MCA Proposed the companies (CSPP) Amendment rule,2020The Companies (Corporate Social Responsibility) Regulations 2021 have been amended by the Ministry of Corporate Affairs with effect from 22 January 2021.

www.carajput.com; MCA Proposed the companies (CSPP) Amendment rule,2020

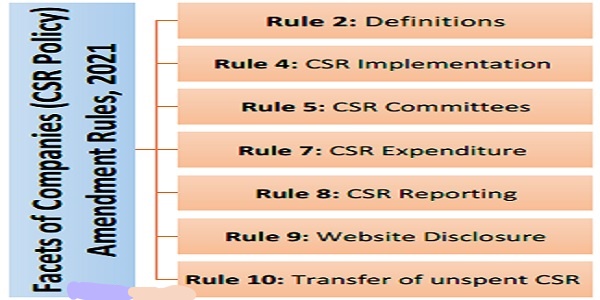

Major Highlights of Companies (CSR Policy) Amendment Rules, 2021

The Companies (Corporate Social Responsibility Policy) Amendment Rules, 2021 has been amended according to the MCA. The said rules majorly concerning the following facets;

CSR Implementation:

The Board shall ensure that the Corporate Social Responsibility activities are undertaken by the company itself or Via the following –

Society registered u/s 12A and 80G of Income Tax Act, 1961; or

The company with incorporated at least three years.

Section 8 Company;

Registered Public Trust;

Every business seeking to undertake Corporate Social Responsibility (CSR) activities should register with the central government itself.

The CSR-1 form should be filed electronically with the Registrar of Companies, with effect from 1 April 2021, and each company will be issued with a unique CSR registration number.

Moreover, on filing the MCA -Form CSR-1 with the Govt, a unique CSR Registration Number will be created by the system automatically.

Certified by Chief Financial Officer:

The Board of the Company shall facilitate the implementation of ongoing projects to ensure that the funds are used for approved purposes and shall be certified by the Chief Financial Officer (CFO) or the people in charge of finance.

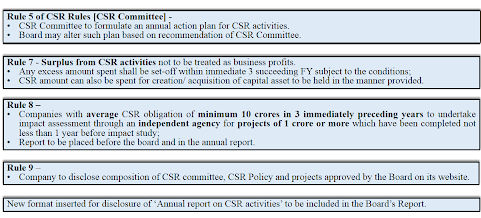

CSR Committees

: CSR Committee shall formulate & recommend to Board, an annual action plan in pursuance of its CSR policy, which shall include the are as follows:

the list of CSR projects/programs that are approved to be undertaken in areas or subjects specified in Schedule VII of the Company Act;

Manner of execution of such projects/programs as specified in Rule 4(1);

the modalities of utilization of funds and implementation schedules for the projects or programs;

monitoring & reporting system for projects/programs;

details of need & impact assessment, if any, for projects undertaken by the company

Board may alter such a plan at any time during the FY, as per the recommendation of its CSR Committee.

Companies carrying out CSR activities will now need to be more transparent by presenting the following information:

Impact Assessment for major projects in Corporate Social Responsibility (CSR).

Each year, in addition to Corporate Social Responsibility (CSR) policy amendments in Board Report reporting formats, an annual action plan for Corporate Social Responsibility (CSR).

Mandatory disclosure on the business website of CSR ventures and activities.

If a company fails to invest the mandated 2% of net profits on Corporate Social Responsibility (CSR), the reasons for that would have to be mentioned.

If the unspent amount does not correspond to any current project, the amount must be transferred to a notified government fund.

Previously, firms investing more than the mandated 2 percent would not have earned any government benefits.

Now, in the coming years, companies can set aside the excess amount expended against the CSR obligation. This will encourage businesses to keep the legislation flexible in perpetuity.

www.carajput.com; MCA Proposed the companies (CSPP) Amendment rule,2020

Administrative overheads shall not exceed 5% of total CSR expenditure:

www.carajput.com; MCA Proposed the companies (CSPP) Amendment rule,2020

CSR Expenditure: The board shall make sure that the administrative overheads shall not exceed five percent of the total CSR expenditure of the company for FY.

Any excess emerging from CSR activities shall be recovered from the same project or transferred to the Available to spend CSR Account & spent by the CSR policy and company’s annual action plan or transferred to the Fund referred to in Schedule VII within Six months of the end of the FY.

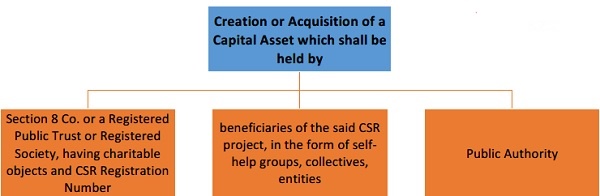

Any capital asset made by a company before the start of business (Corporate Social Responsibility Policy) Amending Rules, 2021, shall comply with the provisions of this rule within 180 days of such initiation, which may be extended by a further period of not more than 90 days with the board approval based on reasonable justification.

Before, violation of the results of Corporate Social Responsibility (CSR) operations will be deemed a criminal offense. It will now be classified as a civil offense, as per the latest laws. For corporate businesses, this is a major relief.

Earlier, through charitable organizations, businesses did not meet their CSR obligations. Companies are also only permitted to register ventures under public trusts, society, or Section 8 companies.

Projects carried out by charitable organizations would therefore be permitted as part of the company’s Corporate Social Responsibility (CSR) expenditure, provided that the project is separately registered with the MCA.

The Companies with CSR obligations below 50 lakhs are now exempted from the establishment of a CSR committee. Through their respective boards, they will now be allowed to fulfill this responsibility.

The Company may now engage with international design, monitoring, evaluation organizations and even create a team for their Corporate Social Responsibility (CSR) projects.

When Companies will either have to put back any surplus amount from CSR projects into the same project or have it shifted to the Unspent CSR account.

Companies with CSR obligations below 50 lakhs are now exempted from the establishment of a CSR committee. Through their respective boards, they will now be allowed to fulfill this responsibility.

Companies may now engage with international design, monitoring, evaluation organizations and even create a team for their CSR projects

Provisions with relation to acquisition of Capital Assets:

www.carajput.com; MCA Proposed the companies (CSPP) Amendment rule,2020

Companies will either have to put back any surplus amount from Corporate Social Responsibility (CSR) projects into the same project or have it shifted to the Unspent CSR account.

The CSR Reporting:

Companies with an average CSR obligation of 10 Crores or more in the three immediately preceding financial years shall carry out an impact assessment through an independent organization for projects of 1 crore or more required to complete not less than 1 year before undergoing an impact study.

Amendment to Rule 10: Transfer of unspent CSR: Till a fund is specified in Schedule VII for subsection (5) and (6) of section 135 of the Act, the amount of the unused CSR shall if any, be transferred by the company to any fund included within Schedule VII of the Act.

Current format incorporated for the disclosure of the ‘Annual Report on CSR Activities’ to be included in the report of the Board.

CSR Activities Display of on its website:

The Company BOD shall ensure compulsorily disclosure of the below on the Company website (if any):

About the CSR policy.

CSR Committee Composition,

Board Approved Projects & CSR Policy;

To improve transparency through the required disclosure of Corporate Social Responsibility activities and evaluation results, new rules have been introduced.

It is expected that this will raise the compliance burden on multinational companies.

These regulations, however, are also required to provide businesses with increased flexibility in meeting their Corporate Social Responsibility (CSR) obligations.

Rajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}