HSN & SAC CODES ALONGWITH GST RATE

- HSN codes: Basically HSN stands for a harmonized system of nomenclature. This harmonized system of the nomenclature coding system is developed by the World Customs Organization.

- Now This is a global standard of the Nomenclature of normal trading goods in foreign trade.

- The harmonized system of nomenclature is the codification of all tradable commodities into twenty broad sections with each and every chapter containing commodities of the same kind of nature.

- Its normal vision of classifying goods from all worldwide in a systematic & logical way. It is a 6th digit uniform code that classifies more than 5k products & is accepted globally.

- This HSN code is a set of defined regulations used for GST taxation objective in identifying the GST Rate of tax apply to a product in a Nation.

HSN codes of goods along with the rate of IGST, CGST, SGST mention in the below link

Link

What is a harmonized system of nomenclature (HSN) classification?

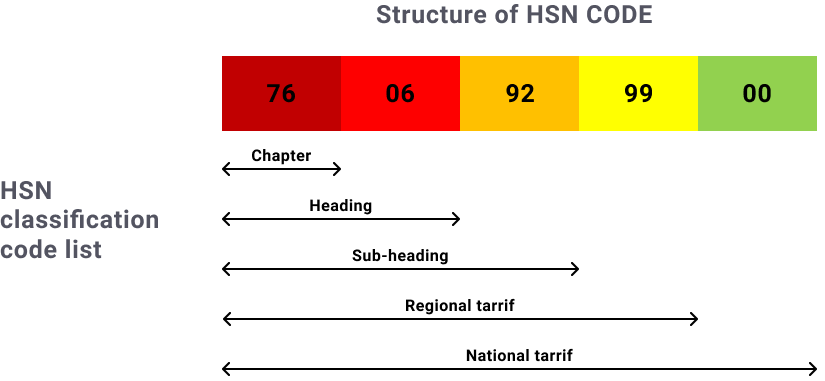

HSN(harmonized system of nomenclature) have twenty-one sections, ninety-nine chapters, 1,244 headings, & 5,224 subheadings. Sections & chapters are arranged in order of a product’s degree of manufacture/ in terms of its technological complexity.

Natural products like animals & vegetables appear in earlier sections; man-made/technologically advanced products like machinery appear later.

Chapters have a similar structure. Take cotton, for example – Chapter 52. Cotton that has not been carded or combed appears earlier in the chapter; cotton as a woven fabric appears later.

- Each Section is a collection of various chapters. Sections represent a broader class of goods, and chapters represent a particular class of goods.

- Each chapter is further divided into various headings depending upon different types of goods belonging to the same class.

- Each heading contains products, which are ultimately assigned an HSN code.

- For better identification of goods, India and a few other countries use eight-digit codes for deeper classification.

- few HSN codes also use dashes. A single dash (-) at the beginning of a description denotes an article that belongs to a group covered under a heading.

- A double dash (–) indicates that the article is a sub-classification of the preceding article that has a single dash. Similarly, a triple dash (—) or a quadruple dash (—-) indicates the article is a sub-classification of the preceding article that has a double dash or triple dash.

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}