Page Contents

BRIEF INTRODUCTION

As per the Union Budget 2021, which was presented on 1st February 2021, the following provisions were inserted in respect of penalty and appeal –

It is to be noted that for the effective implementation of any tax law, there is a need for having a strict action against tax offenders. Thus, to have effective implementation of India’s new GST tax regime, the government implemented a three-pronged approach involving interest, monetary penalties, and prosecution.

Where any offense has been committed, a penalty is required to be paid under GST laws. The penalty depends upon the various parameters –

It can be seen that the amount of penalty in GST regime has increased substantially than that in the earlier tax laws. This shows that the government is pretty much serious regarding proper GST compliance. However, the government has provided for certain relief and exemption for penalty as well. These are as follows –

The default related to late filing attracts late fees. The amount being Rs. 100 per day of default. The said amount is applicable for each type of GST, thus the effective rate comes out to be Rs. 200/day, subject to the maximum of Rs. 5,000. However, no late fee is levied on IGST.

Apart from the late fee, an interest @ 18% per annum is also required to be paid.

Where the GST return is not filed, the provision for subsequent filing of other returns is not provided. Thus, late filing leads to a piling of burden, resulting in heavy fines and penalty.

Under the GST Act, the inspection can be initiated where, the Joint Commissioner of SGST/CGST, have the reasons to believe that to evade tax, a person has suppressed any transaction or claimed excess input tax credit. In such a case, the Joint Commissioner can authorize any other officer, to inspect places of business of the suspected evader.

The Joint Commissioner has the authority to order for a search. However, the same can be ordered, where he has the reasons to believe that –

Under this, the person carrying the goods of value exceeding Rs. 50,000 is required to carry the following documents:

The proper officer can intercept goods in transit and have an inspection of the goods and the documents. Where the goods are found to be in contravention of the GST Act, such goods, related documents, and the vehicle will be seized. And the goods be released only on payment of tax and penalty.

The following defaults lead to the confiscation of goods and/or conveyances and involves a penalty of Rs 10,000 or an amount equal to the tax evaded.

It is to be noted that the prosecution provisions are much harsher than the monetary penalty.

PERIOD OF IMPRISONMENT

| TYPE OF OFFENCE | AMOUNT OF DEFAULT. | PERIOD OF IMPRISONMENT | APPLICATION OF FINE |

| CERTAIN OFFENSES SPECIFIED IN THE ACT | EXCEEDING RS 500 LAKHS | UP TO 5 YEARS AND NON-BAILABLE | APPLICABLE |

| CERTAIN OFFENSES SPECIFIED IN THE ACT | EXCEEDING RS 200 LAKHS UP TO RS 500 LAKHS | UPTO 3 YEARS | APPLICABLE |

| ANY OTHER OFFENSE | EXCEEDING RS 100 LAKHS UP TO RS 200 LAKHS | UPTO 1 YEAR | APPLICABLE |

| ASSISTS THE COMMISSION OF CERTAIN SPECIFIED OFFENSES | UP TO 6 MONTHS | APPLICABLE | |

| REPETITION OF OFFENSE

| UPTO 5 YEARS | APPLICABLE |

Compounding of offenses is a method to avoid litigation. Where any prosecution for an offense is pending in a criminal court, the accused is required to appear before the Magistrate at every hearing through an advocate. Such an activity involves time and money.

Now, in the compounding, the accused is not required to appear personally and can discharge the liability by making the payment of compounding fee that is capped to the maximum fine as applicable under GST.

Thus, compounding will save time and money. However, the compounding under GST shall not be available where the amount involved exceeds 1 crore.

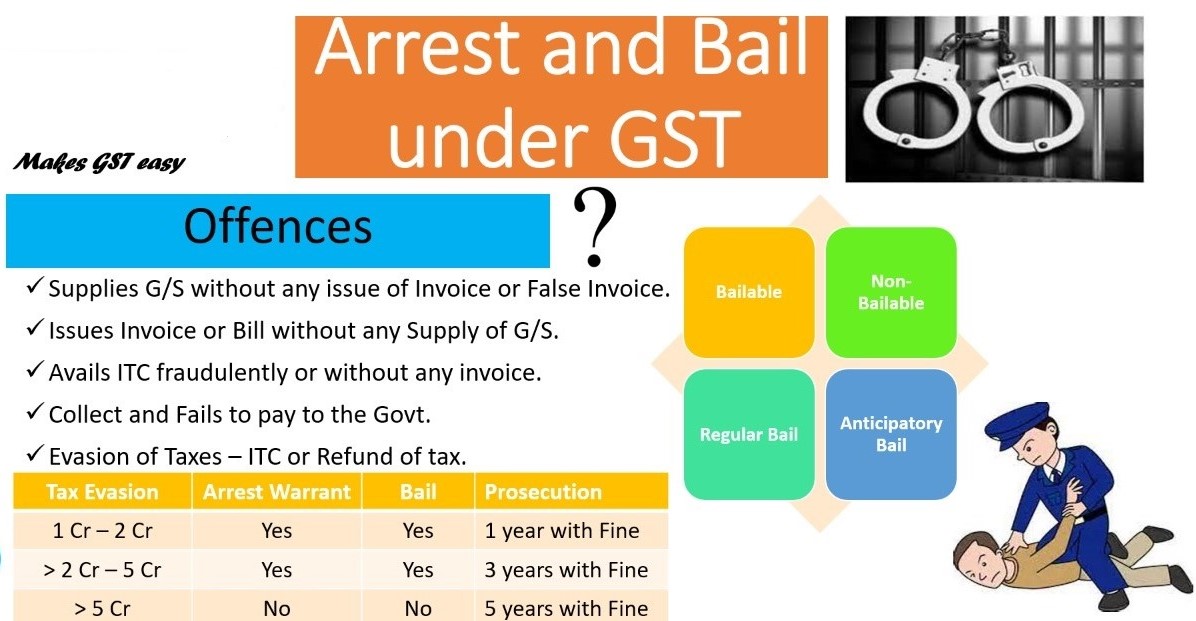

Prosecution involves conducting of legal proceedings against someone in respect of a criminal charge. Where a person with a deliberate intention to fraud, commits an offence, shall be liable to prosecution under GST, and shall face criminal charges. Some of these cases are as follows –

Where the Commissioner of CGST/SGST believes that a person has committed a certain offense, he can make an order for the arrested under GST Act. The arrested person shall be informed about the grounds for the arrest and once arrested, the said person be appeared before the magistrate within 24 hours of arrest.

GST Appellate Tribunal age limit raised to 70, ensuring longer service for taxpayers.

APPEALS

Where a person is unhappy with any decision or order passed against him under GST can apply for the appeal against such decision. The first appeal can be made against the order of the adjudicating authority and the same be filed with the First Appellate Authority.

Where the aggrieved person is not happy with the decision of the First Appellate Authority they can appeal to the National Appellate Tribunal, if still not satisfied, they can go to the High Court, and if still unsatisfied, the last resort is to appeal to the Supreme Court.

To avoid such a long process of appeal and litigation, the taxpayer may apply for the advance ruling under GST, where they can seek clarification from GST authorities on GST treatment before starting the proposed activity.

Popular blog:-

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}