Page Contents

There are some provisions to make payments outside India, one of this compliance is the submission of Form 15CA and 15CB compliance. Rule 37BB provides the manner of supplying information in form 15CB and making a declaration in form 15CA.

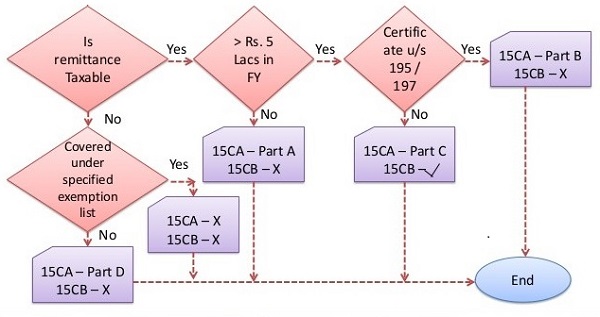

In 15CA, all the information concerning payments made to non-residents is given, making it a tool for the collection of data on international remittances. In general, this form is a statement used by the sender to gather information on payments due.

Form 15CA is a declaration statement of any person who is planning to make a foreign remittance:

Non-requirement of Form 15 CA

This is the kind of certificate that is required only if the remittance is not taxable. It is a channel for getting tax clearance/approval. In general, this form is a declaration used by the remitter to gather information on payments due.

Form 15CB certificate is required from Chartered Accountant when the foreign remittance is made in the following case

Form 15CB is a form that a Chartered Accountant is required to sign. This certificate is regarding the rate and the correct type of tax paid by Assess. some information Form 15CB is requested at the time of submission of Form 15CA.

It appears at first glance that Form 15CA is not necessary to be completed if the remittance or payment to a non-resident Indian is not taxable.

According to Rule 37BB of the Income Tax (14th Amendment) Rule, 2013, There is no reporting of Form 15CA & Form 15CB in the case of international remittances of the following nature since October 2013.

| Purpose code as per RBI | Nature of Payment |

| S0001 | Indian investment abroad -in equity capital (shares) |

| S0002 | Indian investment abroad -in debt securities |

| S0003 | Indian investment abroad -in branches and wholly-owned subsidiaries |

| S0004 | Indian investment abroad -in subsidiaries and associates |

| S0005 | Indian investment abroad -in real estate |

| S0011 | Loans extended to Non-Residents |

| S0202 | Payment- for operating expenses of Indian shipping companies operating abroad. |

| S0208 | Operating expenses of Indian Airlines companies operating abroad |

| S0212 | Booking of passages abroad -Airlines companies |

| S0301 | Remittance towards business travel. |

| S0302 | Travel under basic travel quota (BTQ) |

| S0303 | Travel for pilgrimage |

| S0304 | Travel for medical treatment |

| S0305 | Travel for education (including fees, hostel expenses, etc.) |

| S0401 | Postal services |

| S0501 | Construction of projects abroad by Indian companies including import of goods at the project site |

| S0602 | Freight insurance – relating to import and export of goods |

| S1011 | Payments for maintenance of offices abroad |

| S1201 | Maintenance of Indian embassies abroad |

| S1 202 | Remittances by foreign embassies in India |

| S1301 | Remittance by non-residents towards family maintenance and-savings |

| S1302 | Remittance towards personal gifts and donations |

| S1303 | Remittance towards donations to religious and charitable institutions abroad |

| S1304 | Remittance towards grants and donations to other governments and charitable institutions established by the Governments. |

| S1305 | Contributions or donations by the government to international institutions |

| S1306 | Remittance towards payment or refund of taxes. |

| S1501 | Refunds or rebates or reduction in invoice value on account of exports |

| S1503 | Payments by residents for international bidding”. |

Popular Article :

MCA Changes in Indian Company formation- 2026 A series of reforms measures put forth by the Ministry of Corporate Affairs… Read More

Complete Guide to Reverse Charge Mechanism (RCM) under GST Under Goods and Services, tax is generally paid by the supplier…But… Read More

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

{kind=link}