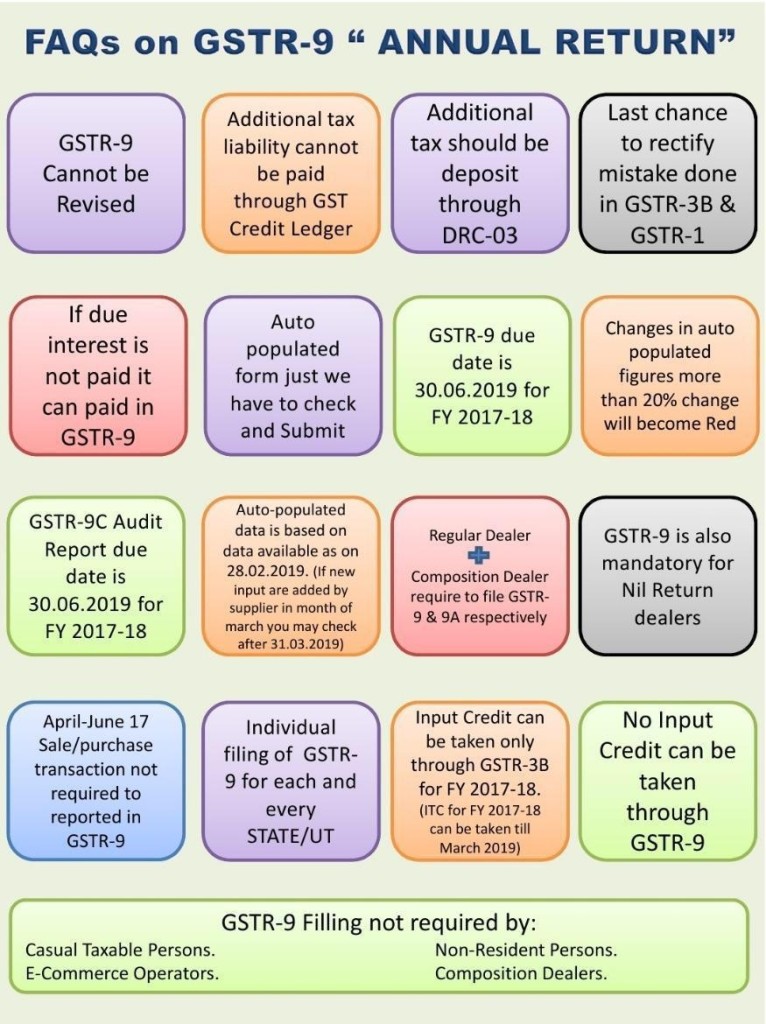

Annual GST report 9 will be filed by taxpayers registered with GST and NIL return Filling

GSTR 9 is an annual report that GST-registered taxpayers are required to file, even those who have opted for the composition levy scheme. Consolidating the information given in the monthly and quarterly reports, GSTR 9 provides descriptions of the deliveries rendered and obtained under SGST, CGST, and IGST during the last financial year.

Under the said scheme, there are four forms of returns to be filed – GSTR 9, GSTR 9A, GSTR 9B, and GSTR 9C that can be lodged on the GST portal.

- GST Annual Return (GSTR-9) part A and Part B as per Section 44 of CGST

- GSTR 9 is the form provided for in section 44 of the CGST Act.

- This GSTR 9 comprises two parts, i.e. I Part A, Basic Data, and (ii) Part B, Annual Return, respectively.

- Part-I attempts to capture the basic information of the Registered Individual in Part A (Reconciliation Declaration) containing 4 clauses;

- Each of the clauses in Part I is applicable to the criteria for disclosure.

- This provision requires documentation of the “financial year” to which Part A of the Declaration of Reconciliation relates.

- The term of the financial year was not specified in the GST legislation.

- However, ‘financial year’ as specified in the General Clauses Act means the year starting on the first day of April and ending on the 31st day of March;

- It is important to recognize the significance of the term ‘financial year’ in the first year of the GST regime since the first day of July 2017, when the GST legislation came into force.

- For all purposes, and for the financial year 2017-18, since the GST Laws were applicable only for nine months from July 2017 to March 2018, ‘2017-18’ may be referred to in this section. (9 months starting July 1, 2017, and ending March 31, 2018).

Annual Returns Filing under GSTR 9 NILL

It is necessary to note that if certain conditions are met, annual returns under GSTR 9 can also be filed under “NIL.” You will apply for Zero GSTR 9 returns if you have:

- No outward supply (commonly referred to as sale)

- There is No inward supply (commonly referred to as purchase) of goods/services

- No liability whatsoever

- There is no Credit was claimed during the financial year

- No order generating demand was issued • No refund was requested

You may also like the following Blogs: GSTR enable details to be auto-populated in E-invoice GSTR-1

- Annual returns on Form GSTR-9 / 9A will be optional for taxpayers with an annual turnover of less than Rs 2 crore;

- Taxpayers with a yearly aggregate turnover of more than Rs 5 crore will be required to provide a reconciliation statement in FORM GSTR-9C.

- GST Taxpayers would be able to self-certify the reconciliation statement (GSTR 9C), instead of getting it certified by Chartered Accountants / Cost accountants.

It will increase management responsibility and accountability because he will no longer be able to claim that a mistake occurred because he did not to get proper guidance. Anyway, Self Certification gives as much trouble as Self Medication.

Govt Reduces Compliance Burden For GST Taxpayers

Self Certification GST Annual Return(Form GSTR-9C) for Financial Year 2021-21

- Finance Ministry announced new relaxations for the GST taxpayers. Taking to Twitter, the Finance Ministry said that taxpayers with AATO up to INR 5 Cr are not needed to submit reconciliation statement in Form GSTR-9C for Financial Year 2020-21 onwards.

- The Finance Ministry also given relief to GST taxpayers Annual Aggregate Turnover (AATO) above INR Five Cr.

- GST Taxpayers Annual Aggregate Turnover (AATO) above INR Five Cr can now self-certify reconciliation statement in Form GSTR-9C for Financial Year 2020-21 onwards, instead of getting it certified by a cost accountant or charted accountant.

Relaxation from the filing of GSTR 9 i.e. Annual Return

- Meanwhile, taxpayers having Annual Aggregate Turnover upto INR 2 Cr only are now not required to file GST Annual Return -Form GSTR-9 for Financial Year 2021-21.

What is the due date for Gstr 9 and 9c?

- Deadline for companies to file GST Annual return filings for Financial year 2020-2021 has been extended by the Center govt.

- CBIC vide Notification No. 40/2021 stated that -Deadline for filing GSTR 9 and 9C for Financial year 2020-2021. has been extended from December 31, 2021 to February 28, 2022 for the (By Amended Rule 80 of the CGST Rules – Central Tax dated December 29, 2021.)

Notes : Important issue in filling GST Audit Filling Form 9C under the GST

Should you fill Tables 17 and 18 of GSTR-9 or skip them?

- While filing GSTR-9, every taxpayer will have the option of filling up Tables 17 and 18. The details of the HSN summary on outward and inward supplies are included in these tables.

- However, the Department has made filling these out an option for FY 2020-21.

We recommend that you set aside some duration to accomplish these tables. There are multiple reasons to do so:

- GST Dept. has been using the data from these tables for raids and inspections, filling them out will help to avoid confusion and offer the Department a clearer picture of your business.

- Because you already filed the HSN summary of the outward supply in Table 12 of the GSTR-1 form, you won’t have to go through much effort.

- GST Dept. has made it optional for this year, but that doesn’t imply the case will be the same next year; therefore, filling it out this year will help you next year.

GST: Major Impact on late filers

- Late fees for delayed filing of FORM GSTR-1 are to be auto-populated and collected in the next open return in FORM GSTR-3B.

- CBDT Notification No. 113 of 2021 in S.O. 3814(E) dated 17th September, 2021 issued. In view of the difficulties being faced by the taxpayers, the central government has extended certain timelines.

- CBIC : Rule 80 of CGST Rule has been Changed to provide that annual return (GSTR 9/9C) for Finance Year 2020-21 can be filed till 28.02.2022.

- CBIC has extended the last date for filing of Annual GST Return (GSTR 9/ 9A/ 9C) in respect of FY 2020-21, from 31 Dec 2021 to 28 Feb 2022, through Central Tax Notification 40/2021 dated 29 Dec 2021

Advisory on Revision of Timeline for Amendment of Aggregate Annual Turnover (AATO), 2026

GSTN has revised the timeline for amendment of Aggregate Annual Turnover (AATO) for FY 2025-26 due to system enhancements that will enable automatic updating of AATO as subsequent returns are filed. Key Changes

| Activity | Revised Timeline |

| AATO Amendment Application Window (FY 2025-26) | 01 July 2026 to 31 July 2026 |

| Review by Jurisdictional Tax Officer | 01 August 2026 to 15 August 2026 |

What Has Changed?

- Earlier, as per the GSTN advisory dated 02 May 2022, taxpayers could amend their AATO during the month of May. For FY 2025-26, the amendment window has been shifted to 01–31 July 2026.

- The amended AATO details will be available to the jurisdictional tax officer for review from 01–15 August 2026.

Reason for the Revision of Timeline for Amendment of Aggregate Annual Turnover (AATO)

GSTN is implementing system-level enhancements to Improve consistency and accuracy of AATO data, taxpayer must ensure uniform reporting across GST portal modules. taxpayer must facilitate automatic updates of AATO based on subsequent return filings.

Advisory for Taxpayers

Taxpayers should carefully verify the AATO details before submitting amendment requests. Taxpayers must ensure that amended figures are accurate and supported by records. and taxpayers submit amendment applications within the revised window (1 July–31 July 2026).

In Case of Issues

Any difficulty or discrepancy may be reported through the GST Self-Service Portal (Grievance Redressal Mechanism) with complete details for prompt resolution.

AATO is critical for determining GST return filing eligibility and frequency, e-invoicing applicability, and Various compliance thresholds under GST. Hence, taxpayers whose turnover figures require correction should ensure the amendment is completed within the revised July 2026 window.

Popular Article:

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}