Page Contents

The Govt granted relief in the TDS rates for the time frame 14.05.2020 to 31.03.2021 due to the disease outbreak and the resulting lock-down impacting all economic sectors.

The relief is constrained to the TDS rates only not to the rates at which the tax needs to be deducted or collected at a higher rate. Considering the situation of Covid-19, the TDS rates for payments made to resident Indians have been reduced by 25% for the time frame from 14 May 2020 to 31 March 2021.

Even so, there is no reduction in rates where the tax is needed to be deducted or obtained at a higher rate due to non-furnishing of PAN/Aadhaar.

TDS is withholding tax under the income tax deducted while payment made for the specified purpose (such as rent, commission, professional fees, salaries, interest, etc.) at the time of the transaction by persons making those payments,

Usually, the person earning the income is liable to pay income taxes. But the government, with the aid of the TDS, ensures that income tax is deducted in advance from the payments made by you.

The beneficiary of the income shall receive a net amount (after reducing TDS). The beneficiary will apply the gross amount to his income and the amount of the TDS will be adjusted against his final tax liability. The receiver shall take the credit of the balance already deducted and paid on his behalf.

When is the TDS to be deducted and by whom?

Any Person making specified payments referred to in the Income Tax Act is required to deduct TDS at the time of making such specified payments. But no Tax Deducted at Source must be deducted if the person making the payment is an individual or a HUF whose books are not expected to be audited.

Although, in the case of rent payments made by individuals and HUF above Rs 50,000 p.m., TDS @ 5 percent must be deducted even if the individual or HUF is not liable for tax audits. In addition, those individuals and HUF who are liable to deduct TDS @5 percent do not need to apply for TAN.

Your employer deducts TDS at the applicable income tax rate. Banks subtract TDS by 10%. Or they can deduct up to 20% if they don’t have your PAN details. For the most part, the TDS payment rates are set out in the Income Tax Act and the TDS is deducted by the payer on the basis of these prescribed rates.

If you have submitted investment evidence (for deductions) to your employer and your gross taxable income is below the taxable ceiling, you do not have to pay any tax. Therefore, no TDS should be deducted from your taxes. In the same way, you should apply Form 15G and Form 15H to the bank if your total income is below the taxable limits so that you do not deduct TDS on your interest income.

In the case that you have not been able to provide proof to your employer or that your employer or bank has already deducted TDS and that your gross income is below the taxable limit – you can file a return and demand a refund of this TDS. The complete list of Defined Payments eligible for the TDS deduction along with the TDS rate.

Tax deduction at source (TDS) Rates Chart Assessment Year 2022-23 or Financial Year 2021-22

Tax deduction at source (TDS) Rates in Effect for Fiscal Year 2021-22, Is there any change as a result of COVID, such as the 25% reduction in tariffs last year?

TDS(Tax deduction at source) Rates Chart for Assessment Year 2022-23 or Financial Year 2021-22 is shown below. I hope you find it useful as well.

| Under Section | Nature of Payment for the purpose of | Threshold limit | Tax deduction at source (TDS) Rates % |

| U/s 192 | Income from Salary | As per Income Tax Slab provided In act | Tax Slab rates |

| 192A | Premature withdrawal- EPF | INR 50,000 | 10% If no Pan, TDS @ 30% |

| 193 | Securites Interest received | INR. 10,000 | 10% |

| 193 | Debentures Interest | INR 5,000 | 10% |

| 194 | Dividend (Dividend other than listed companies) | INR 5,000 | 10% (No TDS on Div Payouts by REITs / InvITs) |

| 194 A | Interest other than on securities by banks / post office | INR. 40,000 (INR 50,000 for Senior Citizens) | 10% |

| 194 A | Interest other than on securities by other | INR. 5,000 | 10% |

| 194 B | Income from Winnings from Puzzle / Game/ Lotteries / | INR. 10,000 | 30% |

| 194 BB | Income from Winnings from Horse Race | INR. 10,000 | 30% |

| 194 D | Insurance Commission (Form 15G/H can be submitted) | INR. 15,000 | 5% (Individuals) 10% (Companies) |

| 194DA | Life Insurance Policy Payment | INR 1,00,000 | 5% |

| 194E | Non-resident sportsmen / sports association Payment | – | 20% |

| 194 EE | NSS Deposits Payment | INR 2,500 | 10% |

| 194 G | Lottery tickets sale Commission | INR 15,000 | 5% |

| 194 H | Brokerage or Commission | INR 15,000 | 5% |

| 194 I | Land, Building or Furniture rent | INR. 2,40,000 | 10% |

| 194I | Plant & Machinery rent | INR. 2,40,000 | 2% |

| 194 IB | Other Rent (Tenant has to deduct TDS) (Individuals who are not liable to Tax Audit) | INR 50,000 (per month) | 5% |

| 194 IA | Immovable Property Transfer, other than Agricultural land | INR. 50 lakhs | 1% |

| 194IC | monetary consideration under Joint Development Agreements Payment | – | 10% |

| 194J | professional or technical services Fees | INR 30,000 | 2% (or) 10% |

| 194LA | compensation on acquisition of certain immovable property Payment | INR 2,50,000 | 10% |

| 194 LB | Infrastructure Bond to NRI Interest | NA | 5% |

| 194 LD | certain bonds and govt. Securities Interest | NA | 5% |

| 194N | Cash withdrawal during the Last Year from 1 or more A/s maintained by a person on with a banking company, co-operative society engaged in business of banking or a post office: | > INR 1cr | 2% |

| 194Q | Purchase of goods (applicable w.e.f 01.07.2021) | INR 50 lakh | 0.10% |

| 206AB | TDS on non-Filing of ITR at higher rates (applicable w.e.f 01.07.2021) | – | 5% or 2 time of the rates in force |

| 194P | Tax deduction at source on Senior Citizen above 75 YeaINR (No ITR filing cases) | – | Slab Rates |

Basis Understanding about The TDS Concept then follow The Link

Now, let’s take a look at the TDS/TCS rates for the financial year 2020-21 as per the news release issued by the Ministry of Finance on 13 May 2020: The benefit of revision applies to only Resident Indians. As a result, Non-residents cannot take the claim advantages of the same.

New Revised TDS Rates applicable for FY 2020-21 relevant Assessment Year 2021-22 w.e.f 14th May 2020

| Nature of Payment | Basic Cut off (Rs.) | Individuals /Company and others New Rate %) | If No Pan or Invalid PAN (Rate %) | Individuals /Company and others (Old Rate %) |

| 192 – Salaries | Slab Rate | Slab Rates | 22.5% | Slab Rates |

| 192A- Premature withdrawal from Employee Provident Fund | 50000 | Individual: 7.5% Company: NA | 15% | Individual: 10% Company: NA |

| 193 – Interest on securities | – | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10%` |

| 194B – Winning from Lotteries | 10000 | Individual: 22.5% Company: 22.5% | 22.5% | Individual: 30% Company: 30% |

| 194BB – Winnings from Horse Race | 10000 | Individual: 22.5% Company: 22.5% | 22.5% | Individual: 30% Company: 30% |

| 194C- Payment to Contractor – Single Transaction | 30000 | Individual: 0.75% Company: 1.5% | 15% | Individual: 1% Company: 2% |

| 194C-Payment to Contractor – Aggregate During the Financial year | 100000 | Individual: 0.75% Company: 1.5% | 15% | Individual: 1% Company: 2% |

| 194C- Contract – Transporter not covered under 44AE | 30000 / 75000 | Individual: 0.75% Company: 1.5% | 15% | Individual: 1% Company: 2% |

| 194C- Contract – Transporter covered under 44AE & submit declaration on prescribed form with PAN | – | – | 15% | – |

| 194D – Insurance Commission | 15000 | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194DA Payment in respect of life insurance policy | 100000 | Individual: 0.75% Company: 0.75% | 15% | Individual: 1% Company: 1% |

| 194E – Payment to Non- Resident Sportsmen or Sports Association | – | Individual: 20% Company: 20% | 15% | Individual: 15% Company: 15% |

| 194EE – Payments out of deposits under National Savings Scheme | 2500 | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194F – Repurchase Units by MFs | – | Individual: 15% Company: 15% | 15% | Individual: 20% Company: 20% |

| 194G – Commission – Lottery | 15000 | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194H – Commission / Brokerage | 15000 | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194I – Rent – Land and Building – furniture – fittings | 240000 | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194I – Rent – Plant / Machinery / equipment | 240,000 | Individual: 1.5% Company: 1.5% | 15% | Individual: 2% Company: 2% |

| 194IA -Transfer of certain immovable property other than agriculture land | 50,00,000 | Individual: 0.75% Company: 0.75% | 15% | Individual: 1% Company: 1% |

| 194IB – Rent – Land or building or both | 50000 per month | Individual: 3.75% | 15% | Individual: 5% |

| 194IC – Payment of Monetary consideration under Joint development agreement | – | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194J – Professional Fees for technical services (w.e.f. from 1.4.2020) | 30000 | Individual: 1.5% Company: 1.5% | 15% | Individual: 2% Company: 2% |

| 194J – Professional Fees in all other cases | 30000 | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194K- Payment of any income in respect of Units of Mutual fund as per section 10(23D) or Units of an administrator or from a specified company | – | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194LA – TDS on compensation for compulsory acquisition of immovable Property | 250000 | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194 LBA (1)- Business trust shall deduct tax while distributing, any interest received or receivable by it from a SPV or any income received from renting or leasing or letting out any real estate asset owned directly by it, to its unitholders. | Individual: 7.5% Company: 7.5% | 0 | Individual: 10% Company: 10% | |

| 194LB – Income by way of interest from infrastructure debt fund (non-resident) | – | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194LBB – Income in respect of investment in Securitisation trust. | – | Individual: 7.5% Company: 22.5% | 30% | Individual: 10% Company: 30% |

| 194LBC- Income in respect of investment made in a securitisation trust | – | Individual: 18.75% Company: 22.5% | 30% | Individual: 25% Company: 30% |

| 194 LC – Income by way of interest by an Indian specified company to a non-resident / foreign company on foreign currency approved loan / long-term infrastructure bonds from outside India | – | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194LD – Interest in certain bonds and govt. Securities | – | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194M – Payment of Commission, brokerage, contractual fee, the professional fee to a resident person by an individual or a HUF who are not liable to deduct TDS under section 194C, 194H, or 194J. | 50,00,000 | Individual: 3.75% Company: 3.75% | 15% | Individual: 5% Company: 5% |

| 194N – Cash withdrawal in excess of Rs. 20 Lakh during the previous year from one or more account maintained by a person with a banking company, co-operative | 20,00,000 | Individual: 1.5% Company: 1.5% | 15% | Individual: 2% Company: 2% |

| society engaged in the business of banking or a post office. | ||||

| 194N – Cash withdrawal in excess of Rs. 1 crore during the previous year from one or more account maintained by a person with a banking company, co-operative society engaged in business of banking or a post office. | 100,00,000 | Individual: 1.5% Company: 1.5% | 15% | Individual: 2% Company: 2% |

| 194O- Applicable for E- Commerce operator for sale of goods or provision of service facilitated by it through its digital or electronic facility or platform. | – | Individual: 0.75% Company: 0.75% | 15% | Individual: 1% Company: 1% |

| 194 – Dividend other than the dividend as referred to in Section 115-O | 2500 | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194A – Interest other than interest on securities – Others | 40000 (for individual) | Individual: 7.5% | 15% | Individual: 10% Company: 10% |

| 194A – Banks (Time deposits) | 40000 (for individual) 50000 (for Senior Citizens only) | Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 194A – Banks (Recurring deposit) | 40000 (for individual) 50000(for Senior Citizens only) | Individual: 7.5% | 15% | Individual: 10% Company: 10% |

| 194A – Deposit in Co-op Banks | 40000 (for individual) 50000(for Senior Citizens only) | Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 195- Payment of any sum to Non resident | – | – | Higher of Rate in force or Double Taxation Avoidance Act rate | – |

| 196B – Income from units | – | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 196C-Income from foreign currency bonds or GDR (including long-term capital gains on transfer of such bonds) (not being dividend) | – | Individual: 7.5% Company: 7.5% | 15% | Individual: 10% Company: 10% |

| 196D – Income of FIIs from securities | – | Individual: 20% Company: 20% | 15% | Individual: 15% Company: 15% |

*This is further mentioned that there is no reduction in the rates of TDS or TCS where the tax is needed to be deducted or collected at a rate higher due to the failure to provide the PAN/Aadhaar.

For instance, if the tax is needed to be subtracted at 20% under section 206AA of the Income Tax Act due to non-furnishing of PAN/Aadhaar, it shall be deducted at a rate of 20% and not at a rate of 15%.

In case of non-furnishing of PAN/Aadhaar by collectee, TCS will be charged at twice of the normal rate applicable or 5% {1% in case of sale of any goods (given in the last point) of the value exceeding 50 Lacs}, whichever is higher.

Note: In the event of non-furnishing of PAN/Aadhaar by collection, TCS shall be charged at 2 times of normal TDS rate applicable or 5% {1 percent in the case of sale of any goods (given in the last paragraph) with a value exceeding 50 Lacs}, whichever one is higher.

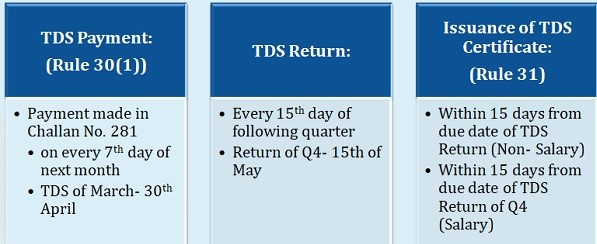

Form 16/16A is a certificate of deduction of tax at source issued by the employer on behalf of employees on the deduction of tax. These certificates help in providing TDS/TCS information for the trading activities between the deductor and the deductee. These certificates must be issued to taxpayers.

In the case of delays in depositing TDS or errors in filing TDS returns, the following penalty applies:

Failure to file your TDS returns within the deadline means that you will be subject to a late filing fee of Rs.200 each day. The fee will be paid every day after the due date, till the date on which your return is filed. However, the maximum fees that you will have to pay will be limited to the amount of the TDS.

In case of TDS returns are filed after the deadline or there is a mismatch in the return form, the following penalties shall become applicable:

The penalty under Section 234E: under this section of the Income Tax Act, the deductor will be fined Rs.200 each day until the TDS is paid, but the penalty cannot be more than the TDS sum.

The penalty referred to in Section 271H: penalty which can vary from a minimum of Rs.10,000 to a maximum of Rs.1 lakh. A penalty will not be paid under Section 271H of the Income Tax Act in the case that TDS/TCS returns are not filed within the deadline, provided that the following conditions apply:

a). The TDS/TCS shall be paid to the Government’s credit.

b). The filing of the TDS/TCS return shall take place before the expiry of 1 year from the deadline.

c). Interest and delayed filing fees (if there are any) have been charged to government credit.

Under Section 201(1A) of the Income Tax Act, 1961, if the tax is not deducted at source, either in part or in full, an interest rate of 1% pm would apply from the date on which the tax was subtracted to the date on which it was actually subtracted.

COLLECTION AND RECOVERY OF TAX – WHEN TAX PAYABLE AND WHEN ASSESSEE DEEMED IN DEFAULT SECTION 220 :

Stay of demand: The power of the Assessing Officer under section 220(6) cannot be said to be a power to grant stay against recovery of disputed demand and or mere filing of an appeal does not suo-moto stay recovery proceedings.

A new window has been enabled for claiming TDS/TCS credits. The taxpayer has the option of accepting or rejecting the TDS/TCS credits available and filing their return, after which the credits get transferred to the cash ledger and can be used for making GST payments.

The applicable TDS rates relevant for the FY 2020-21 appeared first on Rajput Jain and Associates

Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@carajput.com or call at 9555555480

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}