Page Contents

CBDT issued order an explanation/ clarification U/s 119 on 9-04-2020 on questions arising from orders issued on 31 March and 3 April 2020, The above said Orders extended the timelines for the application and issuance of Certificates for Lower or Nil Tax Deducted at Source/ Tax collected at Source pursuant to Sections 195, 197 and 206C of the Income-tax Act for the Financial Year 2019-2021, in the light of Coronavirus-19 Pandemic

Background

To mitigate the prospective hardship of taxpayers triggered by the forced disturbance of working practices in the view of Coronavirus-19 Pandemic, On 31 March 2020, the Central Board of Direct Taxes issued Order U/s 119 of the ITA providing for alterations and amendments to the application of lower or zero Tax Deducted at Source/ Tax collected at Source for the financial year 2019-2021.

Consequent orders issued on 3 April 2020 clarified the position with respect to applications filed on time for low or zero certificates via the TRACES (TDS Reconciliation Analysis and Correction Enabling System) portal for the financial year 2019-2020, which had not been processed as of that date.

The CBDT acknowledged that the applicants must contact the appropriate Assessing Officer (AO) by e-mail, informing the AO that the application had not been received and providing the necessary documents together with evidence that the application had been filed through the TRACES portal. The AO must process the application by 27 April 2020 and communicate the issuance of the certificate or the refusal of the application by e-mail. The certificate issued for the financial year 2019-2020 will continue to apply for amounts credited/debited during the financial year 2019-2020 after the date of the application but will remain unpaid or not received until the date of issue of the certificate.

In order to provide relief for small taxpayers, the Central Board of Direct Taxes issued a further order on 3 April 2020, clarifying that the valid Forms 15G and 15H submitted to banks or other institutions facilitating stipulated income to be paid without tax deduction at source for the financial year 2019-2020 would’ve been valid until 30 June 2020.

In a press release dated 4 April 2020, the Central Board of Direct Taxes clarified the position in relation to payments made to a non-resident with a permanent establishment in India. The press release indicates that where if an application for a lower or zero rate of Tax Deducted at Source/ Tax collected at Source is ongoing, the tax on payments made in the financial year 2019-2021 will be deducted at a subsidized rate of 10% (which include surcharge and cessation) until 30 June 2020 or the date on which the application is made.

Clarification By CBDT

Regarding the issue of all the above orders, amount of observations were made by taxpayers seeking guidance on the different aspects of the orders, which led the Central Board of Direct Taxes to make the following clarification on 9 April 2020:

| Applicable relevant provision of the Order of 31 March 2020 | The explanation is given by The Central Board of Direct Taxes |

| Where taxpayers have introduced for a lower or zero rate of Tax Deducted at Source/ Tax collected at Source via the TRACES portal (U/s 197 or 206C(9) of the ITA, respectively) for the financial year 2019-2021, and an application is pending, but a certificate for the financial year 2019-2020 has been issued, the financial year 2019-2020 certificate will implement for the financial year 2019-2021, or the date on which it is issued, for the financial year 2019-2021. | Subject to the requirements set out in the Order of 31 March 2020: The lower or zero rate Tax Deducted at Source/ Tax collected at Source certificates will be valid for the specific time period for which they were imposed for the financial year 2019-2020 and for an even farther period from 1 April 2020 to 30 June 2020 for the financial year 2019-2021; and |

| If taxpayers would be unable to apply for a certificate for the financial year 2019-2021 through the TRACES portal (U/s 197 or 206C(9) of the ITA) but have issued a certificate for the financial year 2019-2020, the financial year 2019-2020 will pertain for the financial year 2019-2021 until 30 June 2020. Such taxpayers must apply for the financial year 2019-2021 certificate when the common procedure is restored or by 30 June 2020, which would be even earlier. The request to the AO must include details of the transactions and the deductor/collector of the Tax Deducted at Source/ Tax collected at Source. | The transaction limit/threshold set out in the certificate for the financial year 2019-2020 will be restored for the period from 1 April 2020 to 30 June 2020 for the financial year 2019-2021. The cutoff will be the same as that set for the financial year 2019-2020. |

The Central Board of Direct Taxes also explained that authorised e-mails or other electronic information may be used by the tax authorities for internal approvals relating to the issuance of a lower/zero Tax Deducted at Source/ Tax collected at Source Certificate, and for the notification of the outcome to the applicants.

The relaxation provided for certificates for the financial year 2019-2020 does not apply to the inclusion of a new TAN in the application for the financial year 2019-2021 or where the Source/Tax Deducted Tax collected at Source Rate is greater in the financial year 2019-2020 and the application for the financial year 2019-2021 is lower in order to understand the effect of Coronavirus-19 Pandemic.

The Central Board of Direct Taxes clarification is helpful in understanding the relaxation granted by the different orders for extension of the application and the certificate for the financial year 2019-2020 for the timeframe 1 April to 30 June 2020 for the financial year 2019-2021.

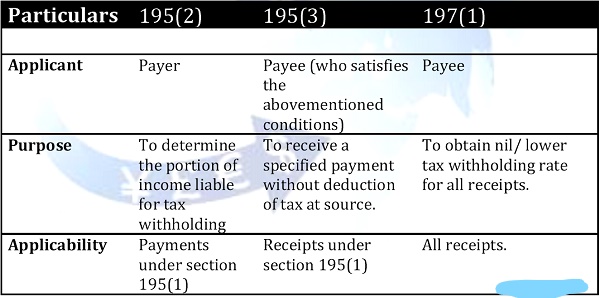

It seems that the procedure laid down for the application and issuance of certificates U/s 195(2) or 195(3) of the ITA (relevant for Indian branches of foreign banks, foreign reinsurance companies, foreign companies, etc.) continues to be as set out in the order issued on 31 March 2020. An application must be submitted by e-mail, and an application should also be given by e-mail. In case Otherwise, TDS @ 10% shall be deducted where applications are pending but not processed.

As per the Notification, it is noted that the extension of existing certificates is for certificates issued pursuant to section 197/206C of the Act through TRACES, while certificates issued pursuant to section 195(2) and 195(3) of the Act for the year 2020-21 must still be applied by e-mail and certificates issued by e-mail.

Current certificates under 197 of the Act for the financial year 2019-20 include details of the deductor as well as amounts paid during the relevant financial year and lower tax rates. In the light of the notification, given that the current certificates are extended until 30 June 2020 or earlier, the amount covered by the deductor for the year 2020-21 should be regarded proportionate to the amount covered by the certificate for the year 2019-20 for that particular deductor.

The prompt confirmation of the CBDT and the extension of an existing zero or lower Tax Deducted at Source/ Tax collected at Source certificates for FY 2019-20 to 30 June 2020 for FY 2020-21 is much sought after relief given to taxpayers in the volatile situation caused by the pandemic and the consequent lockdown.

For payments made to non-residents (including foreign companies) who have a permanent establishment in India, Payment tax will be deducted @ 10%, including surcharge and cessation, on payments until 30/06/2020 of Financial Year 2020-21, or on the disposal of their applications, whichever is earlier.

The explanation is still expected from the department for the limitation of the certificate, as it may be in circumstances where the limit of the Financial Year 2019-20 lower TDS certificate has been exhausted. In all those cases, the degree to which the certificate limit is finalised by the department is still anticipated.

WHAT IS DIFFERENCES BETWEEN SECTIONS 195(2), 195(3) & 197(1)

GST Updates:

INPUT CREDIT AVAILABILITY

Read more about: All about GST Offenses, Penalties, and Appeals

Key Due Dates:

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

Understanding Form 16, Form 16A & Form 26AS: A Complete Guide for Taxpayers When filing your Income Tax Return (ITR),… Read More

CFO Cum whole-time director? ROC Gwalior Says No in EKI Energy Services Case Corporate governance is built on the principle… Read More

Toughest Exams in India: More Than a Test of Knowledge, A Test of Character Every year, millions of students and… Read More

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

{kind=link}

{kind=link}