Page Contents

This is the hug misunderstanding in the minds of Indian citizens. The following items explain some of the issues:

1) FY 2019-20 is not at all extended until 30 June, only the date for other compliances is extended.

2) Late returns or revised returns for the FY 2018-19 can be reported before 30 June.

3) In the financial year 2019-20, salary is taxable only until 31 March and not until 30 June, i.e. the taxability of salary for the full year is considered only until 31 March.

4) Deductions under 80C, 80D, etc. can be obtained by saving before 30 June.

5) New LIC, medical, PPF, NPS, etc. policies adopted by 30 June would be deductible during the year 2019-20.

6) Payment of the premium of the old policies of LIC, medical, PPF, NPS, etc. due by 31 March may be claimed as deduction even if it is paid by 30 June.

7) Residential loan interest is eligible for deduction on an accrual basis, and interest accumulated before 31 March should be available for deduction in the financial year 2019-20. However, payments due until 31 March will be reported as deductions if they have been paid until 30 June.

30.06.2020 is the extended date of the Vivad Se Vishwas Scheme requirement for the settlement of cases pending with the appellate authorities without extra charge. Note-100 percent exemption from tax and fine. Only the tax amount in dispute must be paid.

07.05.2020 is the due date for the collection of TDS / TCS for the month of April 2020. Note-Interest at 0.75 percent p.m. Or half of it will be paid in case of delay until 30.06.2020.

30.06.2020 is the current due date for Opt-in Composition Scheme by Current Taxpayers during the year 2020-21 by filing Form GST CMP-02. Note-Taxpayers intending to transfer Ought NOT to register GSTR-3B or GSTR-1 for the months of April, May, and June 2020.

Current Composition Taxable Citizen to file CMP-08 for Q4 (2019-20) by 07.07.2020 instead of 18.04.2020 and file GSTR-4 for FY 2019-20 by 15.07.2020 instead of 30.04.2020.

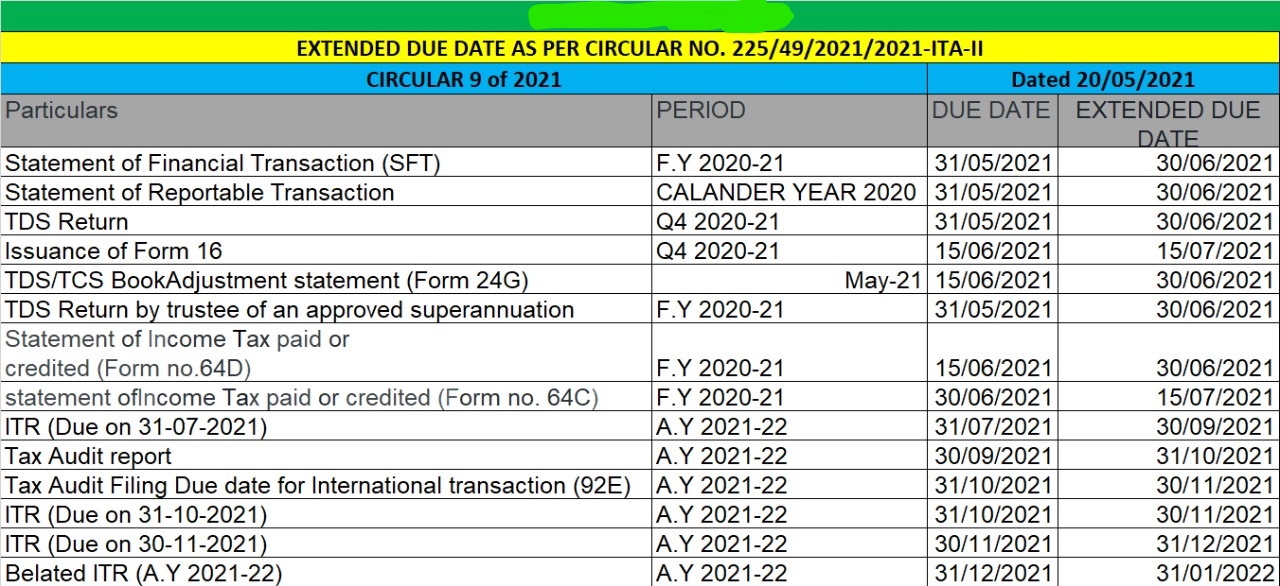

30.06.2020 is the due date for the TDS / TCS returns to file for Q4 (F.Y. 2019-20).

CBIC extended the filing dates of GSTR-5 (NRTP), GSTR-6 (ISD), GSTR-7 (TDS Deductor), GSTR-8 (TCS Collector) for the months of March, April, and May 2020 to 30.06.2020.

30.06.2020 is the due date of the original/revised income tax return during the year 2018-19.

MCA has declared a “Moratorium Period” from 01.04.2020 to 30.09.2020 for the filing of ROC Forms and no further fees will be paid during this time due to the late submission of any form submitted during this time.

MCA extended the deadline for registration at the Independent Director Databank Registry for registered Independent Directors from 29.02.2020 to 30.04.2020. * * Update to Rule 6 of the Code of Practice of the Board.

ESIC has expanded to 15.05.2020 the due date of payment of ESI Donation for the months of Feb, 20, and Mar.

EPFO has increased the payment deadline of PF Donation for the month of March from 20 to 15.05.2020.

Income Tax & Goods and services tax – Extension of Due Dates as per Press Release dated 30.12.2020.

| Nature of Taxpayer | Extended Due Date of ITR | Extended Due Date of Audit Reports (Tax Audit Report, Transfer Pricing Report etc.) |

| Taxpayer (including their partners) who are required to get their accounts audited and Companies | 15th February 2021 | 15th January 2021 |

| Taxpayer who are required to furnish report in respect of international/specified | 15th February 2021 | 15th January 2021 |

| Other Taxpayers | 10th January 2021 | – |

Last date for making a declaration under Vivad Se Vishwas Scheme has been extended to 31st January 2021

| Particular | Extended Due Date |

| Date of filing GSTR9/9C for FY 2019-20- | 28th February 2021 |

Due date for filing GSTR-9/9C for FY 2018-19 remains same i.e. 31st December 2020 till any further notification (For details, please refer Press Release dated 30th December 2020)

More read:

Also, read the relevant blog;

Post by Rajput Jain & Associates

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}