Key features on Auto-population of e-invoice details in GSTR-1/2A/2B/4A/6A

Who’s needed to create an E-invoice?

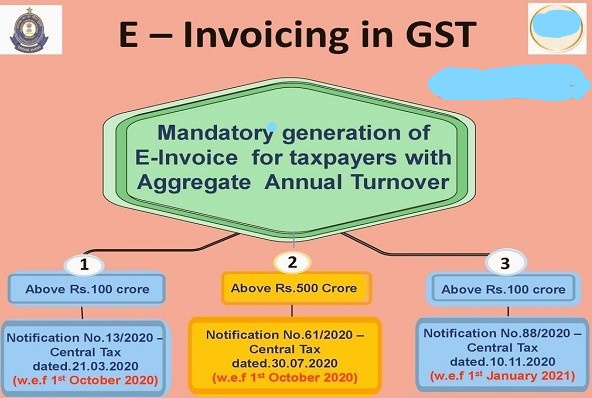

Wide Notification No. 13/2020–Central Tax dated 21 March 2020, amended from time to time, any registered person with a cumulative turnover exceeding Rs 500 Cr in any previous FY from 2017 to 18 is needed to create an e-invoice w.e.f. 1 October 2020.

In addition, every registered person with a total turnover in excess of Rs 100 Cr during any previous FY from 2017-18 onwards is required to generate an e-invoice w.e.f. 1 Jan 2021.

E-invoice for Registered Person

Starting Timeline

The registered person having a total turnover in excess of Rs 500 Cr.

1st Oct 2020

The registered person having Total turnover in excess of Rs 100 Cr

1st Jan 2021

GST E-Invoices – Advantage

It is a reduction in price.

GST E-Invoices Simplified GST compliance

E-Invoices Improvement in business efficiency

Precision

E-Invoices abolition of paper

Lesser reconciliation errors

The effective functioning of capital performance

It is therefore not a soft copy of the GST invoices.

The e-invoice is not just about the invoice shown in the soft copy as PDF, etc.

E-invoice does not assume that the invoice is created through the govt portal.

E-invoicing shall not apply to specific categories of registered persons, whether or not their turnover exceeds the threshold as notified in CBIC Notification No. 13/2020-Central Tax:

The registered person providing services by way of admission to the exhibition of cinematographic films in multiplex services.

An insurer, a banking company, or a financial institution, including the NBFC.

A registered person providing passenger transport services.

Goods and Transport Agency (GTA).

SEZ unit (excluded by CBIC Notification No. 61/2020 – Central Tax).

Auto-population of e-invoice details in GSTR-1/2A/2B/4A/6A

Invoices for which e-invoices have been created have also begun to auto-populate particulars of such e-invoice in the below processes:

Return Form GSTR-2A (Auto-populated Inward Supply Details) of the recipient.

Form GSTR-2B Return (Auto-drafted recipient’s ITC statement).

Return Form GSTR-4A (Auto-populated Inward Delivery Details by Composition Dealer) of the recipient.

Form GSRT-6A Return (Auto-populated details of inward supply by Input Service Distributor).

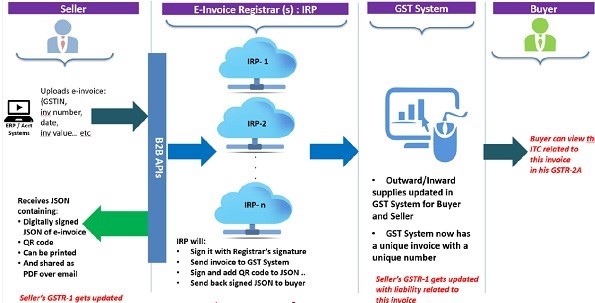

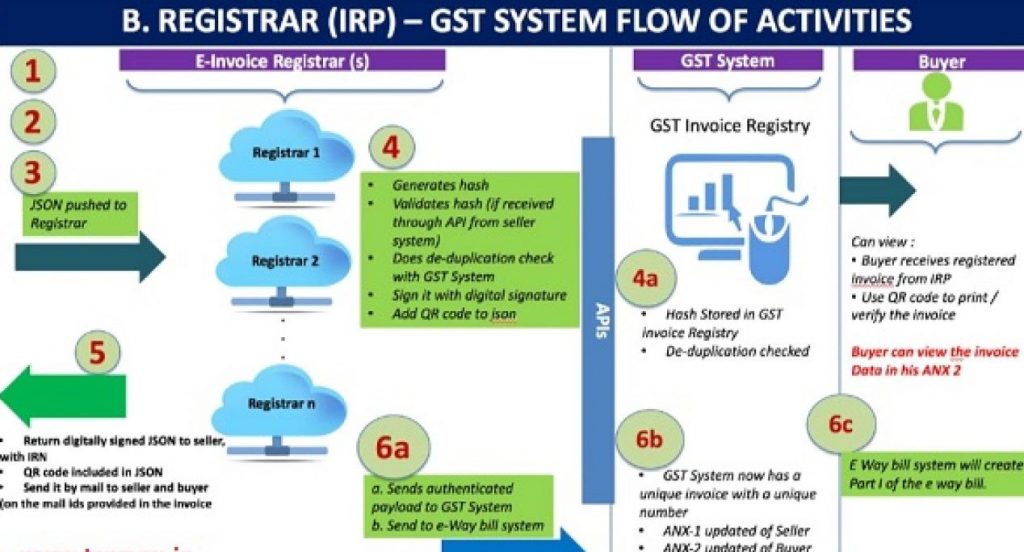

Few notified taxpayers issued invoices after acquiring the Invoice Reference Number (IRN) from the Invoice Registration Portal (IRP) (typically called ‘e-invoices’). The specifics of these e-invoices shall be auto-populated in the respective GSTR-1 tables. Here are all the key requirements that must be taken into consideration.

The time lag between E-invoices uploaded to the portal and updated to GSTR-1

The data in GSTR-1 is now available on T+3 days, i.e. e-billing data uploaded on 18-12-2020 would’ve been visible in GSTR-1 on 21-12-2020.

Consequent reflection of these e-invoice details in GSTR-2A/2B/4A/6A has also started.

Auto-population of E-invoice records to GSTR-1 based on Document Date

Auto-population of e-invoice data in GSTR-1 is provided at the time of the document (as reported to IRP). For instance, a document dated December 30, 2020, is reported to IRP on January 3, 2021, with two situations possible;

Situation 1:

If GSTR-1 is not filed for Dec 2020, the particulars of that document will be obtainable in the GSTR-1 tables for Dec 2020.

Situation 2:

If the GSTR-1 has already been filed for Dec , the details of that document will be made accessible in the consolidated excel file that can be downloaded from the GSTR-1 dashboard (with an error description as ‘Return already filed).

An instance where Invoice details will not be auto-populated in the GSTR-1 Return

Due to the existing validations in GSTR-1, the e-invoices reported as below frequently reported issues are not auto-populated in the GSTR-1 tables but are made publicly available in the consolidated excel file that can be downloaded from the GSTR-1 dashboard (with based on the error description):

The document date is after the date of cancellation of the registration by the supplier/recipient;

Invoices reported as attracting “IGST on intrastate supply” but without reverse charge

The supplier is found to be of type ISD/NRTP/TCS/TDS;

Supplier is found to be a composition taxpayer for that tax period;

The document date is before the date of registration of the Supplier/Recipient;

Commonly used data structure issues during E-invoice

Moreover, due to data structure issues, e-invoice details could not be processed (and were therefore not auto-populated) in some cases. These errors may be noted and avoided while reporting the data to the IRP.

The serial number of the item shall not be reported as ‘0’

White space found in POS (Place of Supply State Code), e.g. ‘8’ The expected values were 08 and 8.

Comprehensive advice on self-population methodology etc. has already been made available on the GSTR-1 dashboard (‘e-invoice advisory’) and has also been e-mailed to the appropriate taxpayers.

Auto-population of information in GSTR-1 is just a facility responsibility of the Supplier

It is reiterated once again that the auto-population of details from e-invoices to GSTR-1 is only an opportunity for taxpayers. After viewing the auto-populated data,

Taxpayer needs to verify the propriety and accuracy of the amounts and all other data in each field in particular from the viewpoint of GSTR-1, and file the very same information in the light of the relevant legal provisions.

The Taxpayer has recommended authenticating the auto-populated documents in the GSTR-1 tables & excel on the below areas:

All documents reported to the IRP are in excel.

The position of each e-voucher/IRN is correct

All the details of the document are correctly stored

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}

{kind=link}

{kind=link}