Page Contents

Section 195 of the Income-tax Act (‘the Act’) empowers the Central Board of Direct Taxes to capture information in respect of payments made to non-residents, whether chargeable to tax or not. Rule 37BB of the Income-tax Rules have been amended to strike a balance between reducing the burden of compliance and collection of information under section 195 of the Act.

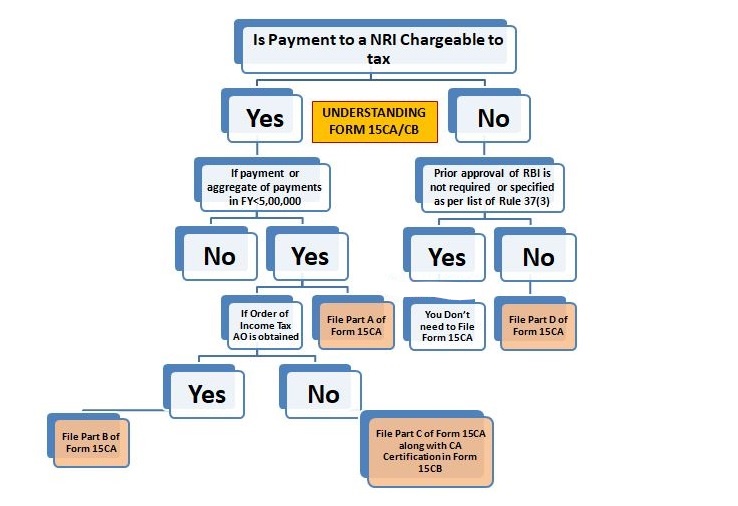

The furnishing of information for payment to a non-resident, not being a company, or to a foreign company in Form 15CA has been classified into 4 parts- Part A, Part B, Part C and Part D, wherein:

Where the remittance is chargeable to tax under the provisions of the Income-tax Act,1961 and the remittance or the aggregate of such remittances does not exceed five lakh rupees during the financial year.

Where the remittance is chargeable to tax under the provisions of the Income-tax Act,1961 and the remittance or the aggregate of such remittances does not exceed five lakh rupees during the financial year and an order/ certificate u/s 195(2)/ 195(3)/ 197 of Income-tax Act has been obtained from the Assessing Officer.

Where remittance is chargeable to tax under the provisions of Income-tax Act, 1961 and the remittance or the aggregate of such remittances exceeds five lakh rupees during the financial year and a certificate in Form No. 15CB from an accountant as defined in the Explanation below sub-section (2) of section 288 has been obtained.

Where the remittance is not chargeable to tax under the provisions of the Income-tax Act,1961 {other than payments referred to in rule 37BB(3)} by the person refer 3red to in ru7BB(2).

Any person who fails for delaying or failing to submit Forms 15CA & 15CB to the Income-tax dept is entitled to impose a penalty of INR 1,00,000/- on the defaulter. The penalty is also payable in the event that the person files incorrect information or files the wrong section of Form 15CA. The person shall be deemed to have defaulted until he/she has been unable to make a reasonable reason for failure to submit the form.

The steps to take before sending money to a non-resident are listed below:

Form 15CA must be provided by anyone making a payment to a Non-Resident. Any of the relevant elements of Form 15CA must be filled out, depending on the amount of payment and the authority to levy tax.

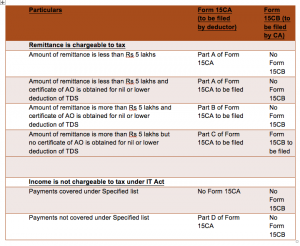

| Parts of Form 15CA | Description |

| Part A | To be filled up if the remittance is chargeable to tax under the provisions of the Income-tax Act,1961 and the remittance or the aggregate of such remittances, as the case may be, does not exceed five lakh rupees during the financial year) |

| Part B | To be filled up if the remittance is chargeable to tax under the provisions of the Income-tax Act, 1961 and the remittance or the aggregate of such remittances, as the case may be, does not exceed five lakh rupees during the financial year and an order! certificate u!s 195(2)! 195(3)! 197 of Income-tax Act has been obtained from the Assessing Officer. |

| Part C | To be filled up if the remittance is chargeable to tax under the provisions of Income-tax Act, 1961 and the remittance or the aggregate of such remittances, as the case may be, exceeds five lakh rupees during the financial year and a certificate in Form No. 15CB from an accountant as defined in the Explanation below sub-section (2) of section 288 has been obtained |

| Part D | To be filled up if the remittance is not chargeable to tax under the provisions of the Income-tax Act,1961 other than payments referred to in rule 37BB(3) by the person referred to in rule 37BB(2) |

Note: Before filling out Part C of Form 15CA, you must first upload Form 15CB. The Acknowledgment number of e-Filed Form 15CB should be provided to prefill the details in Part C of Form 15CA.

| Sr. No | Form Number | Description |

| 1. | FORM- 15 CA | Information to be furnished for payments to a non-resident not being a company, or to a foreign company |

| 2. | FORM- 15 CB | Certificate of an accountant |

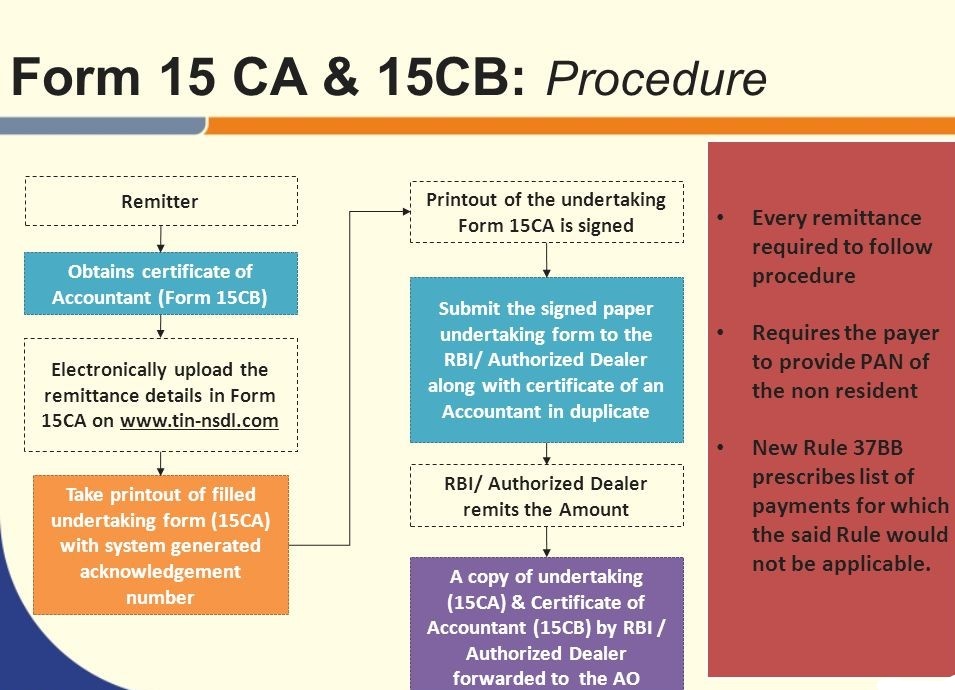

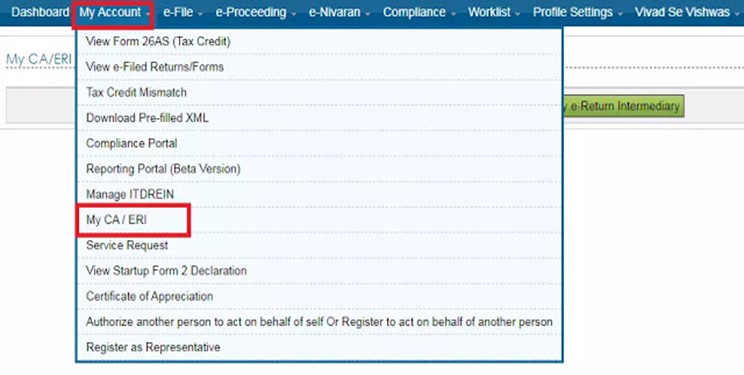

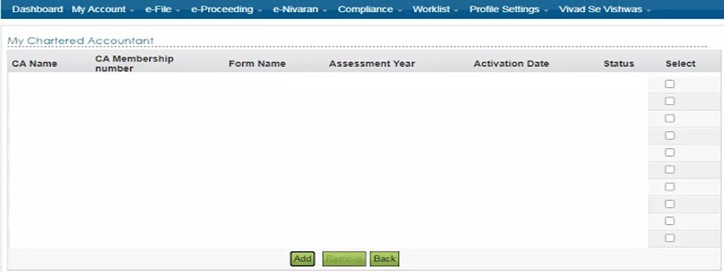

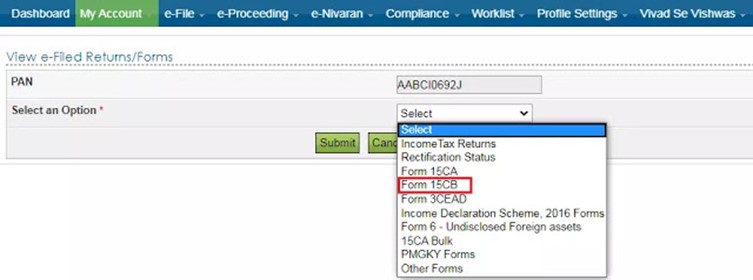

Step 1: Go to the e-filing portal and log in. Go to ‘My Account,’ then to ‘My CA/ERI,’ and finally to ‘My Chartered Accountant.’

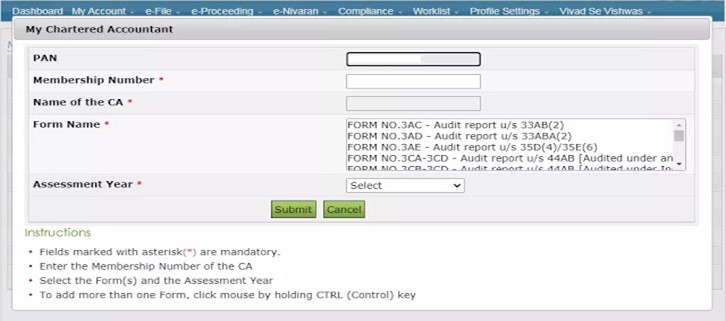

Step 2: Select ‘Add’ from the drop-down menu. Enter the Chartered Accountant’s “Membership Number.” The CA’s name will be filled in automatically. To do so, the CA must first create an account on the e-filing portal.

The website will also display the assessee’s previously added CA.

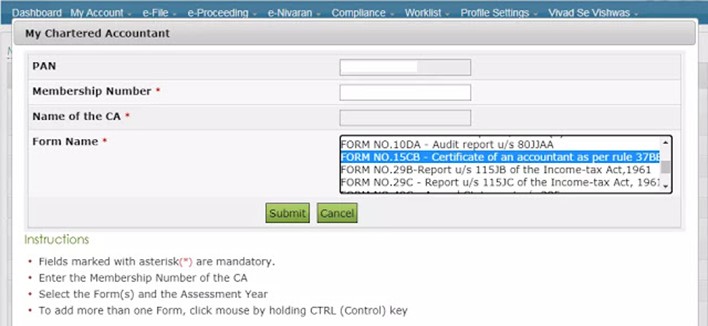

Step 3: Click Submit after selecting ‘Form No. 15CB – Certificate of an accountant as per Rule 37BB’ as the Form Name. When Form 15CB is selected, the page’s field “Assessment Year” is obscured.

Once the assessee has added CA, the CA can file Form 15CB on the assessee’s behalf.

To file the Form 15CB by the CA, go to the e-filing portal’s downloading area and download the program. Fill out the Form in the utility and the XML file will be generated. The CA then uploads this XML file on behalf of the assessee to the e-filing portal.

Note: The CA’s digital signature is required to upload the XML file of Form 15CB.

After filing the Form 15CB, or if the Form 15CB is not necessary, the Form 15CA must be filed. The assessee must file Form 15CA through his e-filing account.

The steps to e-File Form 15CA (e-filing portal) issued by the Income Tax Department are listed below.

Due to technical issue of the Released recently income Tax Portal, Manual Submission of 15CA/CB to AD are allowed, AD is encouraged to accept the manual form. Later on a service will be supplied to upload such manual form for records.

Popular blog:-

For query or help, contact: singh@carajput.com or call at 9555555480

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

Understanding Form 16, Form 16A & Form 26AS: A Complete Guide for Taxpayers When filing your Income Tax Return (ITR),… Read More

CFO Cum whole-time director? ROC Gwalior Says No in EKI Energy Services Case Corporate governance is built on the principle… Read More

Toughest Exams in India: More Than a Test of Knowledge, A Test of Character Every year, millions of students and… Read More

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}