Mandatory Private Ltd Co. Common Compliance’s Ensure

Page Contents

www.carajput.com; PRivate Limited Company

Mandatory Private Ltd Co. Common Compliance’s Ensure

A private limited company is held for small-run businesses.

It has a perpetual succession the liability of the members is limited by the number of shares held by the members. Name of the private company end with the words private limited.

REQUIREMENTS OF PRIVATE LIMITED COMPANY REGISTRATION

Minimum 2 and maximum 200 members are required for making a private limited company.

In This case Minimum 2 directors are required for making a private limited company.

The company must make one registered office address.

Company shall register his permanent address to the registrar until the permanent address is not established company shall provide the temporary address.

It shall send 1 or 2 names for approval to the registrar. All names shall be unique and not resemble any other company.

Every company shall obtain a digital signature certificate (DSC) which is used to verify the documents.

copy of PAN card of shareholders/ directors with Passport copy in case NRI subscribers.

This needs various professional company secretaries, chartered accountants, cost accountant

COMPLETE FILING OF YOUR COMPANY ROC ANNUAL COMPLIANCE- COMMON COMPLIANCE’S WHICH A PRIVATE LIMITED COMPANY HAS TO MANDATORILY ENSURE- TIME IS RUNNING OUT-: –

While you are busy planning the business strategies, there are various compliance’s which are required to be followed once your business is incorporated.

Managing the day-to-day operations of your business along with complying with the corporate laws can be a little taxing for any entrepreneur.

Hence, it is essential to take the help of a professional and also understand such legal requirements to ensure timely fulfillment of compliance’s, without any levy of interest or penalty.

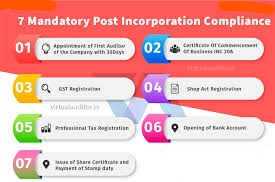

The first auditor of the company should be appointed within 30 days of the incorporation. Filing of ADT – 1 is mandatory.

Appointment of Auditor- Auditor will be appointed for the 5 (Five) years and form ADT-1 will be filed for a 5-year appointment. Appointment of Auditor- within one month.

Board of Directors shall appoint an auditor at the first annual general meeting till the conclusion of the 6th annual general meeting.

Holding Annual General Meeting- It is mandatory for every Private Limited Company Company to hold an AGM in every Calendar Year. Companies are required to hold their AGM within a period of six months, from the date of closing of the Financial Year.

Every private company under section 184(1) is required to obtain MBP – 1 from the director. Every director of the company at the first meeting of the board shall disclose his interest in another entity.

As per section 164(2), it is required to give yearly DIR – 2 a disclosure of nondisqualification to the companies.

Private limited company-

Paid-up share capital 10 cr. Or more

Turnover of 550 cr. Or more

Shall require to file MGT – 8 from the company secretary

If any private limited company has any outstanding loans, deposits at the end of the financial year are required to file DPT – 3 before 30th June of the next financial year from the year of outstanding loans or deposits.

MSME – 1 every private company is required to file every half year within 30 days of the end of half-year.

director of the company who is having DIN no. is required to file e – form DIR – 3 KYC till 30 September every year.

Return of director or KMP is filed with ROC in FORM DIR – 12 within 30 days of appointment.

Every private company is required to file a director’s report, Preparation of Directors’ Report- Directors’ Report will be prepared with a mention of all the information required under Section 134.

Every private limited required to meet at least one general meeting of the shareholders

Maintain a register of members

Maintain a register of director

Maintain Register of key managerial

Register of share transfer

Maintain Register of related party

Lastly Register of investment.

Statutory Audit of Accounts- Every Company shall prepare its Accounts and get the same audited by a Chartered Accountant at the end of the Financial Year compulsorily.

The Auditor shall provide an Audit Report and the Audited Financial Statements for the purpose of filing it with the Registrar.

AOC – 4 filing of a financial statement within 30 days of the annual general meeting to the registrar of companies.

The director’s report is filed along with the form AOC – 4 within 30 days of the annual general meeting. Filing of Annual Return (Form MGT-7)- within 60 days

Filing of Financial Statements (Form AOC-4)- within 30 days.

Under section 92 every private company is required to file MGT – 7 to the registrar of companies within 60 days of the annual general meeting.

Besides this. Do you know?

Being a Pvt Ltd Company / LLP you are liable for paying Profession Tax of Company, Directors & Employees from the 1stday of company inception.

You are liable for deducting TDS in various rates applicable for various slabs from 1st

Non-Compliance;

If a Company fails to comply with the rules and regulations of the Companies Act, then the Company and every officer who is in default shall be punishable with a fine for the period for which default continues.

There is a delay in any filing, then additional government fees is required to be paid, which keeps on increasing as the time period of non-compliance increases.

Please take note of this very important proposed amendment in the companies act.This is passed by Lok Sabha and presented to Rajysabha.

Once it is passed, for the annual return and balance sheet late fees will be Rs. 100 per day. And if there is a repeat default (means for more than one year) for a second-year late fee will be Rs. 200 per day.

If any company has not filed returns for 2015-16 or for earlier years; the late fee perform will be a minimum of 36500 per year. We need to file all old returns before this amendment gets passed.

FAQ ON ANNUAL COMPLIANCES

Q1- in how many days AOC – 4 shall be filed by the private limited company?

Ans.- within 30 days of holding of annual general meeting AOC – 4 shall be filed.

Q2- within how many days of incorporation auditor should be appointed by the company?

Ans.-within 30 days of the incorporation auditor shall be appointed by the company.

Q3- in which form shall directors disclose their interest to the company?

Ans- MBP – 1 is to be filed by the director to disclose his interest to the company.

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}