Page Contents

Waiver of late fee & interest for composition taxpayers and normal taxpayers (filing return on monthly or quarterly basis) (Part1)

Normal (Monthly / Quarterly) and composition taxpayers have been exempted from paying interest and/or late fees for the tax periods of March, April, and May, 2021, by Government has granted via Notification Nos. 18/2021 and 19/2021, both dated 1st June, 2021. The details are concluded as follows:

Relaxation to normal taxpayers in filing of monthly return in Form GSTR-3B

| Sl.No. | Tax Period | Class of taxpayer (Based on AATO) | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 45 days | From 61st day onwards | |||||

| 1 | March, 2021 | > Rs. 5 Cr. | 20th April | 9% | 18% | 18% | 5th May, 2021 |

| Up to Rs. 5 Cr | 20th April | Nil | 9% | 18% | 19th June, 2021 | ||

| Sl.No. | Tax Period | Class of taxpayer (Based on AATO) | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 30 days | From 46th day onwards | |||||

| 1 | April, 2021 | > Rs. 5 Cr. | 20th May | 9% | 18% | 18% | 4th June, 2021 |

| Up to Rs. 5 Cr | 20th May | Nil | 9% | 18% | 4th July, 2021 | ||

| Sl.No. | Tax Period | Class of taxpayer (Based on AATO) | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 15 days | From 31st day onwards | |||||

| 1 | May, 2021 | > Rs. 5 Cr. | 20th June | 9% | 18% | 18% | 5th July, 2021 |

| Up to Rs. 5 Cr | 20th June | Nil | 9% | 18% | 20th July, 2021 | ||

Waiver of late fee & interest for composition taxpayers and normal taxpayers (filing return on monthly or quarterly basis) (Part2)

the government waived interest and/or late fees for normal (monthly / quarterly) and composition taxpayers for the tax periods of March, April, and May, 2021. via Notification Nos. 18/2021 and 19/2021, both dtd. 1st June, 2021,

| Sl.No. | Tax Period | Form Type | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 45 days | From 61st day onwards | |||||

| 1 | March, 2021 | Form GSTR-3B (Quarterly) | 22/24th April, 2021,(Group A/B) | Nil | 9% | 18% | 21/ 23rd June, 2021,(Group A/B) |

| Sl.No. | Tax Period | Form Type | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 30 days | From 46th day onwards | |||||

| 1 | April, 2021 | Form GST PMT-06 | 25th May, 2021 | Nil | 9% | 18% | NA |

| Sl.No. | Tax Period | Form Type | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 15 days | From 31st day onwards | |||||

| 1 | May, 2021 | Form GST PMT-06 | 25th June, 2021 | Nil | 9% | 18% | NA |

| Sl.No. | Tax Period | Due date of filing | Reduced Rate of Interest | Waiver of late fee till | ||

| First 15 days from due date | Next 45 days | From 61st day onwards | ||||

| 1 | March, 2021 (Qtr.) | 18th April, 2021 | Nil | 9% | 18% | NA |

GST latest Notifications: Analysis of CBIC Notifications on GST extensions dated 24 June 2020

Today, CBIC issued various notifications to implement the recommendations of the 40th GST Council meeting as follows: CBIC Notifications signed on 24.06.2020 regarding interest waiver and late fees. On 24 June 2020, the CBIC released multiple notifications of GST. The synopsis of those updates is here.

Notice No. 49/2020 – Central Tax: Implementing some aspects of the Finance Act, 2020

Notification No. 50/2020 – Central Tax: Notification of GST rates for individuals taxable in composition under Rule 7 of the CGST Rules

GSTR-3B-Interest rate waiver: Notification No.51/2020-Central Tax 24.06.2020: To put certain provisions of the Finance Act into force, 2020.

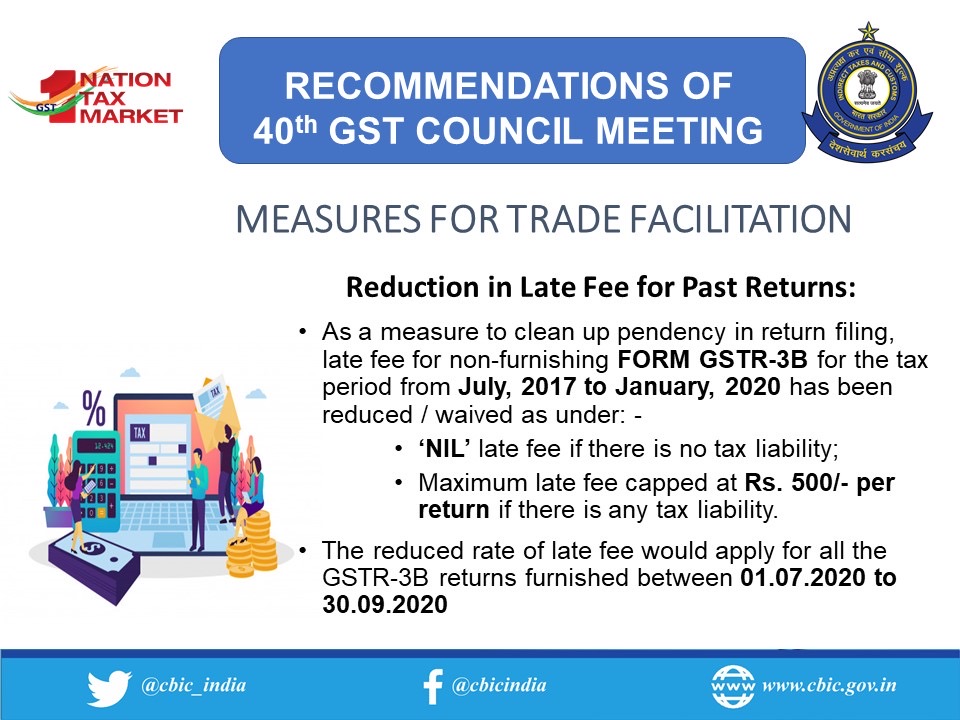

Notification No. 52/2020 – Central Tax: GST waiver for taxpayers who’ve not filed GSTR-3B for tax dates between July 2017 and January 2020 shall be informed as stated earlier at the 40th meeting of the GST Council. In CGST Notification No. 52/2020 dated 24 June 2020, the CBIC notified that between 1 July 2020 and 30 September 2020, Zero GSTR-3B could be filed without a late fee for the above duration. Furthermore, it shall be limited to a maximum of Rs 250 per return per month per act for the remaining taxpayers.

A late fee exemption also moved the last GSTR-1 deadlines from March to June 2020 as of June 30th, 2020. The latest timelines for monthly filing without even a late fee charge will be from March to June 2020, 10th, 24th, 28th July 2020, and 5th August 2020 respectively. The last date for the GSTR-1 quarterly is 17th July and 3rd August 2020 for the quarters January-March 2020 and April-June 2020.

More updates :ITC on sale of DEMO cars Supply under GST

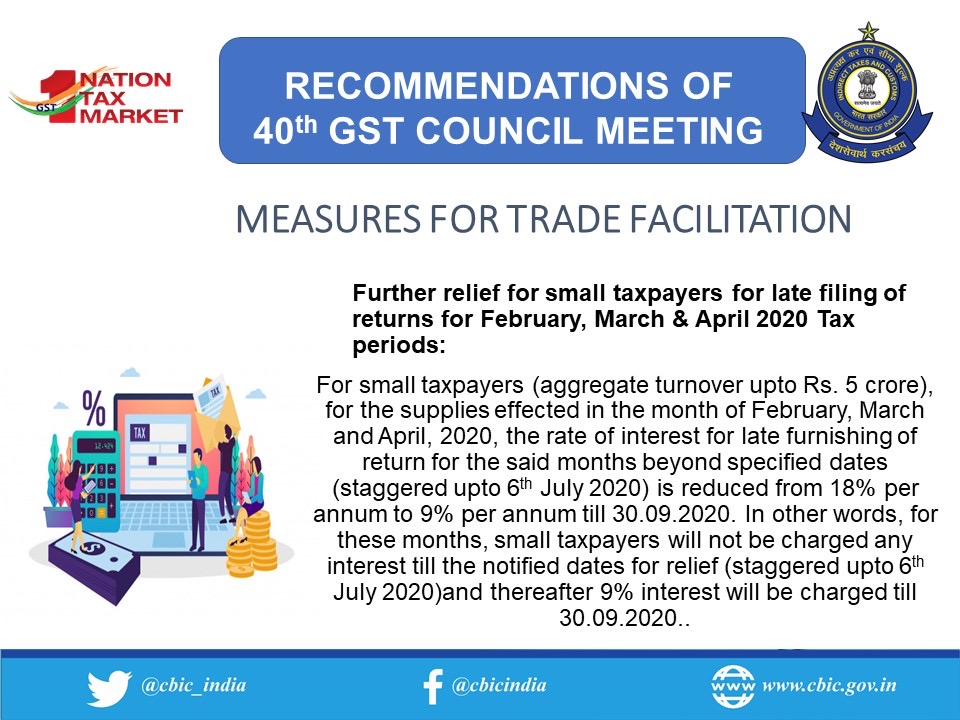

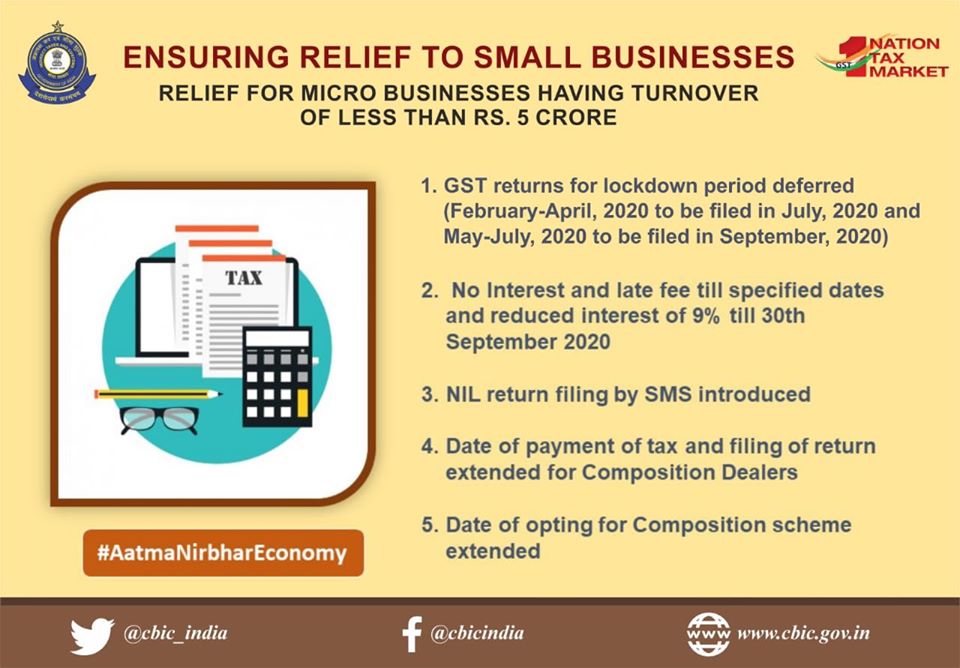

Big taxpayers have not been informed of further extensions for filing GSTR-3B from February to May 2020, with an annual turnover of more than Rs 5 Crore in the previous financial year. Furthermore, no interest should have been paid from the respective due dates of February to April 2020, i.e. 20th of the following month, for the first 15 days respectively. After that, interest at a 9 percent p.a. reduced rate. Any further delay in GST payments would have been imposed till 24 June 2020.

Initially, taxpayers with an aggregate annual turnover of up to Rs 5 crore in the last financial year have their due date staggered as 22nd # or 24th # of their next month, depending on the state / UT from which they run their main place of business. For the exception of May 2020, its due date staggered as July 12th # or 14th # # 2020. Furthermore, in the exception, August 2020 also comes with yesterday’s due date extended to 1st # or 3rd # # October 2020.

The CBIC has abolished the taxpayer bifurcation based on the annual sales up to Rs 1.5 crore or between Rs 1.5 crore and Rs 5 crore. Correctly, as per yesterday’s 40th meeting of the GST Council, the late fee and the interest waiver will continue until September 2020

GSTR-1-Late Fees / Penalty Waiver: Notification No.53/2020-Central Tax 24.06.2020: Conditional waiver of late fees for all GSTR 1 registered persons for months/quarters ending March to June 2020, if submitted by the time set.

GSTR-3B-Extension of the deadline for Aug 2020: Notification No.54/2020-Central Tax 24.06.2020: extension of the deadline for submission of GSTR 3B to 1/3 October 2020

Popular blog:-

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}