Page Contents

Under the new provisions, implemented by the Income Tax Department, some sought of relief has been provided to small taxpayers, wherein, instead of undertaking the tedious job of maintenance of books of account and their auditing, they can apply for presumptive taxation scheme under sections 44AD, Section 44ADA and Section 44AE.

Presumptive taxation scheme related to providing relief to small taxpayers. Any small taxpayer whose turnover is less than Rs 2 crores shall be eligible for such a scheme. To facilitate the running of businesses without any burden due to excessive compliance-related requirements, Section 44AD was introduced in the Income Tax Act.

Under this section, the assesses can declare their income at the prescribed rate and be relieved from the requirement of maintaining books of account.

This relaxation would also involve non-requirement of getting the accounts auditing, thus saving their cost and time. Businesses that enroll for taxation under the presumptive taxation scheme shall compute their income on an estimated basis, as provided under Section 44AD.

The small taxpayers can avail of the following presumptive taxation scheme under the Income-tax Act –

The entity that shall be enrolled under the scheme shall be a business that may differ based on the nature and size of its operations. Some of the common forms of business are –

It is generally advised that the entity should be a company, since by forming a company, there is a separate legal entity, due to which the company can have its PAN and same be used to file a separate tax return.

Also read: Legal Compliance Audit service in India

For an entity to pay tax under this scheme shall follow the following conditions –

The following businesses are not eligible to apply for the presumptive scheme under section 44AD –

Where the business satisfies the eligibility criteria, they would be required to mandatorily maintain proper books of accounts where –

In any of the 3 financial years immediately preceding the current financial year.

However, in the case of individuals and HUF, the above provisions have been further relaxed and they would be required to maintain proper books of accounts where –

In any of the three financial years immediately preceding the current financial year.

Where proper books of accounts are not maintained by the persons, requiring to do so, shall be liable to a penalty of up to Rs 25,000.

Businesses having gross receipts exceeding Rs 1 crore in a financial year, are required to compulsorily have tax audits. The due date for filing the tax audit report has been provided as 30th September of the relevant assessment year. The report is filed electronically using Form 3CD.

It is also provided that under the normal circumstances, any revision to tax audit report is not possible, however, in some cases where the accounts are subject to any revision, the tax audit report can be revised.

The person opting for presumptive taxation under section 44AD, shall declare their income @ 8% for non-digital transactions or 6% for digital transactions on the gross receipts or turnover.

Suppose there is a company named Ram Traders have gross receipts of Rs 1 Crore for FY 2020-21 and they do not maintain books of accounts. Ram traders is looking to opt for presumptive taxation. In the above Rs 1 crore receipts, receipts worth Rs. 70 Lakhs were received through non-digital transactions while the remaining Rs. 30 Lakhs was received through digital transactions.

The computation of under the head of Income from Business and Profession would be –

For non-digital transactions: 8% of 70,00,000 = Rs. 5,60,000

For digital transactions: 6% of 30,00,000 = Rs. 1,80,000

Income under the head “Business or Profession” will be = Rs 7,40,000

Where any individual of HUF carries on a business and opts for payment under a presumptive taxation scheme, shall file their annual return of income in form ITR 3.

It is provided that the person eligible to claim the benefit under Section 44AD, shall avail the same at any time during the relevant financial year. And also, such a person can opt out of the scheme at any point in time.

However, where a person opts out from the scheme of Presumptive Taxation under Section 44AD, the same shall not be eligible to avail the scheme for the next 5 financial years.

| PARTICULARS | PRESUMPTIVE TAXATION UNDER SECTION 44AD |

| AY 2019-20 | OPTS FOR PRESUMPTIVE TAXATION |

| AY 2020-21 | DOES NOT OPT FOR PRESUMPTIVE TAXATION |

| AY 2021-22 – AY 2025-26 | INELIGIBLE FOR PRESUMPTIVE TAXATION |

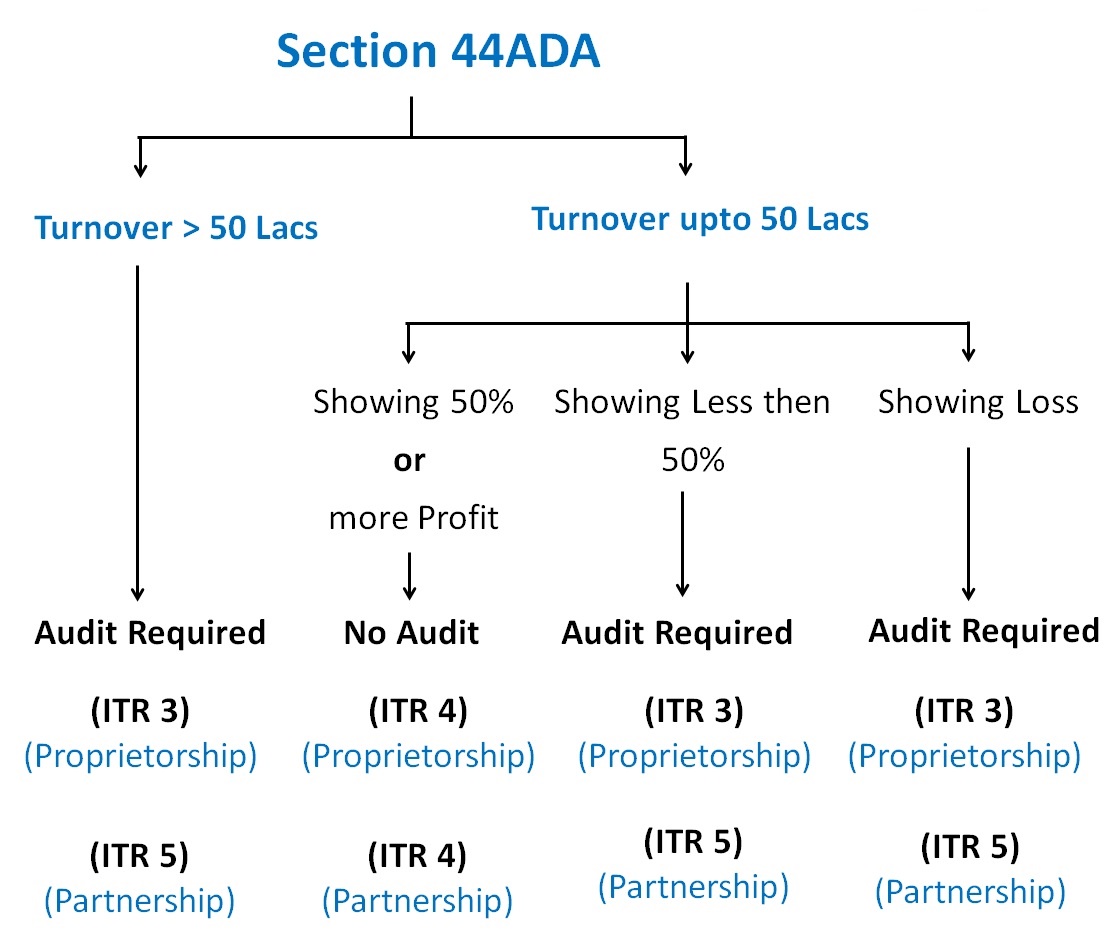

The benefit under this scheme shall be applicable to professions registered in India. Professionals having total gross receipts of up to Rs. 50 Lakhs in a financial year, shall be eligible to claim benefit under this Section with effect from Financial Year 2016-17.

Under this scheme, the taxable income of the person shall be determined at a flat rate of 50% of the total receipts.

The following professions be eligible to avail the benefit of presumptive taxation under section 44ADA –

The scheme includes only resident Individual, HUF and Partnership firms only and exclude Limited Liability Partnership firm. The person opting under this scheme, shall be allowed claim deductions under Section 30 to 38. However, no other deduction related to expenses shall be allowed.

A. PROFESSIONALS CARRYING SPECIFIED PROFESSIONS

Professionals carrying the above-mentioned professions would be required to maintain books of accounts in accordance with Rule 6F, provided their annual gross receipts exceeds Rs. 1.5lakhs in any of the 3 immediately preceding financial years.

Where the person carries the profession other than those discussed above, the same would be required to maintain proper books of accounts, provided the total annual income exceeds Rs. 2.5 lakhs or annual gross receipts exceeds Rs. 25 lakhs in any one of the immediately preceding 3 financial years.

The total gross receipts be determined by reducing the amount of expenses related to the profession like salary to any employee, rent for the premises of carrying profession, internet expenses, mobile expenses, official travel, lunch expenses etc.

Suppose, Arun is an interior designer and is having a gross revenue of Rs 40 lakhs for the FY 2020-21. The following expenses were incurred during the year –

| PARTICULARS | AMOUNT (IN RS) | |

| GROSS RECEIPTS | 40,00,000 | |

| LESS – | EXPENSES RELATED TO PROFESSION | |

| INTERNET AND MOBILE | 50,000 | |

| SALARY | 5,00,000 | |

| RENT | 2,00,000 | |

| LUNCH EXPENSES | 50,000 | |

| TRAVEL EXPENSES | 1,00,000 | |

| NET RECEIPTS | 31,00,000 |

However, in the case of presumptive taxation, the income would 50% of Rs 40 lakhs = Rs 20 lakhs which would be lower than that as determined above.

The person carrying a professional, shall file ITR 3, as their annual return and the same be filed on and before 31st July of the Assessment.

Professionals shall be liable to tax audit, where their gross receipts exceed Rs 25 lakhs during any financial year. In case of any failure, a monetary penalty of up to 0.5% of the gross receipts or Rs 1.5 lakhs whichever is lower, shall be applied.

It is provided that any person eligible to the scheme under section 44ADA, can opt in and opt out from the scheme at any point of time, without any 5-year restriction, as applicable in case of section 44AD.

| PARTICULARS | PRESUMPTIVE TAXATION UNDER SECTION 44ADA |

| AY 2019-20 | OPTS FOR PRESUMPTIVE TAXATION |

| AY 2020-21 | DOES NOT OPT FOR PRESUMPTIVE TAXATION |

| AY 2021-22 | ELIGIBLE TO OPT FOR PRESUMPTIVE TAXATION. |

Freelancers shall also be eligible for presumptive taxation, provided they are involved in any of the specified or non-specified professions.

Such a scheme can be availed by any person engaged in the business of plying, hiring or leasing of goods carriages and the said business does not involve vehicles exceeding 10 goods vehicles at any point of time in a financial year.

In order to compute tax under this section, the following provisions be followed –

It is to be noted that no relaxation in respect of advance tax payment be provided to persons opting for a presumptive taxation scheme under section 44AE.

It is provided that the persons opting for the presumptive scheme under this section, shall maintain proper books of accounts in relation to income, expenses, assets, and liabilities of their business since these financial records would be essential to understand the performance of their business.

It is provided that no credit for depreciation be allowed to persons opting for this scheme. Whenever a person purchases a capital asset, the benefit of the same is expected to last for more than a year.

Every year a small portion of its cost is expensed and is allowed to be reduced from your income. This amount of expense being charged every year is known as depreciation.

Tax audit would be required to be undertaken by a Chartered Accountant where –

Step 1: Identify Nature of Income

Step 2: Determine Eligibility

| Particulars | Section 44AD | Section 44ADA |

|---|---|---|

| Applicable To | Businesses | Specified Professionals |

| Eligible Persons | Individual, HUF, Firm | Professionals |

| Income Presumed | 6%/8% of Turnover | 50% of Gross Receipts |

| Books of Account | Generally not required | Generally not required |

| Tax Audit | Usually not required | Usually not required |

| Turnover/Receipt Limit | Up to INR 2/3 Crore | Up to INR 75 Lakh* |

*Subject to applicable conditions and amendments. Key Takeaway is a simple formula to remember:

Understanding these provisions correctly can significantly reduce compliance burden, simplify record-keeping, and help eligible taxpayers opt for presumptive taxation while remaining fully compliant with the Income-tax Act.

Popular blog:- Tax Audit Check List

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}