Page Contents

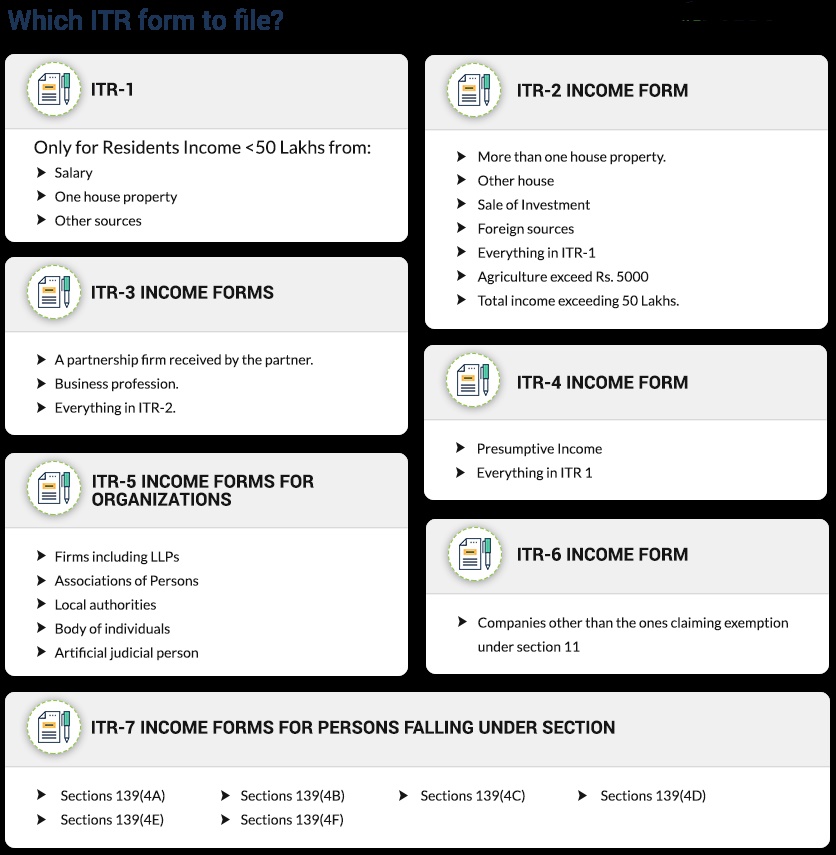

It is to be filed by persons having income from a business or profession. Thus, the eligible source of income for ITR 3 are –

Popular Article :

MCA Changes in Indian Company formation- 2026 A series of reforms measures put forth by the Ministry of Corporate Affairs… Read More

Complete Guide to Reverse Charge Mechanism (RCM) under GST Under Goods and Services, tax is generally paid by the supplier…But… Read More

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

{kind=link}