Page Contents

Note: Rule 3(7) states under the heading Explanation “If ratification of appointment is not made by the members in the Annual General Meeting, the Board shall appoint another individual or Firm as Auditors as per procedures laid down under the Act.’

This is contrary to the provisions contained in Section 139(10) wherein it states if no auditor is appointed or reappointed, the existing auditor shall continue to be the auditor of the Company.

a. An Auditor matching his qualification and experience with the size and requirements of the Company shall be chosen by the Board.

b. The Board shall then see whether there are any orders or pending proceedings relating to professional matters of conduct against the proposed Auditor before ICAI or any other competent Authority.

c. The Board has to see whether he satisfies the eligibility norms specified under Section 141.

d. The Board has to obtain a declaration from the Auditor that he is eligible to issue a certificate under rule 4(1).

Note: Asper Rule 4(1), the Company has to get the eligibility certificate after the Auditor is appointed in the AGM. What if the management finds out if the Auditor is ineligible to issue the certificate after he is appointed.

e. The Board has to finalize the remuneration payable to the Auditor in consultation with him and pass the resolution in the Board subject to the approval of the shareholders in the AGM.

Section 142 requires the Company to quantify the remuneration in the General Meeting.

Note: Hitherto, under the Companies Act, 1956, The Company had the privilege to appoint Auditors in the AGMs on a remuneration that could be decided by the Board at a later date. That era is over.

f. With the Board’s consent on the Appointment as well as on the remuneration, the intended resolution to be passed could be mentioned in the AGM NOTICE itself. Here is the model resolution.

“Resolved that in accordance with the provisions of Section 139, 141 and 142 of the Companies Act, 2013 read with rule 3(7) of the Companies (Audit and Auditor) Rules, 2014, M/s.ABC & Co, Chartered Accountants, Bangalore is and are hereby appointed as Statutory Auditors of the Company so as to hold the said office from the conclusion of this meeting till the conclusion of the sixth AGM on a consolidated remuneration of Rs.22,000 (Rupees twenty-two thousand four hundred and seventy-two only) for each Audit period unless otherwise revised subsequently at the time of ratifications in the subsequent Annual General Meetings”.

“Resolved further that M/s ABC & Co, Chartered Accountants, Bangalore shall in addition to the above remuneration be eligible to reimbursement of all expenses incurred during the course of Audit and availing all such facilities as are extended to them during Audit”.

g. The Company shall file an E Form in ADT–1 intimating the Registrar about the appointment of Auditors within 15 days from the date of his appointment

h. Company shall also inform the Auditors about his appointment in the AGM within 15 days of his appointment.

i. Instead of the Board, the Audit Committee has to go through the process of selection of Auditors as mentioned in Clause (a) to (e) and then recommend to the Board which in turn recommends to the Members for consideration in the AGM.

ii. If the Board disagrees with the recommendation of the Audit Committee, it shall refer back again to the said Committee citing the reason for disagreement and recommending reconsideration.

iii. In case the Audit committee decides not to reconsider the recommendations made by the Board, the Board shall then record the reason for disagreement and send its own recommendations for consideration to the members to decide in the Annual General Meeting.

The Auditor appointed by the Members or by the Board as the case may be shall submit a certificate stating that

i. he is eligible for appointment and is not disqualified for appointment under the Companies Act, 2013, the chartered Accountants Act, 1949, and the rules and regulations made thereunder.

ii. The proposed appointment is as per the terms provided under the Act.

Note: Section 141 and rule 10 list out the eligibility criteria for the Auditors and Section 144 list out services that he should not render either directly or indirectly while serving as Auditor

iii. the proposed appointment is within the specified limits laid under the Act.

iv. List of proceedings against the Auditor or Audit firm or any partner of the Audit firm pending with respect to professional matters of conduct as disclosed in the certificate is true and correct.

a. In the case of a casual vacancy caused by the resignation of the Auditor, the following procedures have to be followed.

i. The Board of Directors shall approve the filling up of the casual vacancy within thirty days and then recommend such appointments to the members.

ii. Members in an Extra-Ordinary General Meeting shall confirm and approve the vacancy filled up by the Board on its recommendations within three months.

b. In the case of a casual vacancy caused by any other reason other than the resignation of the Auditor, the Board of Directors has the powers to fill such a vacancy within thirty days.

c. If the Companies have Audit Committee, filling up of casual vacancy shall be done after taking into account the recommendation of such a Committee in addition to the recommendation of the Board.

The Appointed Auditor shall hold office till the conclusion of the next Annual General Meeting

i. The Comptroller and Auditor General of India shall fill up the casual vacancy within thirty days.

ii. In case the casual vacancy is not filled as mentioned in (i) above, the Board of Directors shall fill such vacancy within the next 30 days.

As per Section 139(9) of the Act, the retiring Auditor shall be reappointed at an Annual General Meeting if

i. retiring Auditor is not disqualified for reappointment

ii. he has not given the company a notice of unwillingness to be reappointed.

iii. A special resolution is passed at the Annual General Meeting appointing some other auditor or providing expressly that he shall not be reappointed.

iv. The retiring Auditor shall continue to remain as Auditor till the end of this term viz., the conclusion of the sixth Annual General Meeting if no other auditor is appointed or reappointed.

Note: This is contrary to rule 3(7) as mentioned earlier.

i. The Auditor shall conduct the Statutory Audit the manner in which it is laid down under Section 143.

ii. Auditor in his report shall specify all matters as are enumerated in Section 143 and Rule 11.

iii. In case of fraud, the Auditor shall report in the manner laid under Rule 13.

iv. Section 146 requires the Auditor to attend either by himself or through his authorized representative who shall be qualified to be an Auditor at all general meetings and he shall have the right to be heard on any part of the business that concerns him. (However, the Company may exempt the Auditor in complying with this provision)

The auditor shall not render either directly or indirectly to the Company, or its Holding or Subsidiary Company the following services.

a. Accounting and Bookkeeping service.

c. Design and Development of any financial information system

d. Actuarial Services

e. Investment advisory services

f. Investment Banking Services

g. Rendering of outsourced financial services

h. Management Services

Any other services as may be prescribed by the Government.

The term of office of an Individual Auditor shall be for five years and for a firm of Auditors shall be for two consecutive terms of five years for the following classes of Companies.

However, the Act has given time to comply with the above provisions by the aforesaid companies within a period of three years viz., on or before 31–3–2017.

Note:

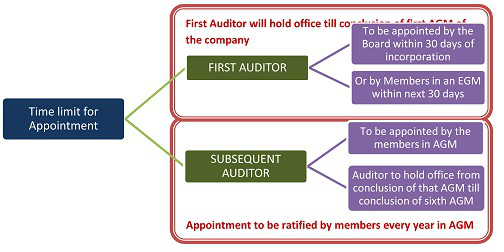

Tenure: – Till the conclusion of the 1st annual general meeting.

Remuneration: – As per proviso to section 142(1) remuneration of the first auditor can be decided by the Board.

As per section 139(1), every company shall appoint at its 1st annual general meeting an individual or a firm as an auditor of the company who shall hold office who shall hold office from the conclusion of that meeting till the conclusion of its sixth AGM and thereafter till the conclusion of every sixth AGM meeting

Tenure subject to ratification:- The tenure of 5 consecutive years is subject to ratification by shareholders at every AGM.

Remuneration: –As per section 142(1) remuneration of the auditor of a company shall be fixed in its general meeting or in such manner as may be determined therein.

Manner & Procedure for selection to be governed through rules:- it is prescribed in rule 3, explained hereunder,

1. Consideration of the appointment – The Board or the Audit Committee (where it is required to be constituted) shall consider the qualifications, experience of the auditor, and whether the aforesaid attributes are commensurate with the size and requirements of the company.

Further regard should also be given to professional matters of conduct against the proposed auditor before the ICAI, Court, or any competent authority.

The procedure depends upon whether the audit committee is required to be constituted or not.

However, if the committee decides not to do so then the Board shall record reasons for its disagreement with the committee and send its own recommendation for consideration of the members.

The company shall inform the auditor regarding the appointment and also file a form ADT-1 to ROC within 15 days of the meeting in which the auditor is appointed.

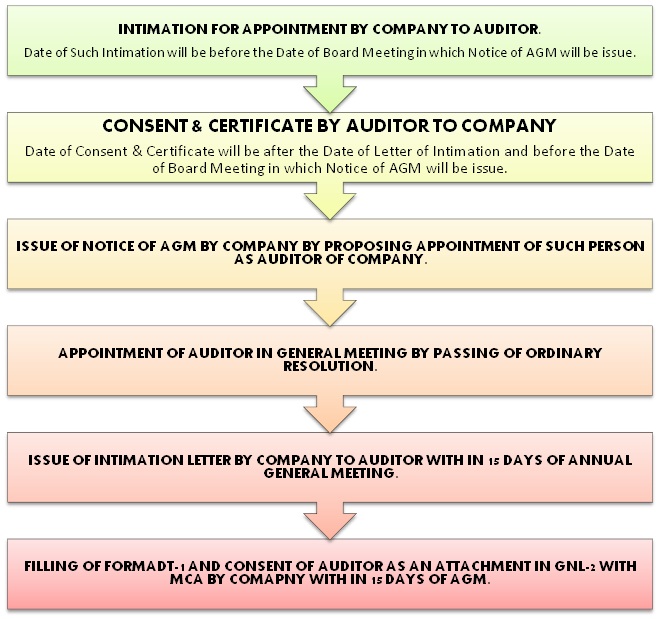

1. Intimate the proposed auditor(s) regarding the intention of appointing him/it as an auditor and ask for the following information and documents:-

2. Call Board meeting for the purpose of following:-

3. Convene the AGM and get the Ordinary resolution appointing the auditor passed at the meeting.

4. Intimate the Auditor and file with ROC form ADT-1(to be attached in form GNL-2 as per MCA circular 09/2014 dated 25th April 2014) within 15 days.

Note: – In case the Company is required to constitute the Audit Committee, then the work of consideration and recommendation vests with it. The concept of the same has been discussed above.

Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@carajput.com or call at 011-435 201 94

Popular blog:-

Summary of the Proposed Amendments to the IBBI Liquidation Regulations (2026) The document proposes major changes to India's liquidation… Read More

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}