Page Contents

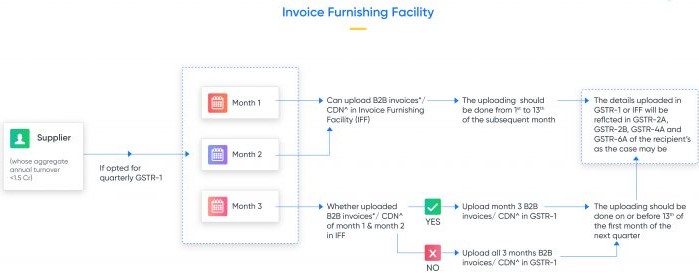

How to will provide documents in the Invoice Furnishings Facility (IFF) under the QRMP Scheme

The salient features of the Invoice Furnishing Facility are provided as under.

9B – Credit / Debit Notes (Registered) – CDNR

9A – Amended B2B Invoice – B2BA

9C – Amended Credit/ Debit Notes (Registered) – CDNRA

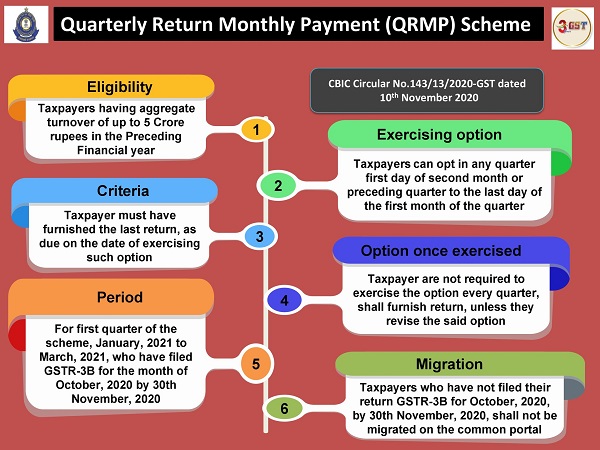

GST QRMP Scheme – Less Filing, Same Discipline

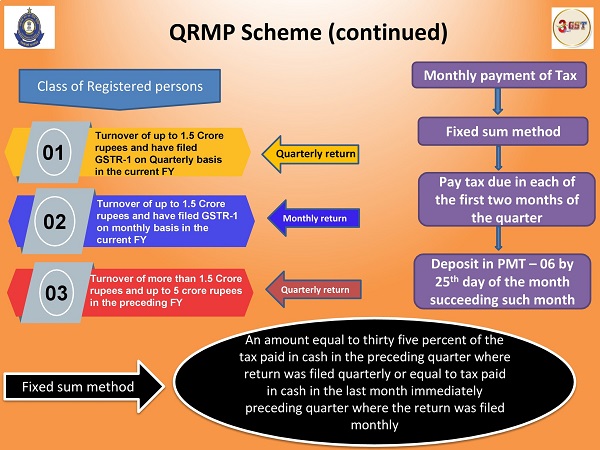

The taxpayer should first pay the tax in the form of GST PMT-06 by the 25th of the following month, for the first and second months of the quarter.

Taxpayers may pay their monthly tax liability in either the Fixed Sum Method (FSM) or the Self-Assessment Method (SAM).

The taxpayer should pay the amount of tax indicated in the pre-filled call in the form of GST PMT-06 for an equivalent amount to 35% of the tax paid in cash.

| S No | Type of Taxpayer | Tax to be paid |

| 1 | Who needed to file GSTR-3B quarterly for the last quarter | 35% of tax paid in cash in the preceding quarter |

| 2 | Who needed to file GSTR-3B monthly during the last quarter | 100% of tax paid in cash in the preceding month of the immediately preceding quarter |

The interest will be applicable as follows if the taxpayer opts for Fixed Sum Method (FSM):

| S No | Situation | Rate of Interest to be paid |

| 1 | GST Tax liability mentioned in pre-filled form GST PMT-06 is paid by 25th of the upcoming next month | Nil |

| 2 | GST Tax liability mentioned in pre-filled form GST PMT-06 is not paid by 25th of the upcoming next month | Eighteen percent of the tax liability (from 26th of the following month till the date of payment) |

| 3 | GST Tax liability for first 2 months is less than or equal to amount paid via pre-filled form GST PMT-06 | Nil |

| 4 | Final GST Tax liability for first 2 months is higher than tax amount paid via pre-filled form GST PMT-06, and such excess liability has been paid within quarterly GSTR-3B due date | Nil |

| 5 | The final GST Tax liability for the first 2 months is higher than the tax amount paid Via pre-filled form GST PMT-06, and such excess liability has not been paid within the quarterly GSTR-3B due date | Eighteen percent of the tax liability (from GSTR-3B due date* till the date of payment) |

*22nd or 24th of the month succeeding such quarter based on the state of the taxpayer.

The interest will be applicable as follows if the taxpayer opts for the Self-Assessment Method. The taxpayer has to pay interest @ 18% on the net tax liability which remains unpaid or paid beyond the due date for the first two months of the quarter.

Also Read :

The applicable late fee shall be paid as below if the quarterly GSTR-3B is not submitted within the deadline date, subject to a maximum late fees of INR 5k:

| Kind of the Act | Applicable late fee for every day of delay | Applicable late fee for every day of delay (if the ‘Nil’ tax liability) |

| CGST Act | Rs.25 | Rs.10 |

| SGST Act | Rs.25 | Rs.10 |

| IGST Act | Rs.50 | Rs.20 |

Notes : Clarification in respect of applicability of Dynamic Quick Response (QR) Code on B2C invoices and compliance of notification 14/2020- Central Tax dated 21st March, 2020- Clarification on applicability on QR Code Notification 14/2020

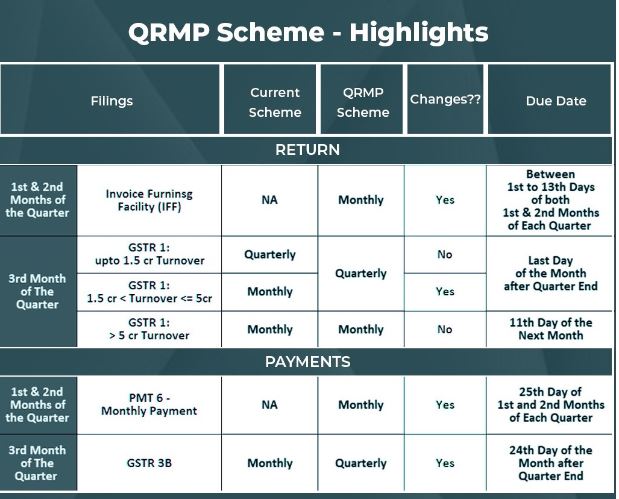

The deadline dates for submitting quarterly GSTR-3B has been notified as below :

| S No | GST Registration in States and Union Territories | Due Date |

| 1 | Karnataka, Goa, Lakshadweep, Daman and Diu, Maharashtra,Telangana, Kerala, Tamil Nadu, Puducherry, Andaman and Nicobar Islands, Chhattisgarh, Madhya Pradesh, Gujarat, Dadra and Nagar Haveli, and Andhra Pradesh | 22nd of the month upcoming Next such quarter |

| 2 | West Bengal, Jharkhand and Odisha, Uttarakhand, Haryana, Delhi, Rajasthan, Jammu and Kashmir, Ladakh, Himachal Pradesh, Punjab, Chandigarh,Uttar Pradesh, Bihar, Mizoram, Manipur, Tripura, Meghalaya, Sikkim, Arunachal Pradesh, Nagaland, Assam, | 24th of the month upcoming Next such quarter |

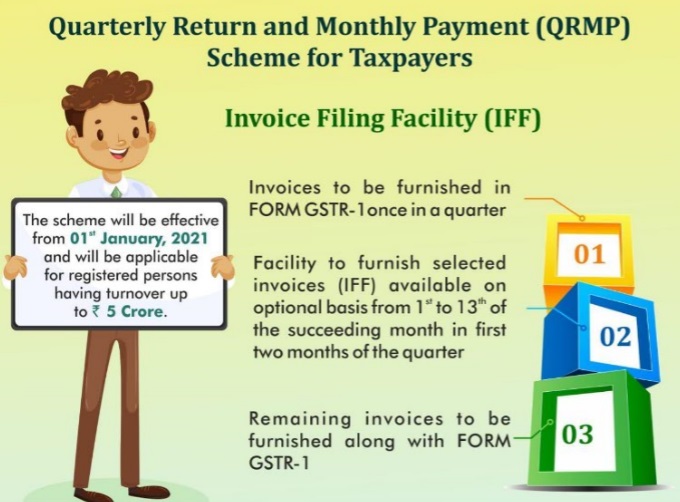

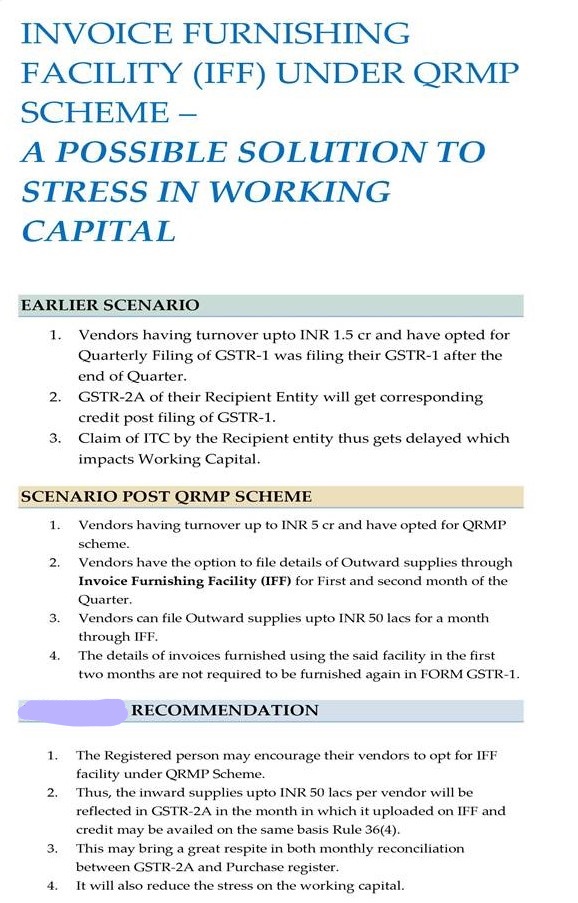

The potential benefits of the Invoice Furniture Facility are as follows:

This is an excellent strategy to help both small taxpayers and small taxpayers’ buyers. This facility will indirectly support small taxpayers to improve their businesses by providing faster ITC makes a claim to their buyers. Even so, this will raise the cost of compliance for them.

It is, therefore, necessary to make a comparison between the benefits of opting for IFF and the costs involved. It is decent to opt-in for this facility if a small taxpayer raises large amounts of B2B invoices in one quarter compared to B2C invoices.

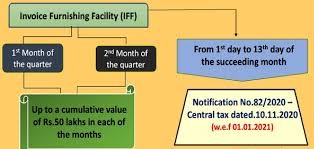

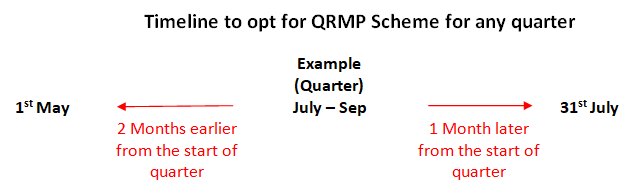

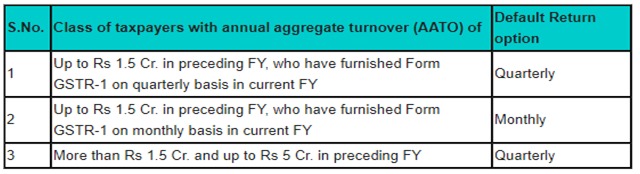

All taxpayers with Annual Total Sale up to INR 5 Crore have been given an option to file their Form GSTR-1 Statement & Form GSTR-3B return on a QTRLY basis. They also have an option to file B2B invoice details in Invoice Furnishing Facility (IFF) for months 1 & 2 (eg. Jan and Feb) of the quarter in order to pass on the credit, whereas the remaining invoices have to be declared in the QTRLY Form GSTR-1 of Month 3 (e.g. March). {With effect from 1st January 2021}

Our Recommendations: As we already know the limit of availing of the Input tax credit in respect of missed invoices have been reduced from 10% to 5% effective 01.01.2021. Thus, it is imperative for the large companies that have significant vendors under QRMP schemes that they should mandate their vendors to use the Invoice Furnishing Facility scheme. Basis the Invoice Furnishing Facility scheme, the inward supplies up to INR 1 Cr will be reflected in GSTR-2A before filing of GSTR-1 by the vendor. Thus, there will not be any unnecessary blockage of Input Tax Credit and it will also not put too much stress on the working capital of the large corporates.

Popular Articles :

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}