Page Contents

The Govt. of India requires to make the National pension Scheme fair to all classes of subscribers.

The Budget 2021 will be introduced on the 1st of Feb 2021, so I think to make few tips to eliminate some of the inequalities & anomalies in the provisions of the income tax law to make the National pension system framework a little better and fair for all persons.

Here are some of the recommendations.

Employee provident fund Schemes were launched for all employees in the regulated sector to support them accumulate retirement assets. Primarily NPS was Implemented in 2004 for Govt employees & later expanded to all citizens of India.

Under the Employee provident fund scheme, the user gets all the accumulated funds to his credit as tax-free at his retirement with full rights to invest it as he wishes, while the National Pension System subscriber finds only up to 60 percent of the accumulated balance in his National Pension System account at the time of retirement as tax-free

For the balance 40 percent amount he has to compulsory buy annuity from any life insurance company registered with Insurance Regulatory and Development Authority.

In our point of view, why should the govt prescribe to the members of one scheme where it should spend its retirement people & encourage it to make full use of the way it wants in the other scheme also.

It is becoming essential especially in view of the fact that the annuities of insurance corporate usually do not give you returns that are capable of overcoming the inflation effect, furthermore, it will be entirely taxable in the hands of the annuitant.

Investments in mutual funds have now become safe with the growth of the mutual fund as an industry & tight regulatory monitoring.

The Govt of India should provide the National pension Scheme subscribers the freedom to invest in any item of their choice including a limitation on the complete withdrawal of the capital, in order to assure that the entire corpus is not placed at risk.

It should apply to the members/subscribers of the two schemes.

Tier I withdrawals are tax-free up to Sixty percent and the balance of Forty Percent must be used to purchase an annuity plan.

There is no proper clarity of the provision under the Income Tax Act which provides on how withdrawals from Tier II accounts should require to be taxed.

Although these are not products of the mutual fund, for which there exist exact rules, there is doubt and non-clarity of a provision of taxation of Tier II withdrawals.

There is no clarification as to whether the same could be regarded as an equity product and therefore eligibility to a concessional tax rate in the event that the subscriber opts for Seventy-five Percent or more of the equity portion.

Full clarification would go a long way towards clearing the clouds around Tier II account taxes treatment to be made. The Govt. of India should quickly bring in clarification about the taxation of withdrawals from the National Pension Scheme Tier II account.

Some Professionals claim that maximum value should be taxed, which is ridiculous in my view, but then clear cut-off provisions would support us to explain this.

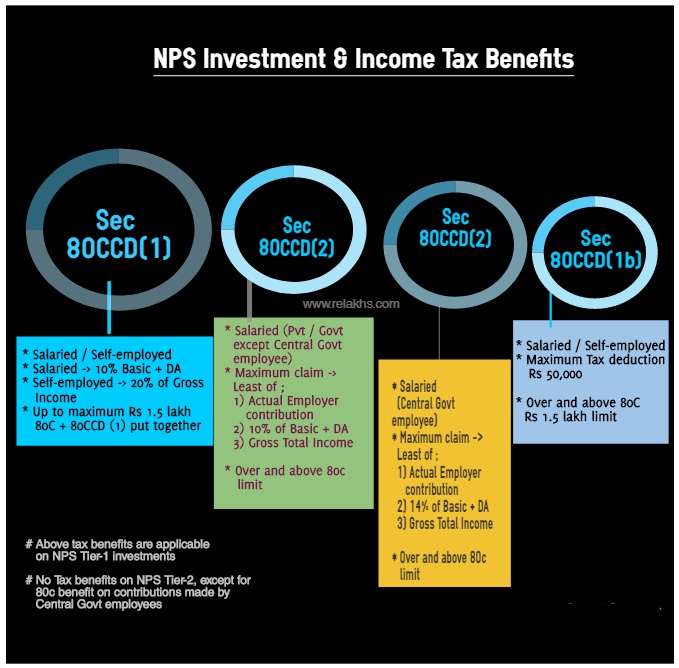

Currently, only employees of the Govt are permitted to claim a deduction u/s 80C of the Income-tax Act, for contributions made towards Tier II accounts with a locked-in period of 3 Years. Some subscribers do not have the same choice.

Tax advantages for Tier I account contribution, for employer’s contribution for Central Govt employees, are available up to fourteen percent, but for other employees, it is restricted to Ten percent that is qualified for deduction u/s 80CCD(2) of the Income Tax Act.

Again this indicates that the above NPS system is designed to support Central Govt workers relative to all other classes of employees. We do not see any obvious explanation for this partiality with others.

The Govt. of India should make the employer contribution part up to fourteen percent of the tax eligible for all classes of workers/ employees.

We believe that the Govt. of India should introduce amendments to fix these anomalies in order to make the scheme fair and just for each variety of Subscribers.

Popular blog:-

No Interest Deduction Allowed Against Dividend Income (Budget 2026 Update) Investors in stocks and mutual funds, particularly those who use… Read More

CBDT’s NUDGE Initiative Driving Compliance (AI vs. Tax Evasion) Meaning of NUDGE: NUDGE stands for Non-Intrusive Use of Data to… Read More

All about Goods and Services Tax on event entry tickets—recreational, cultural & sporting services Meaning of Recreational, Cultural & Sporting… Read More

Recent Amendments to FIU‑IND Regulations: What Businesses Need to Know Why the Amendments Were Introduced With the rapid rise of… Read More

All about Financial Intelligence Unit – India registration in 2026 With rising scrutiny over digital assets, cross‑border payments, and fintech… Read More

TDS & TCS Changes (Effective from 1 April 2026): Budget 2026 The Indian Financial Budget 2026 introduces a major overhaul… Read More

{kind=link}

{kind=link}