Page Contents

On February 1, 2021, the finance minister is scheduled to present a paperless Union budget and has her task cut out provided that the FY 2020-21 has been challenging and unprecedented for both the government and the common man.

Although the government has made many attempts to provide relief by stimulus packages, this year is a bigger challenge, as the balancing act of controlling the burgeoning fiscal deficit and taxpayer expectations would have to be managed.

Also read: Application for APEDA (RCMC) Registration

The government implemented a tax relief scheme if a person purchased goods or services during the period October 12, 2020, to March 31, 2021, instead of travelling.

These goods and services should be subject to a GST of 12% or more and payments should be made in an electronic medium.

For non-central government employees, the deemed LTC fare (as this tax relief is called) is up to Rs 36,000 per person and the entity has to pay 3 times the deemed fare in order to benefit from tax exemption.

The Finance Minister is expected to be able to extend the LTC cash voucher scheme from March 2021 to FY 2021-22 in order to improve consumer demand in the economy. This is more so because it will take time to return to its flourishing avtaar for actual travel.

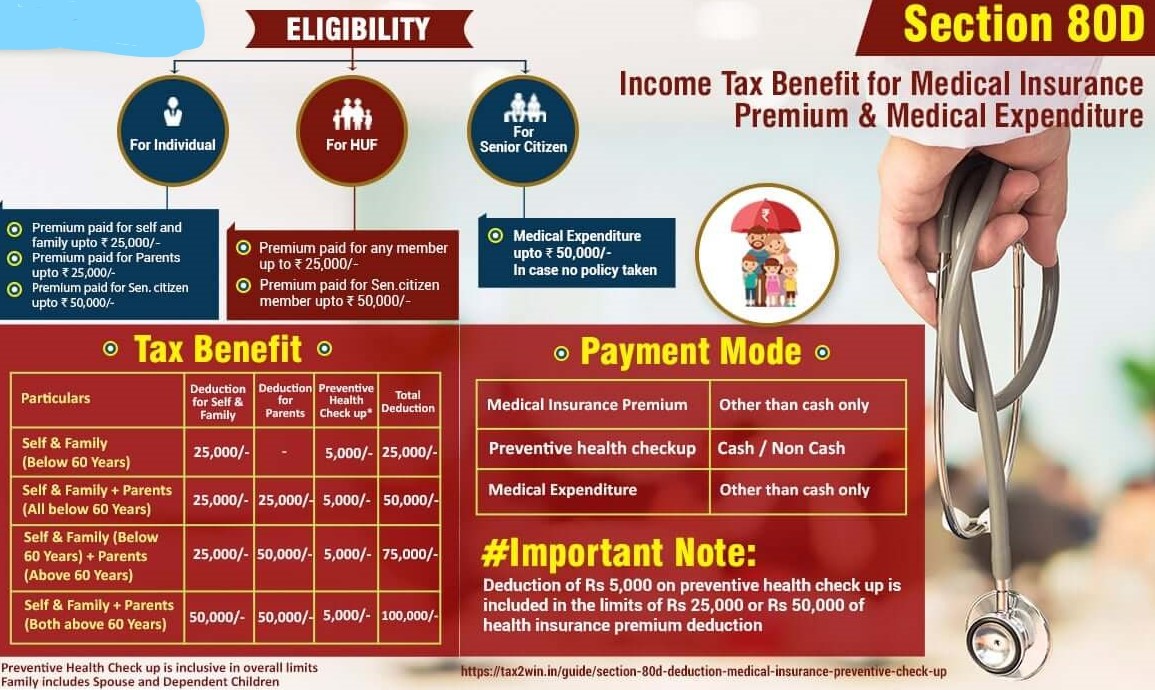

Current tax laws allow individual taxpayers to receive a medical insurance premium tax credit for themselves and their families.

In view of the current situation, the common man expects the finance minister to liberalize section 80D provisions and extend its reach to include medical expenditure on COVID-19 or any other illness sustained by taxpayers, without restricting the age or availability of medical insurance.

In addition, under section 80D, the currently recommended limits (Rs 25,000 to Rs 100,000, depending primarily on the age of the person and the coverage of family members) are not in line with the possible cost that an individual may incur. It is a demand that the total limit be raised to represent the reality on the ground.

Equity markets are at an all-time high and have stabilized from the downturn at the start of the outbreak of COVID-19. There is a clear argument that long-term capital gains are not affected by the tax rate (earned from the sale of shares on a stock exchange platform or equity mutual funds).

The government, however, may look to raise the rate of tax on such capital gains from the current 10 percent in order to obtain additional revenue. In addition, for taxpayers who own more than 2 properties, the tax rate on profits earned from the selling of home property can be raised.

The reform around the taxation of employee stock option profits – i.e. deferment of taxation to the event of selling of shares instead of taxation at the time of allotment of shares – is a long-running request that has maybe become more relevant in the last year. This will ensure more liquidity in individuals’ hands, especially with salary cuts replaced by stock options.

There is also discussion regarding the potential for the government to reintroduce tax-deductible infrastructure bonds where taxpayers subscribing to bonds are entitled to claim the deduction (subject to certain limits) of such expenditure from their gross income.

It will serve the dual purpose of providing taxpayers with a tax benefit as well as the much-needed inflow to enhance the infrastructure sector for the nation.

Another subject that is much debated is the implementation of estate duty or inheritance tax. Since 1985, when estate duty was abolished, the re-introduction controversy has emerged every now and then.

However, due to the extreme effect of COVID 19 on individuals/businesses, such a levy is unlikely to be introduced in the current Union Budget.

There seems to be mention of imposing a tax or duty on high-end luxury goods, but considering that the surcharge rates were just raised in 2019 (making the highest tax rate 42.7 %), in terms of expectations vs. real income collections, this will again take a lot of thought.

The Finance Minister Nirmala Sitharaman has their job cut out – this year is harder than others and apart from taxes or other problems concerning the personal finances of an individual, there are several issues of discussion – e.g. the new labor codes where there will be a possible effect on the net take home.

What we can perhaps say is that the probability of relief, cuts, and sops is not quite realistic with the fiscal deficit, but one can only predict – Feb 1 is going to be the day to look out for

Popular blog:-

MCA Changes in Indian Company formation- 2026 A series of reforms measures put forth by the Ministry of Corporate Affairs… Read More

Complete Guide to Reverse Charge Mechanism (RCM) under GST Under Goods and Services, tax is generally paid by the supplier…But… Read More

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

{kind=link}