Page Contents

E-way bill is an electronic way bill for movement of goods which can be generated on GSTN portal. E-way bill contains the details of transported goods besides the name of consignor and consignee of such goods.

It is the evidence of realness of supply of goods from one place to another.

This is required to be generated for consignment of goods of value exceeding Rs 50000. (Generating an e-way bill for consignments valuing less than Rs 50000 is optional)

In relation to supply

For reasons other than supply

For inward supply from an unregistered persons

Validity of E-Way Bill

| Distance | Valid for |

| Upto 100 km | 1 day |

| 100 km or more but less than 300 km | 3 day |

| 300 km or more but less than 500 km | 5 day |

| 500 km or more but less than 1000 km | 10 day |

| More than 1000 km | 15 day |

Transport of goods as specified in Annexure to Rule 138 of the CGST Rules, 2017

Goods being transported by a motorless conveyance;

Product being transported from the port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs

In respect of movement of goods within such areas as are notified under rule 138(14) (d) of the SGST Rules, 2017 of the concerned State;

Consignment value less than Rs. 50,000/

Goods worth more than Rs.50, 000 are transported from one place to another an e-way bill is required.

In case goods are transported without an e-way bill, the goods can be seized by a GST officer and penalty could be levied.

Read more about: What is core Business Activity GST

Read more about: All about GST Offenses, Penalties, and Appeals

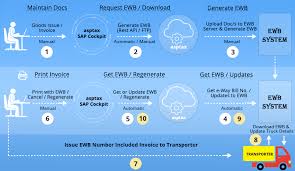

Documents Required for Transport under GST

In addition to the GST E-Way Bill, a person-in-charge of conveyance of goods is required to carry the following documents for inspection by authorities at any time:

Invoice or bill of supply or delivery challans and invoice reference number from the GST common portal, obtained by uploading a copy of the GST tax invoice issued in FORM GST INV-1.

Copy of the e-way bill or the e-way bill number, either physically or mapped to a Radio Frequency Identification Device (RFID) embedded onto the vehicle. in such manner as may be notified.

Major improvements over the last set of rules, as approved by the Council now, are as follows:

Calculation while computing GST Interest & Late fee The Goods and Services Tax Interest & Late Fee Calculator helps taxpayers… Read More

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

{kind=link}