Page Contents

In the Finance Bill 2021, government proposed to insert two new sections, namely, Section 206AB and Section 206CCA under Income Tax Act, 1961.

These sections would provide for application of a higher rate of TDS and TCS, in respect of the deduces who did not file their Income Tax Returns related to the 2 FY’s immediately preceding the FY in which tax is required to be deducted or collected.

The Govt proposed to insert new section 206AB & section 206CCA in the Income Tax Act, 1961, which will provide a special provision.

The proposed rate for deduction of TDS under this section will, higher of the following –

| Under Section 206AA- Rate of TDS when a person fails to file of Permanent Account Number: Rate of TDS U/s 206AA Higher of- | Under Section 206AB- Rate of TDS when a person fails to file 2 years ITR’s: Rate of TDS U/s 206AB Higher of- |

| AT RATE, AS SPECIFIED IN THE RELEVANT PROVISION. | AT TWICE THE RATE, AS SPECIFIED IN THE RELEVANT PROVISION OF THE ACT. |

| 2 time of rate or Rate in Force . | AT TWICE THE RATE OR RATES THAT ARE THERE IN FORCE. |

| AT THE RATE OF 20%. | AT THE RATE OF 5%. |

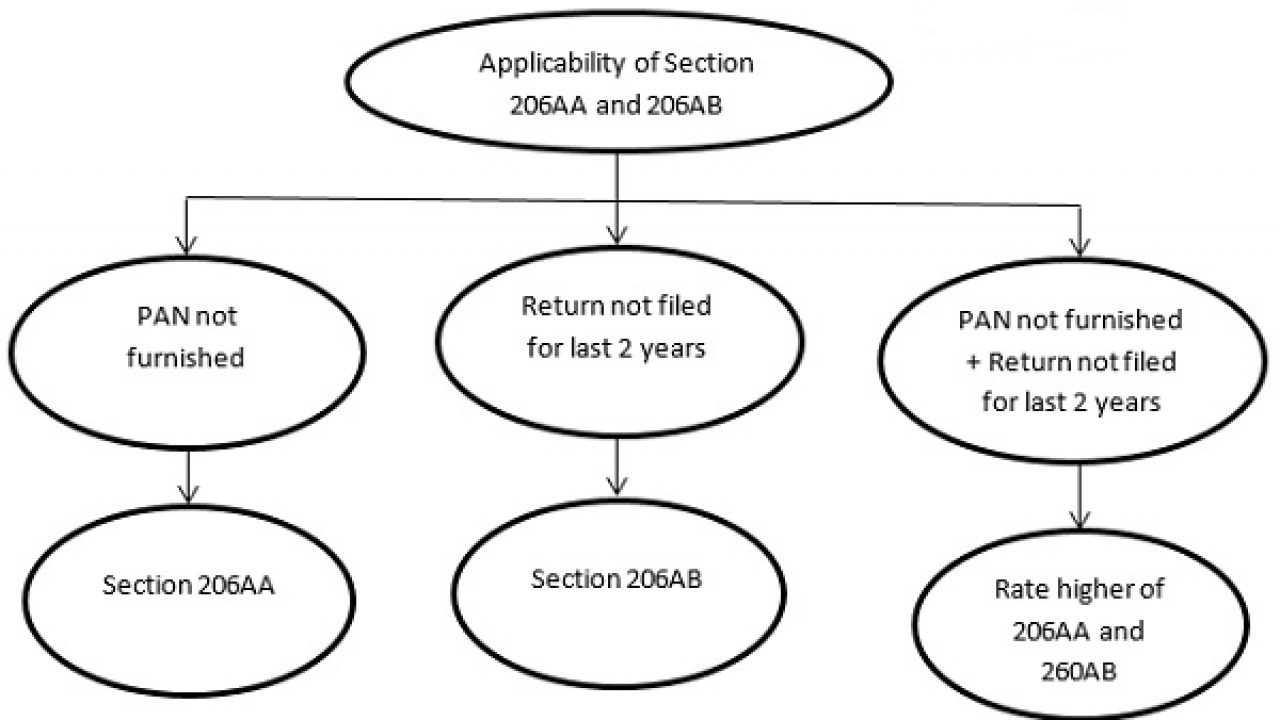

Under this situations according to U/s 206AB(2), Tax deducted at sources will be deducted at a higher rate from the below :

• TDS Rate determined according to section 206AA

• Rate of TDS determined according to section 206AB

| BASIS | SECTION 206AA | SECTION 206AB |

| APPLICABILITY | WHERE THE DEDUCTEE FAILS TO FURNISH THEIR PAN | WHERE THE DEDUCTEE FAILS TO FURNISH THE RETURN FOR A SPECIFIED PERIOD AND THE AGGREGATE AMOUNT OF TDS, TO BE DEDUCTED, DURING SUCH SPECIFIED PERIOD EXCEEDS THE SPECIFIED LIMIT |

| RATE OF TDS | HIGHER OF – · AT RATE, AS SPECIFIED IN THE RELEVANT PROVISION. · AT RATE OR RATES THAT ARE THERE IN FORCE. · AT THE RATE OF 20%. | HIGHER OF – · AT TWICE THE RATE. AS SPECIFIED IN THE RELEVANT PROVISION. · AT TWICE THE RATE OR RATES THAT ARE THERE IN FORCE. · AT THE RATE OF 5%. |

| EXCEPTIONS | WHERE THE INCOME IS RECEIVED BY A NON-RESIDENT INDIVIDUAL OR COMPANY – · INTEREST ON BONDS REFERRED UNDER SECTION 194LC. · SPECIFIED PAYMENTS AS REFERRED UNDER RULE 37BC. · INCOME IN RESPECT OF INVESTMENT IN CATEGORY I OR CATEGORY II AIFS AS REFERRED UNDER RULE 114AAB. | WHERE THE INCOME IS REQUIRED TO BE DEDUCTED UNDER THE FOLLOWING SECTIONS –

· SECTION 192 · UNDER SECTION 192A · SECTION 194B · UNDER SECTION 194BB · SECTION 194LBC · UNDER SECTION 194N

HOWEVER, THIS EXEMPTION SHALL NOT BE AVAILABLE TO A NON-RESIDENT, NOT HAVING A PERMANENT ESTABLISHMENT IN INDIA. |

| SPECIAL RATE OF TAX | A TAX @ 5% BE LEVIED, WHERE THE TAX IS DEDUCTIBLE UNDER SECTION 194-O AND SECTION 194Q. HOWEVER, WHERE TDS IS DEDUCTIBLE UNDER SECTION 192A, THE RATE SHALL BE THE MAXIMUM MARGINAL RATE APPLICABLE. | Not applicable |

There is no exception U/s 206AB even if the recipient person is ‘not liable’ to file Income tax Return:

It is provided, that the provisions of section 206AB, shall not apply on the amount on which TDS is required to be deducted under the following sections –

A person is said to be a specified person, where all the following conditions are fulfilled –

In case, a person is liable to higher rate of TCS, under the provision of both section 206CCA and Section 206CC, the tax shall be collected at the highest rate, as determined under both the section respectively.

There are big issue that emerge from section 206AB. New challenges in related to difficulty that deductor face to determine:

So, the main duty of collecting all needed details from the deductee can confine TDS to function with ease & can impose an additional burden.

| BASIS | SECTION 206CC | SECTION 206CCA | |

| Applicability of section 206AB | WHERE THE COLLECTEE FAILS TO FURNISH THEIR PAN. | WHERE THE COLLECTEE FAILS TO FURNISH THE RETURN FOR A SPECIFIED PERIOD AND THE AGGREGATE AMOUNT OF TCS, TO BE COLLECTED, DURING SUCH SPECIFIED PERIOD EXCEEDS THE SPECIFIED LIMIT | |

| RATE OF TCS | HIGHER OF –

· AT TWICE THE RATE. AS SPECIFIED IN THE RELEVANT PROVISION. · AT THE RATE OF 5%. | HIGHER OF –

· AT TWICE THE RATE. AS SPECIFIED IN THE RELEVANT PROVISION. · AT THE RATE OF 5%. | |

| EXCEPTION | ANY NON-RESIDENT NOT HAVING A PERMANENT ESTABLISHMENT IN INDIA | ANY NON-RESIDENT NOT HAVING A PERMANENT ESTABLISHMENT IN INDIA | |

| SPECIAL TAX RATES | TAX B

E LEVIED @ 1% WHERE IT IS COLLECTABLE UNDER SECTION 206C(1H). | Not applicable |

. Specified person |

A person is said to be a specified person, where all the following conditions are fulfilled –

Such amendment be made effective from 1st July 2021.

| HIGH RATE OF TDS ON NON-FILERS OF ITR UNDER SECTION 206AB | HIGH RATE OF TCS ON NON-FILERS OF ITR UNDER SECTION 206CCA |

| APPLIES WHEHRE THE DEDUCTEE FAILS TO FURNISH TO FURNISH THEIR ITR FOR 2 FINANCIAL YEARS, IMMEDIATELY PRECEEDING THE FINANCIAL YEAR IN WHICH THE TDS IS REQUIRED TO BE DEDUCTED. | APPLIES WHEHRE THE DEDUCTEE FAILS TO FURNISH TO FURNISH THEIR ITR FOR 2 FINANCIAL YEARS, IMMEDIATELY PRECEEDING THE FINANCIAL YEAR IN WHICH THE TCS IS REQUIRED TO BE COLLECTED. |

SPECIFIED PERSON –A PERSON IS SAID TO BE A SPECIFIED PERSON, WHERE ALL THE FOLLOWING CONDITIONS ARE FULFILLED –

| |

| EXEMPTED

WHERE THE INCOME IS REQUIRED TO BE DEDUCTED UNDER THE FOLLOWING SECTIONS –

· SECTION 192 · UNDER SECTION 192A · SECTION 194B · UNDER SECTION 194BB · SECTION 194LBC · UNDER SECTION 194N

HOWEVER, THIS EXEMPTION SHALL NOT BE AVAILABLE TO A NON-RESIDENT, NOT HAVING A PERMANENT ESTABLISHMENT IN INDIA. | EXEMPTED

WHERE INCOME IS RECEIVED BY ANY NON-RESIDENT NOT HAVING A PERMANENT ESTABLISHMENT IN INDIA |

RATE WOULD BE HIGHER OF –

| RATE WOULD BE HIGHER OF –

|

| THE SECTIONS WILL BE EFFECTIVE FROM 1ST JULY, 2021. | |

Also, under Section 194-IB, every Individual or HUF were required to deduct TDS on the amount paid as rent, provided their gross receipts or turnover in a particular financial year immediately preceding the financial year in which the TDS/TCS on rent paid is required to be deducted/collected, does not exceed Rs. 1 crore in case of a business and Rs. 50 lakhs in case of a profession.

However, where the PAN is not furnished by the deductee or collectee, tax be deducted/collected at the higher rates prescribed Section 206AA, but the same shall be subject to the maximum amount of TDS to be deducted.

But after the introduction of Section 206AB, an amendment be made to Section 194-IB, to provide for deduction of TDS at the higher rates in case of non-filing of ITR.

In case deductor fails to comply provisions of U/s 206AB, then below Consequences would possibly arise: –

Conclusion

Popular Articles :

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}