-invoicing and generate their Tax Invoices through IRP portal and issue such invoices with QR code and IRN number.

Notes :

Popular blog:-

GSTN: Available Tax Payer Features in the GST Portal

How to charge GST on expenses in the invoice?

about GSTN enable details to be auto-populated in E-invoice GSTR-1

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}