Page Contents

Tax incidence on an assessee depends on his residential status. For instance, whether an income, accrued to an individual outside India, is taxable in India depends upon the residential status of the individual in India.

Similarly, whether an income earned by a foreign national in India (or outside India) is taxable in India, depends on the residential status of the individual, rather than on his citizenship.

Therefore, the determination of the residential status of a person is very significant.

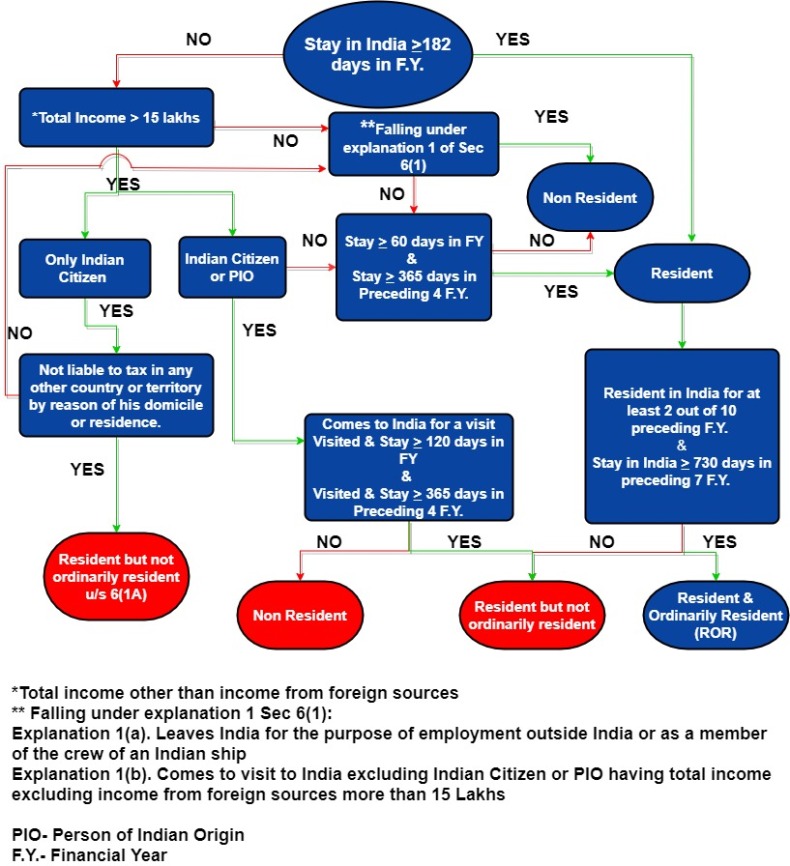

An Individual is said to be a resident Indian for the purpose of Income tax if one of the following Basic conditions are satisfied.

Read our articles:

If one of the above conditions are satisfied then he is resident of india as per income tax. Non-Resident in India if he satisfies none of the basic conditions.

If the Individual fulfils one the following conditions then he said to be resident but not ordinarily resident of India:

Else, he is considered as a resident and ordinarily resident in India.

These conditions need to be tested every year for every Individual.

A Hindu undivided family is said to be a resident in India if the control and management of its affairs is wholly or partly situated in India.

A Hindu undivided family is a non-resident in India if the control and management of its affairs is wholly situated out of India.

In order to determine whether a Hindu Undivided Family is a resident or a non-resident, the residential status of the karta of the family during the previous year is not relevant

An Indian company is always resident in India. A foreign company is resident in India only if during the previous year, control and management of its affairs is situated wholly in India.

Conversely, a foreign company is treated as non-resident if during the previous year, control and management of its affairs is either is wholly or partly situated out of India.

A company can never be ordinarily or not ordinarily resident in India.

Every other person is resident in India if control and management of his affairs is, wholly or partly, situated within India during the relevant previous.

On the other hand, every other person is non-resident in India if control and management of its affairs is wholly situated outside India.

Form 16A (Earlier Reflected in Form 26AS) Now Shows Deductor PAN: A Small Change with a Big Impact on TDS Reconciliation… Read More

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}