Page Contents

RWA- Association is responsible for supervising the occupants’ everyday problems, arranging events, supervising facilities in the apartments and houses, and also representing the members where necessary on issues related to the place. A housing society is a society that allocates house plots and provides housing facilities and amenities to its members and residents.

According to the central goods and services act, a taxable person is the one who is a supplier of goods and services to another person and is not exempted from the purview of GST. According to GST, a taxable person can be a natural person, HUF, a company or a firm, a limited liability partnership, a local authority, central or statement government, a trust or a society registered under Societies registration act, 1860, a body of individuals or an association of persons (whether incorporated or not within or outside India). Hence, a corporate society is liable to pay GST if registered under the societies act.

Also, as per CGST act 2017, the business includes the provision by a club, society, association or any such body which provides benefits and facilities to its members. Hence, a housing society is liable to pay tax under GST.

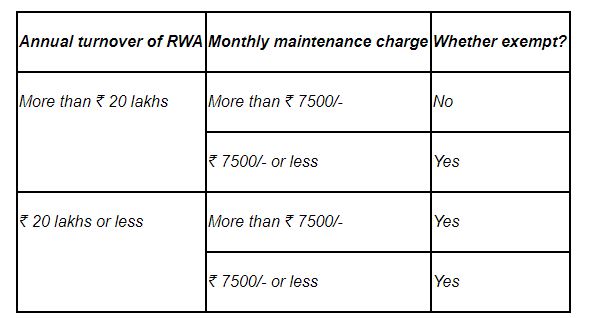

All the housing societies with revenue over 20 lakhs are liable for GST registration. However, if the monthly contribution received from its members does not exceed Rs. 7500, no GST will be charged by the housing society. Moreover, other charges like property tax, electricity charges are exempted from tax under GST and are not included in calculating Rs. 7500.

Also, if the aggregate turnover of the society doesn’t exceed 20 lakh in a financial year even if the monthly charges from each member is more than Rs. 7500, it would be exempted from GST.

25th GST Council Meeting enhances the exemption limit of Rs 5000/- per month per member to Rs 7500/- in respect of services provided by Resident Welfare Association (unincorporated or nonprofit entity) to its members against their individual contribution.

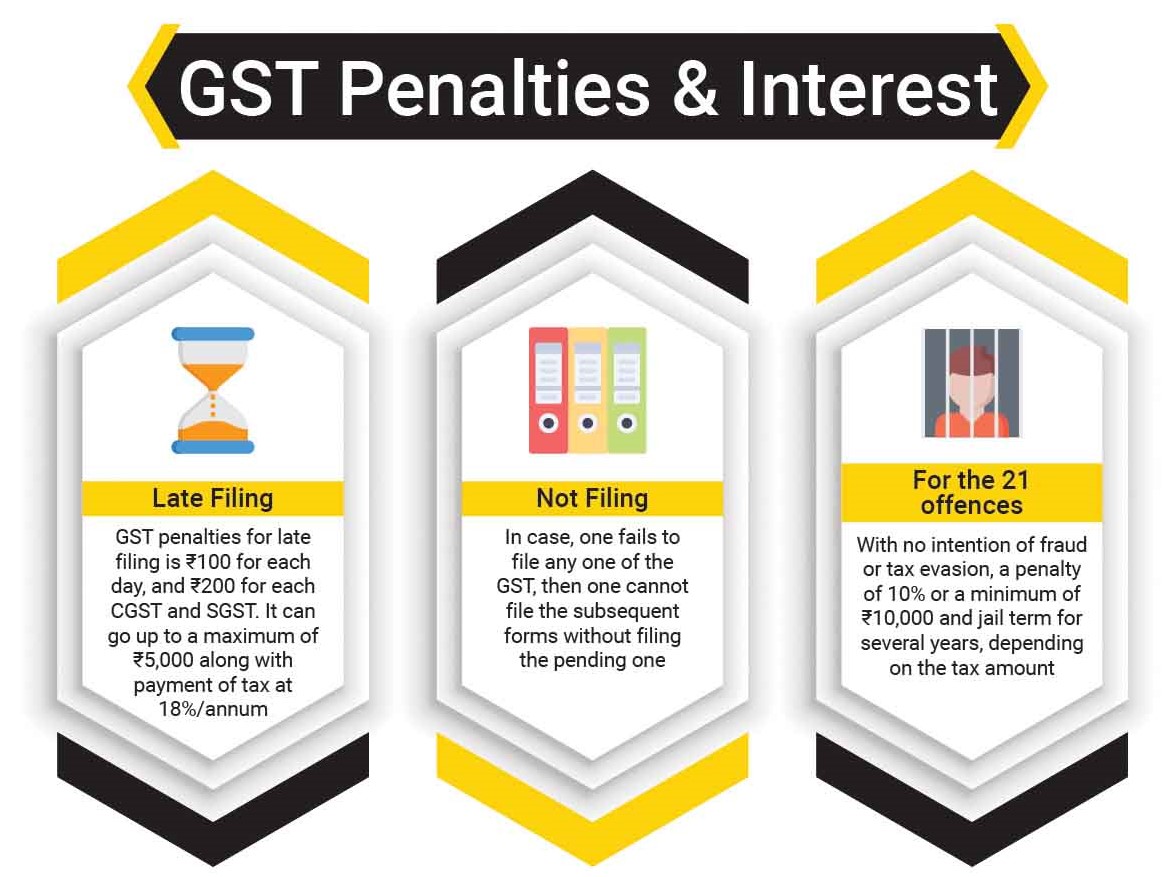

The late fee for delayed filing of GSTR-1 is being reduced to Fifty Rupees per day and shall be Rupees Twenty Five in case of Nil returns.

The following charges are normally collected by the housing society from its members:

Thus, it is clear that a small housing society with a monthly contribution by each member not exceeding Rs 7500 won’t attract GST whereas the societies with a high revenue base or collecting monthly contributions more than Rs. 7500 will come under GST ambit.

Input Tax Credit (ITC) Allowed: If the Society becomes liable to pay GST, it is allowed to take Input Tax Credit under Sec 16 (1) of CGST Act subject to conditions for taking the input tax credit. Housing Society is entitled to ITC in respect of taxes paid by them on capital goods (generators, water pumps, lawn furniture, etc.), goods (taps, pipes, other sanitary/hardware fillings, etc.), and input services such as repair and maintenance services – Lift AMC, Housekeeping, Security, Fire AMC, Repairs & Maintenance, Contract staff, Accounting & Auditing Services, and other such services.

ITC of Central Excise and VAT paid on goods and capital goods were not available in the pre-GST period and these were a cost to the RWA.

Yes, where the fee for such supplies exceeds Rs.7,500 per month per member, most of the ITCs would be available as follows:

As per notification 11/2017 for services related to Services furnished by businesses, employers, and professional organizations Services, Services furnished by trade unions & Services furnished by other membership organizations falling under SAC 9995 the Central Tax Rate is 9%. Similar Provisions are made under SGST Acts also. Therefore there will a levy of 18% (CGST @ 9% + SGST @9%).

Composition Scheme

Housing Society is not eligible for Composition Scheme.

All the Registered Persons (Normal Registration) will have to file 3 returns in a month.

GSTR – 1 by 10th of the following month – Towards Outward Supply (Maintenance Charges)

GSTR – 2 by 15th of the following month –Towards Expenses Side and

GSTR – 3 by 20th of the following month – Monthly consolidated return and

GSTR – 9 by 31st December of the Following Year.

GSTR-3B return will have to be filed by all taxpayers in addition to GSTR-1, GSTR-2 and GSTR-3 return. Earlier, GSTR-3B returns were to be filed for the month of July to December 2017.

IN 23rd council meeting, it has been announced that the GSTR-3B return must be filed for all months from July 2017 to March 2018. The due date for the GSTR-3B return will be the 20th of every month.

Read more about: What is core Business Activity GST

Read more about: All about GST Offenses, Penalties, and Appeals

FEE FOR LATE FILLING OF GST RETURN

When a Registered Dealer misses filing GST Returns within DUE DATE late fees is levied by the government.

If GSTR-1 is not filed within due date you will be liable to pay late fees of Rs. 200 per day of delay

Records and Accounts

Maintain proper Records of Supply & Expenses and preserve such records for 72 Months.

At Rajput Jain and associates we assist customers, who file the registration for resident welfare associations incorrectly, according to the rules of procedure.

Rajput Jain and Associates is a professional tech online and legal service that helps customers streamline RWA registration procedures, implementation, taxes and any other business-related legal compliance and service in India.

Get a free consultation service with our top-qualified experts for registration.

GST – RWA’s heave a sigh of relief – Only contributions in excess of Rs.7500/- would be taxable – CBIC e-flyer of 2017 took correct view – AAR ruling and 2019 Circular quashed: HC

Most Important GST-Related Supreme Court Judgments for Practice The five most impactful Supreme Court cases are discussed in detail. These… Read More

All About the Code on Social Security, 2020: Employer Compliance Guide 2026 What is the meaning of "Code on Social… Read More

Employment Information Return (Form XXVI) under the Code on Social Security, 2020 The Employment Exchanges (Compulsory Notification of Vacancies) Act,… Read More

GSTN: E-Way Bill Enhancements (Ship-To GSTIN) hold next notice GSTN advisory is significant because it would have introduced new mandatory… Read More

Taxation of F&O trading as non-speculative business: F&O trading is treated as non-speculative business income u/s 43(5) and is taxable… Read More

Avoid artificial tax-saving tricks ("jugaads") while filing ITR Don't Claim Section 10(14)(i) Allowances Just to Save Tax Recently, several social… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}