Page Contents

“Relative”, in relation to an individual, means the husband, wife, brother or sister or any lineal ascendant or descendant of that individual ;

As per the Income-tax act, the term “relatives” is described in detail. As gift received in the form of cash, cheque, or good from your relative is fully exempt from tax. So if you receive gift money from any of your relatives listed below, you are not liable to pay any tax on the same.

Gift received from a relative is not taxable in hands of recipients under section 56 of Income Tax Act.

The persons who are considered as relatives are

In the case of individual

| Sr no. | Relative | Covered under |

| 1. | Husband/wife | Clause(i) |

| 2. | Brother and his wife | Clause(ii)with(vii) |

| 3. | Sister and her husband | Clause(ii)with(vii) |

| 4. | Wife’s bro. and his wife | Clause(iii)with(vii) |

| 5. | Wife’s sister and her husband | Clause(iii)with(vii) |

| 6. | Kaka – Kaki | Clause(iv)with(vii) |

| 7. | Fua – Foi | Clause(iv)with(vii) |

| 8. | Mama – Mami | Clause(iv)with(vii) |

| 9. | Masa – Masi | Clause(iv)with(vii) |

| 10. | Father – Mother | Clause(v)with(vii) |

| 11. | Grandfather – Grandmother | Clause(v)with(vii) |

| 12. | Son and his wife | Clause(v)with(vii) |

| 13. | Daughter and her Husband | Clause(v)with(vii) |

| 14. | Father in Law and Mother in Law | Clause(vi)with(vii) |

| 15. | Grand Father in Law (GFIL) and Grand Mother in Law (GMIL) | Clause(vi)with(vii) |

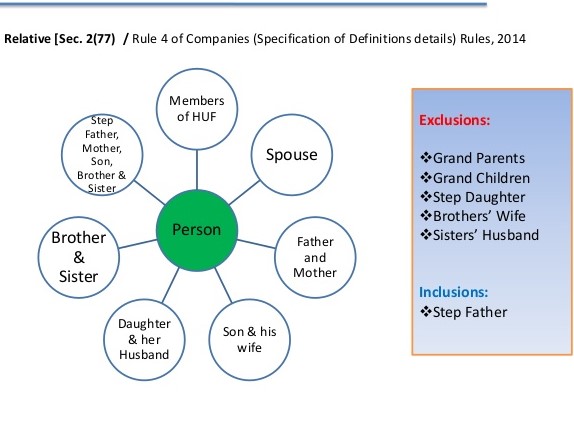

In the case of HUF – Any member of the HUF

A person shall be deemed to be a relative of another if,-

(a) They are members of a Hindu undivided family; or

(b)They are husband and wife; or

c) The one is related to the other in the manner indicated below

| Sr.no | Company`s act 2013 |

| 1 | Father(including stepfather) |

| 2 | Mother(including stepmother) |

| 3 | Son(including step-son) |

| 4 | Son`s wife |

| 5 | Daughter |

| 6 | Daughter`s husband |

| 7 | Brother(including step-brother) |

| 8 | Sister(including step sisters) |

| Relationship | Sec-2(41) of the income tax act | Sec-56(2) –gift | Sec-2(77) –foreign exchange management act |

| Spouse

| Yes | Yes | Yes |

| Parents( father/mother) | Yes | Yes | Yes |

| Brother /sisters | Yes | Yes | Yes |

| Son/daughter | Yes | Yes | Yes |

| Spouse of brother/sister | No | Yes | No |

| Spouse of son/daughter | No | Yes | Yes |

| Parent`s brother/sisters and their spouse | No | Yes | No

|

| Spouse`s brother /sister and their spouse | No | Yes | No |

| Grand-Parents and Grand Children | Yes | Yes | No |

| Spouse of Grand- Children | No | Yes | No |

| Great-Grand-Parents and Great-Grand- Children | Yes | Yes | No |

| Spouse’s Parents, Grand-Parents and Great-Grand- Parents | No | Yes | no |

The comparison graph of the definition of a relative under the acts referred to above is as follows:

| S. No. | Relative | GST Act | IBC Act | Companies Act | Accounting Standard | Income Tax Act | ||

| 2(77) | AS -18 | Ind AS -24 | 2(41) | 56(2)(vii) | ||||

| 1 | Grandson | Not Covered | Covered (Lineal Descendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 2 | Grand Daughter | Not Covered | Covered (Lineal Descendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 3 | Grand Father | Not Covered | Covered (Lineal Ascendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 4 | Grand Mother | Not Covered | Covered (Lineal Ascendant) | Not Covered | Not Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 5 | Father | Covered (If dependent) | Covered (Lineal Ascendant) | Covered | Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 6 | Step Father | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 7 | Mother | Covered (If dependent) | Covered (Lineal Ascendant) | Covered | Covered | Not Covered | Covered (Lineal Ascendant) | Covered (Lineal Ascendant) |

| 8 | Son | Covered | Covered (Lineal Descendant) | Covered | Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 9 | Daughter | Covered | Covered (Lineal Descendant) | Covered | Covered | Not Covered | Covered (Lineal Descendant) | Covered (Lineal Descendant) |

| 10 | Step Son | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 11 | Brother | Covered (If dependent) | Covered | Covered | Covered | Not Covered | Covered | Covered |

| 12 | Step Daughter | Not Covered | Not Covered | Not Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 13 | Step Mother | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 14 | Step Sister | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 15 | Son’s Wife | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 16 | Sister | Covered (If dependent) | Covered | Covered | Covered | Not Covered | Covered | Covered |

| 17 | Step Brother | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 18 | Husband/ Wife/ Spouse | Covered | Covered | Covered | Covered | Covered | Covered | Covered |

| 19 | Daughter’s Husband | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 21 | Member of a HUF | Not Covered | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered |

| 22 | Spouse’s Brother/Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 23 | Liner Ascendant/ Descendant of Spouse (Including their Spouse) | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 24 | Spouse of Liner Descendant | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 25 | Spouse of Liner Ascendant | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 26 | Spouse of Brother/ Sister of the Individual | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 27 | Spouse of Spouse’s Brother/ Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 28 | Spouse of parent’s Brother Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 29 | Parent’s Brother Sister | Not Covered | Covered | Not Covered | Not Covered | Not Covered | Not Covered | Covered |

| 30 | Dependent of Individual/ Spouse | Not Covered | Not Covered | Not Covered | Not Covered | Covered | Not Covered | Not Covered |

Related Persons as specified in GST law Regulatory Framework

Popular Blogs

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

HRA Exemption under Old Tax Regime: New Rules Effective from 1 April 2026 Salaried Employees & HRA: New Rules Effective… Read More

{kind=link}

{kind=link}

{kind=link}