Page Contents

The documentation required for e-Invoicing and reporting to the Invoice Registration Portal (IRP):

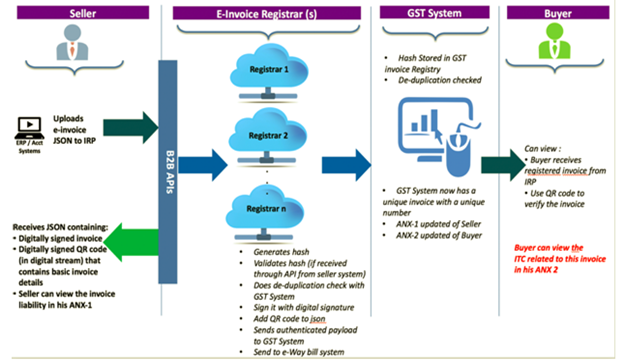

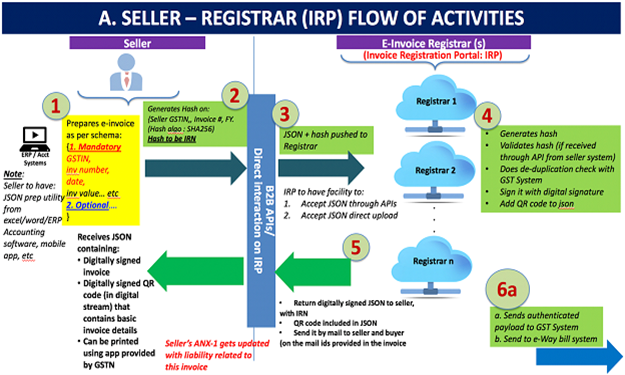

Step 1:

Step 2:

Step 3:

Step 4:

Step 5:

In the backend, the uploaded data is shared with the server maintained by the GSTN.

Step 6:

along with the QE Code, a digitally signed JSON with IRN is given back to the seller. Also, the registered invoice is sent to both the buyer and the seller by e-mail.

Step 1:

Stage 2:

Step 3:

Popular blog:-

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}