Page Contents

www.carajput.com; Foreign contribution (regulation) amendment bill, 2013

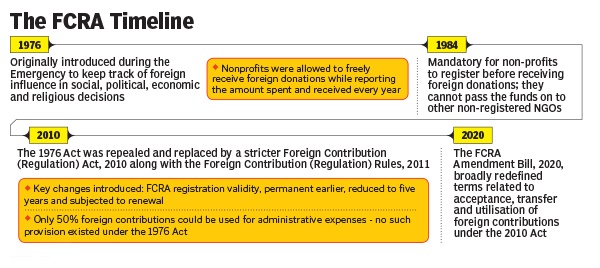

These changes to the FC4 form are greatly appreciated. It will bring deviant organizations more public attention and, perhaps, examination, because commoners will be able to link them to a publicly visible asset (such as an orphanage or a school on one’s street or neighborhood).

Popular article :

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}