Page Contents

Q.: Is the new section mentioned u/s 206C(1H)?

Q.: Is the new section mentioned u/s 194Q TDS on purchases of goods?

Person Responsible for Deducting TDS

Basically, the buyer is responsible for paying any resident for the purchase of goods of the value or aggregate of such value in excess of INR 50 Lakh in the last year and is liable to deduct TDS.

Applicability of Section 194Q

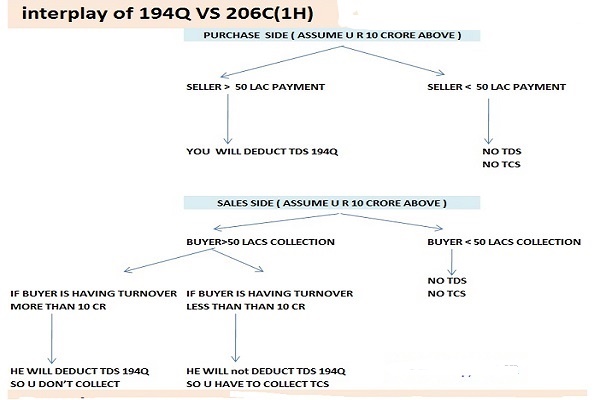

The buyer has the primary and main obligation to deduct the tax under Section 206C, and no tax shall be collected on the transaction (1H). Nevertheless, the seller is accountable for collecting the tax if the buyer fails to do so.

If a transaction is subject to both TDS and TDS under section 194Q, the TDS under section 194Q will apply. TDS u/s 194Q is not applicable if TCS is eligible to be collected under any other provisions of Section 206C.

Read also : Extension of TDS/TCS statement filing Date

More read for related blogs are: New revise TDS/TCS due date for filing a return and Payment for the year 2020

Q.: What should you do if TDS is required to be deducted under another section and TDS u/s 194Q also applies to a transaction?

The provisions of Section 194Q are not applicable if TDS is required to be deducted under any other section of the Income Tax Act.

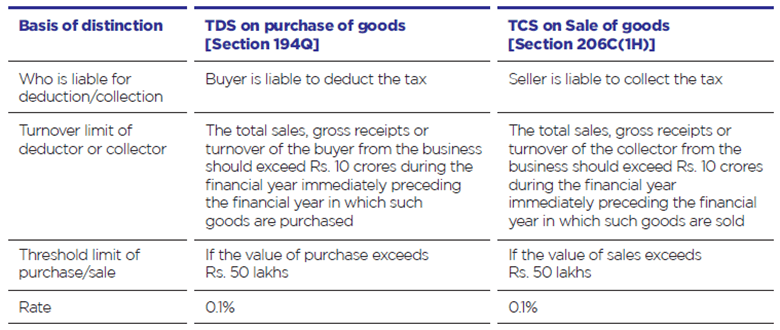

Comparison of 194Q and 206C (1H):

Basis of comparison | TDS on purchase of goods | TCS on Sale of goods |

| Who is liable for deduction/collection | Buyer is liable to deduct the tax | Seller is liable to collect the tax |

| Turnover limit of deductor or collector | The total sales, gross receipts or turnover of the buyer from the business should exceed Rs. 10 crores during the financial year immediately preceding the financial year in which such goods are purchased | The total sales, gross receipts or turnover of the collector from the business should exceed Rs. 10 crores during the financial year immediately preceding the financial year in which such goods are sold |

| Effective date | 1st July 2021 | 1st October 2020 |

| Rate | 0.1% | 0.1% (0.075% for FY 2020-21) |

| Amount on which tax to be deducted/collected | On the amount of purchase in excess of Rs. 50 lakhs | On the amount of sale consideration received in excess of Rs. 50 lakhs |

| PAN not available | 5% | 1% |

| Time of deduction/collection | At the time of credit or payment, whichever is earlier | At the time of receipt |

| Exclusions | Not applicable if a. Tax is deductible under other provisions of the act b. Tax is collectible under 206C other than 206C (1H) | If Buyer is a. Importer of goods b. Central/State Government, Local Authority c. An embassy, High Commission, legation, commission, consulate and trade representation of a foreign state |

| Preference to be given | Purchaser is first liable to deduct the tax if the transaction could be subject to both provision | Seller shall be liable to collect the tax only if the purchaser is not liable to deduct the tax or purchaser failed to deduct tax |

| When to deposit/collect | Tax so deducted shall be deposited with government by 7th day of subsequent month | Tax so collected shall be deposited with government by 7th day of subsequent month |

| Quarterly statement to be filed | 26Q | 27EQ |

| Certificate to be issued to seller/buyer | FORM 16A | FORM 27D |

Read also : key features of TCS on goods sale section-206c

Example 1

| Particulars (assumed that the transactions have occurred after 01st July 2021) | Scenario 1 | Scenario 2 | Scenario 3 |

| Turnover of Seller (In cr.) | 12 | 6 | 12 |

| Turnover of Buyer (In cr.) | 6 | 12 | 12 |

| Sale of goods (In cr.) (A) | 2 | 2 | 2 |

| Sales consideration paid during the year (In cr.) (B) | 1 | 1 | 1 |

| Who is liable to deduct or collect tax? | Seller | Buyer | Buyer |

| Rate of Tax (Seller/Buyer has provided PAN and has satisfied section 206AB) | 0.1% | 0.1% | 0.1% |

| Amount on which tax to be deducted or collected (In Cr.) [Amount in excess of Rs. 50,00,000 is the taxable amount] | 0.5 [(B) – 0.5] | 1.5 [(A) – 0.5] | 1.5 [(A) – 0.5] |

| Tax to be deducted or collected | 5,000 | 15,000 | 15,000 |

Example 2

| Seller’s Turnover | Buyer’s Turnover | Sale or purchase consideration for goods (after 1st July 2021) | Taxable amount | Seller / Buyer PAN | TDS | TCS | Obligated Person to deduct or collect tax | Relevant Section |

| (in Crores | (in crores) | (in lakhs) | ||||||

| 7 | 15 | 55 | 5 | Yes | 0.10% | NA | Buyer | Section 194Q |

| 15 | 6 | 59 | 9 | Yes | NA | 0.10% | Seller | Section 206C(1H) |

| 18 | 16 | 65 | 15 | Yes | 0.10% | NA | Buyer | Section 194Q |

| 5 | 11 | 53 | 3 | No | 5% | NA | Buyer | Section 194Q/ 206AA |

| 16 | 7 | 56 | 6 | No | NA | 5% | Seller | Section 206C(1H)/ 206AA |

Example 3 –

Mr. A, a buyer with an annual revenue of INR 50 crores. Mr. A buys products valued INR 52 lakhs from Mr. B, a seller.

The following is an analysis of the applicability of section 194Q in the current transaction:

The buyer will be able to deduct TDS under section 194Q in the following way:

| Particulars | Amount |

| Taxable amount (INR 52 Lakhs – INR 50 Lakhs) | INR 2 Lakhs |

| Rate at which TDS deductible under section 194Q | 0.1% |

| Amount of TDS deductible | INR 200 |

Example 4 –

Mr. X, a buyer, has INR 40 crores in gross receipts. Mr. X purchases goods worth INR 60 lakhs from Mr. Y. Notably, Mr. Y, a seller, has a revenue of INR 15 Crores.

The following is a description of how the provisions of Section 194Q were applied in the above transaction:

Because both provisions, namely sections 194Q and 206C(1H), are applicable. TDS is only deductible under Section 194Q, as shown in the table below.

| Particulars | Amount |

| Taxable amount (INR 60 Lakhs – INR 50 Lakhs) | INR 10 Lakhs |

| Rate at which TDS deductible under section 194Q | 0.1% |

| Amount of TDS deductible | INR 1000 |

TCS on sale of Goods under section 206(1H) will NOT APLLICABLE from 1.April 2025

Read also : New TDS deduction No cash transactions exceeding 1 Crore -Section 194N

For query or help, contact: info@caindelhiindia.com or call at +91 9555 555 480

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

Tax Dept introduced a new reporting field in Schedule Exempt Income for AY 2026-27 The Income Tax Department has introduced… Read More

Digital Personal Data Protection (DPDP) Act, 2023: Complete Compliance Guide, Requirements, Penalties & Implementation Framework The Digital Personal Data Protection… Read More

{kind=link}

{kind=link}

{kind=link}