Page Contents

The Goods and Services Tax Act was passed in the year 2017, with the aim to subsume, almost all the indirect taxes, into a single tax. Thus, a uniform tax rate be applicable on all goods and services. Every person, registered under GST and supplying goods or services, is required to comply with the rules and regulations specified in the GST Act. Where, any non-compliance is witnessed, the same be held as the breach of law, and shall be liable to penalties. The GST Council expects to have more than 1 crore GST registration since there will be smoothen structure for registration, filing and conducting the business.

GST provides a list of certain activities that are termed as an offence. Since the primary aim of GST is to eliminate Tax Evasion, strict penalties were fixed for the offences listed in the GST.

Under Sec 122(1), the following 21 defaults have been specified, involving a penalty of Rs 10,000 or the amount of tax involved, whichever is higher.

It is believed that for proper regulation and monitoring of any law, there is a requirement to have provisions relates to inspection, search, seizure and arrests to protect the interest of genuine taxpayers. These provisions will thereby help the Officers to undertake requisite actions and hence protect the Government Revenue.

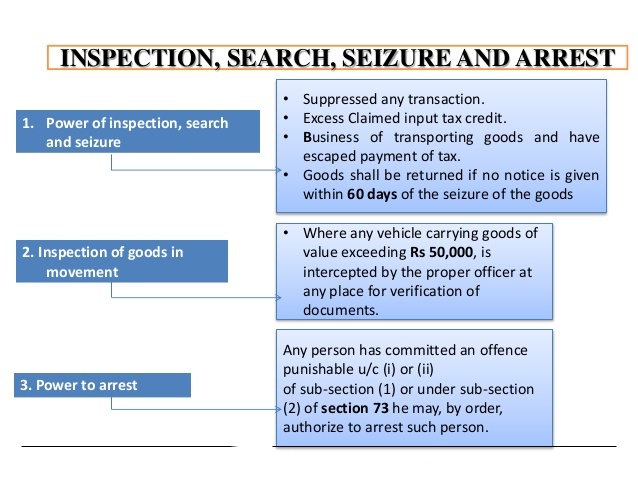

Under the GST Act, the inspection can be initiated where, the Joint Commissioner of SGST/CGST, have the reasons to believe that to evade tax, a person has suppressed any transaction or claimed excess input tax credit. In such a case, the Joint Commissioner can authorize any other officer, to inspect places of business of the suspected evader. The reason to believe shall relate to –

Under this, the person carrying the goods of value exceeding Rs. 50,000 is required to carry the following documents:

The proper officer can intercept goods in transit and have an inspection of the goods and the documents. Where the goods are found to be in contravention of the GST Act, such goods, related documents, and the vehicle will be seized. And the goods be released only on payment of tax and penalty.

It can be seen that more strict procedure of Search and Seizure has been prescribed as compared to inspection, and as a result, the Joint Commissioner or any officer with similar rank is authorized to order for search. Also, the officer shall order for search and seizure only after having valid information and reason to believe that the taxpayer is in receipt of goods liable to confiscation or any documents, books, record or things relevant to any proceedings.

All these search and seizure be carried out in accordance with the provisions of Criminal Procedure Code, 1973 which requires the presence of at least two independent witnesses and a record of entire proceedings. During the time of search and seizure, any goods, documents, books, records or other things which is related to the proceeding shall be searched or seized. Where the seize of a goods or object is practically not possible, such goods or object can be detained. Also, an inventory of the seized goods and documents must be prepared by the Officer and the same be provided to the person from whom the goods or documents were seized.

All documents or objects detained must be returned, provided the same is required for examination / enquiry / proceedings. Where an exporter claims higher duty drawback during the transitional period, the said individual shall attach the declaration from the exporter and certificate from jurisdictional GST officer, so that the double availing of input taxes can be eliminated. However, in case the notice is not issued within a period of six months, then such goods need to be returned to the owner of the goods or documents.

GST: Unauthorized search and seizure by BIEO, HC grants interim relief. Case M/s. Kumar Traders And Company & Anr. Vs. The State of Assam (Guwahati High Court)

GST rules and regulations also provides for the harshest of the punishment involving imprisonment. Imprisonment is ordered under GST if a person commits the prescribed offences and the tax amount is exceeding Rs.100 lakhs. The following term of imprisonment has been provided –

| DEFAULT OF TAX | IMPRISONMENT |

| RS 100 – 200 LAKHS | UPTO 1 YEAR |

| RS 200 – 500 LAKHS | UPTO 3 YEARS |

| ABOVE RS 500 LAKHS | UPTO 5 YEAR |

| AIDS IN COMMITMENT OF AN OFFENCE | UP TO 6 MONTHS |

Where any summon has been issued by the proper officer, the person to whom such summon is issued is required to present himself before the officer, providing the required evidence or to produce a document as and when required.

The proper officer shall appoint an officer for conducting a search in the business premises of the registered taxable person for inspection of the book of accounts, documents and other related papers. However, the search should be made only in respect of audit or verification of accounts of a registered person.

The person shall be asked to provide the following documents to the officer –

Popular blog:

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

{kind=link}

{kind=link}