Form 15CA and Form 15CB are the forms required to be filed by an NRI for undertaking foreign remittances or payments outside India. Thus, whenever a person is required to make any remittance or payment to a non-resident outside India,

The remitter is liable to deduct some amount of income tax thereon. Since the remittance is made through a Bank on behalf of its customer, it becomes difficult for a bank to determine whether tax has been deducted or not.

The authorized banker cannot remit money unless and until the remitter uploads form15CA and 15CBby logging onto the tax department’s website, as per RBI regulations.

What is the purpose of Form 15CA? The remitter makes a declaration on Form 15CA regarding payments to Non-Residents. What is the purpose of Form 15CB? Form 15CB is a type of certificate issued by a Chartered Accountant that confirms if payment is taxable in India and whether the appropriate tax has been paid before remitting cash to a Non-Resident.

To keep a check on the same, a course of action has been prescribed, involving the furnishing of Form 15CA and a certificate of a Chartered Accountant in Form 15CB. Both Forms 15CA and 15CB are available for download online.

DOCUMENTS REQUIRED FOR FORM 15CB ISSUANCE

List of Documents required for issuing form 15CB

Copy of invoice on basis of which payment is to be made

Details of bank account from which payment is to be made

Copy of No PE Declaration from Non-Resident ( if applicable)

Scan Copy of PAN card of Remitter

Digital signature of Remitter.

LIST OF INFORMATION REQUIRED FOR ISSUING FORM 15CA AND CB

Below details/Information are usually needed to prepare & submitting forms 15CA & 15CB:

Remitter name

Name and recipient Address/ Remittance Beneficiary

Remitter TAN

PAN card number of the recipient of Remittance

Nation to which remittance made

Remitter PAN

Currency in which remittance made

Bank name from which transferring money

Branch Name of Bank making remittance

Seven digit code – BSR Code of Bank Branch making remittance

Amount to be transferred in INR Rupees

Amount of remittance in foreign currency

Expected Proposed date of remittance

TDS amount in Indian Rupees

Rate of TDS as per Income Tax Act

The actual amount of remittance after TDS in foreign currency

The actual amount of remittance after deduction of Tax at Source in Indian currency

Date of TDS

Kind/nature of remittance

If the remittance is net of tax, whether tax payable has been grossed up. give computation of grossing up

Email address of remitter

Telephone of remitter with STD code

Email ID of the recipient of remittance

Telephone number of the recipient of remittance

TDS amount in foreign currency

FILING OF FORM 15CA AND FORM 15CB

www.carajput.com: Form15CA &15CB

The person requiring payment to be made to a Non-Resident shall furnish Form 15CA. the Part of Form 15CA be identified on the following basis –

PARTS OF FORM 15CA

PARTICULARS

PART A

INFORMATION BE PROVIDED UNDER THIS PART, WHERE THE AMOUNT OF PAYMENT OR AGGREGATE OF SUCH PAYMENTS MADE DURING THE FINANCIAL YEAR DOES NOT EXCEED RS. 5 LAKHS. WHERE SUCH A FORM IS FILED, FORM 15CB IS NOT REQUIRED TO BE OBTAINED.

PART B

INFORMATION BE PROVIDED UNDER THIS PART, WHERE THE AMOUNT OF PAYMENT OR AGGREGATE OF SUCH PAYMENTS MADE DURING THE FINANCIAL YEAR EXCEEDS RS. 5 LAKHS, DETERMINED AFTER OBTAINING THE CERTIFICATE FROM THE ASSESSING OFFICER UNDER SECTION 197 OR AN ORDER PASSED BY THE ASSESSING OFFICER UNDER SECTIONS 195(2) OR 195(3).

PART C

INFORMATION BE PROVIDED UNDER THIS PART, WHERE THE AMOUNT OF PAYMENT OR AGGREGATE OF SUCH PAYMENTS NOT INCLUDED IN PART A, MADE DURING THE FINANCIAL YEAR EXCEEDS RS. 5 LAKHS, AND THE SAME IS FILED AFTER OBTAINING A CERTIFICATE IN FORM 15CB FROM A CHARTERED ACCOUNTANT.

PART D

INFORMATION BE PROVIDED UNDER THIS PART, WHERE THE AMOUNT OF PAYMENT IS NOT CHARGEABLE UNDER THE PROVISIONS OF THE INCOME TAX ACT. OTHER THAN REFERRED TO IN RULE 37BB (3).

STEPS FOR FILING FORM 15CB

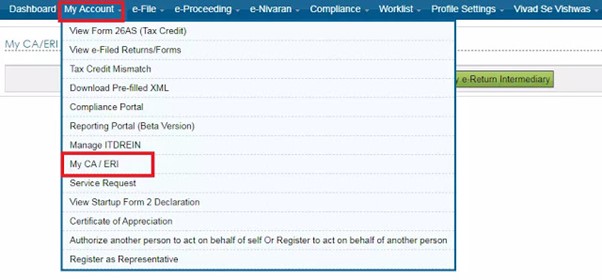

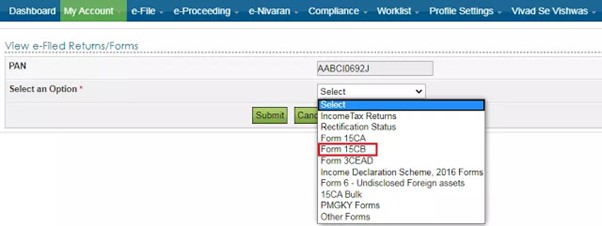

The person requiring to ma remittance, shall log in to the e-filing portal of the IT department, and look for the ‘My Account’ tab.

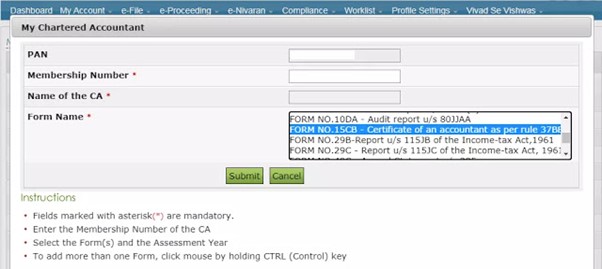

Under the drop-down, select ‘My CA/ERI’ and click on ‘My Chartered Accountant’.

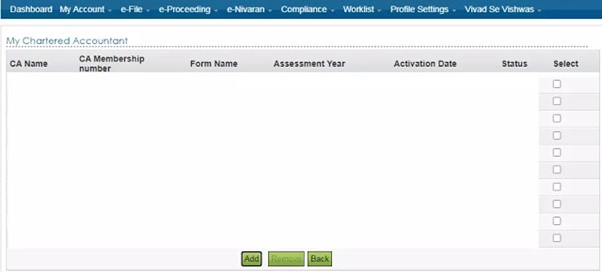

After this, click on the ‘Add’ tab and then provide for the ‘Membership Number’ of the Chartered Accountant, who will be certifying under Form 15CB.

Once the membership number is entered, the name of the CA will be auto-populated, and after clicking on the add button to add that CA to their account.

www.carajput.com: Form15CA &15CB

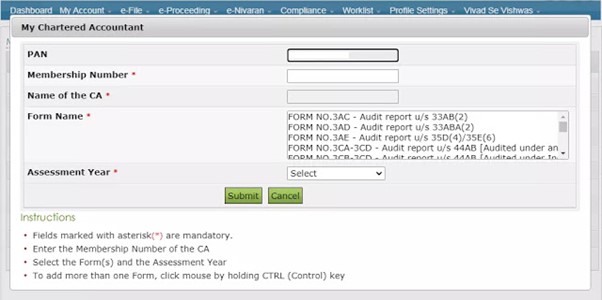

After adding the CA, select the ‘Form No. 15CB – Certificate of an accountant as per Rule 37BB’ as provided under the Forms available on the portal and click on Submit.

Once the Form 15CB is selected, the ‘Assessment Year’ provided on the page will disappear. After this, the CA shall file Form 15CB on behalf of his client.

The following steps are followed for filing Form 15CA –

First, the NRI needs to log in to Income Tax Web Portal.

Create a new user account with the help of a PAN card and other proofs.

Then visit the E-File option and select Form 15CA.

Form 15CA will have certain steps to be followed.

Fill in the required details in all the Parts from A to D.

On completing the information, submit the form by clicking on the submit button.

On successful filing, the NRI is required to submit a copy of the filed form with their bank.

The bank official will sign on the same and thereby complete the procedure.

CBDT enables electronic filing of forms-ITR 1, 4S, 15CA, 15CB & 15CC; other ITR forms to be enabled shortly, CBDT press release

SITUATIONS IN WHICH FORMS 15CA AND 15CB ARE NOT NECESSARY

No forms 15CA CB are required under Rule 37BB of the Income Tax Rules in certain circumstances. These are listed below:

Where Payment in Advance is Required for Import

Where Payment is Made for Import-Invoice Settlement

In the case of diplomatic missions’ imports

When it comes to Intermediary Trade,

Where the import value is less than Rs. 5,00,000/-

SITUATIONS, IN WHICH FORMS 15CA 15CB ARE NOT REQUIRED.

When a remittance is not subject to taxation.

Form 15CB is not required if the total value of remittances throughout the financial year does not exceed Rs. 5 lakhs.

In the case where the certificate of lower/no deduction/ order is made from the Jurisdictional Assessing Officer under sections 195(2), 195(3), and 197 of the Income Tax Act.

PENALTY IN CASE OF DEFAULT:

In the event of a default, there will be a penalty. A penalty of Rs. 1 lakh shall be imposed if forms 15CA/CB are not filed on time. Is it possible to remove Forms 15CA and 15CB once they have been submitted? Within seven days after submitting the online form, 15CA can be withdrawn. However, there is currently no way to withdraw Form 15CB.

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}