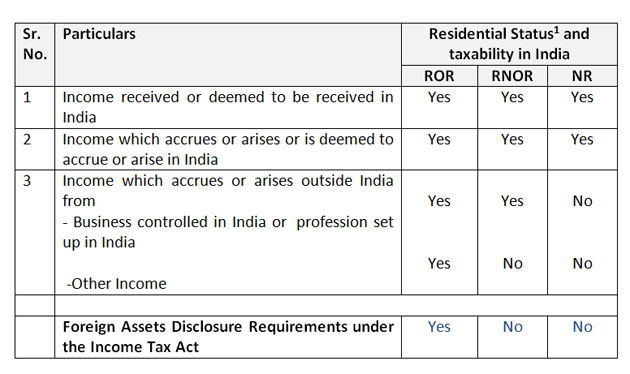

Page Contents

Tax incidence on an assessee depends on his residential status. For instance, whether an income, accrued to an individual outside India, is taxable in India depends upon the residential status of the individual in India.

Similarly, whether an income earned by a foreign national in India (or outside India) is taxable in India, depends on the residential status of the individual, rather than on his citizenship.

Therefore, the determination of the residential status of a person is very significant.

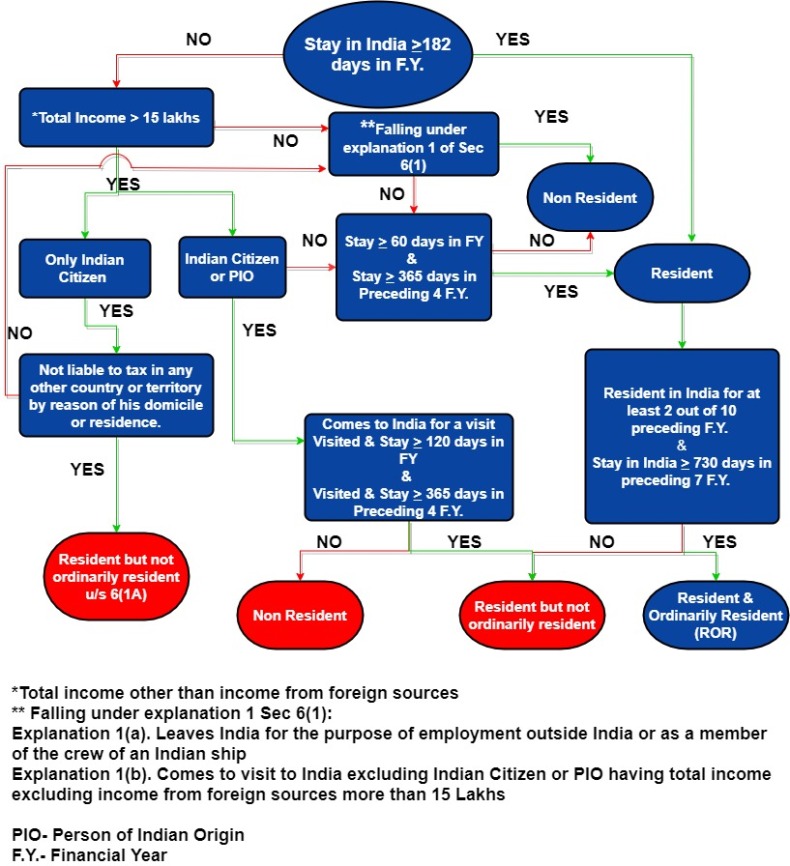

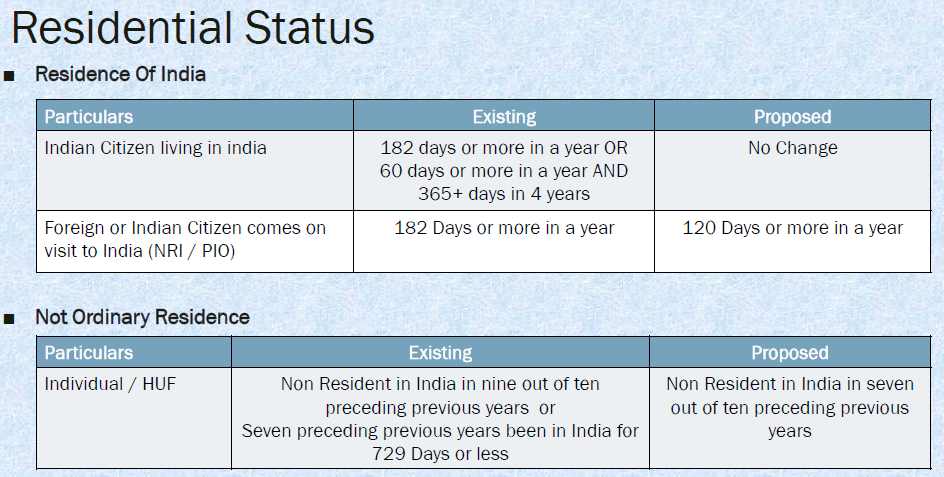

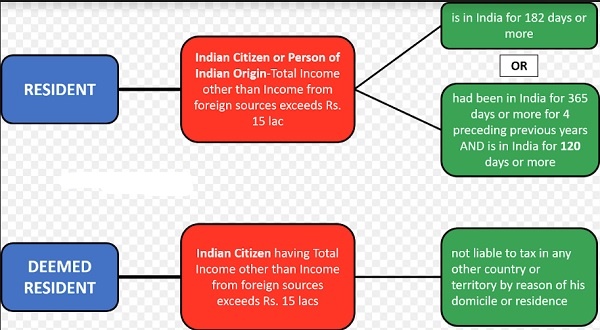

An Individual is said to be a resident Indian for the purpose of Income tax if one of the following Basic conditions are satisfied.

Read our articles:

If one of the above conditions are satisfied then he is resident of india as per income tax. Non-Resident in India if he satisfies none of the basic conditions.

If the Individual fulfils one the following conditions then he said to be resident but not ordinarily resident of India:

Else, he is considered as a resident and ordinarily resident in India.

These conditions need to be tested every year for every Individual.

A Hindu undivided family is said to be a resident in India if the control and management of its affairs is wholly or partly situated in India.

A Hindu undivided family is a non-resident in India if the control and management of its affairs is wholly situated out of India.

In order to determine whether a Hindu Undivided Family is a resident or a non-resident, the residential status of the karta of the family during the previous year is not relevant

An Indian company is always resident in India. A foreign company is resident in India only if during the previous year, control and management of its affairs is situated wholly in India.

Conversely, a foreign company is treated as non-resident if during the previous year, control and management of its affairs is either is wholly or partly situated out of India.

A company can never be ordinarily or not ordinarily resident in India.

Every other person is resident in India if control and management of his affairs is, wholly or partly, situated within India during the relevant previous.

On the other hand, every other person is non-resident in India if control and management of its affairs is wholly situated outside India.

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}