Page Contents

Two members are the minimum requirement to form an LLP, whereas no limitations are put when it comes to the maximum number of partners who can participate.

There are certain people like individuals, limited liability partnerships, companies, Foreign Limited Liability Partnerships, and foreign companies who can participate.

Limited Liability for Partners: This accounts to be one of the most important drawbacks. This is why most people are scared to participate in it. On the other hand in the LLP it is seen the partners to be responsible or liable for their contribution to the firm, They are not awarded individually.

Perpetual Existence: There stands to be a perpetual existence of the partners. The existence of the partner is not at all dependent on other partners. There occurs a change in the partners who participate in the LLP. Therefore the conversion of the partnership is essential which helps to maintain individualism.

Unlimited partners: This is another major cause of conversion. The minimum number is always fixed the participation can exceed any level.

Better credit access: Easier bank loans are provided to the partners. They are given their assets are credits equally and they get their awards for their contribution. They also have a much efficient system of management which is essential in the Limited Liability Partnership. Therefore is always preferred.

Potential Growth: The amalgamation and merger of the business greatly help to unlock many business strategies. The LLP, in turn, can also easily merge with other LLP which helps in a notable amount of growth in the business profits.

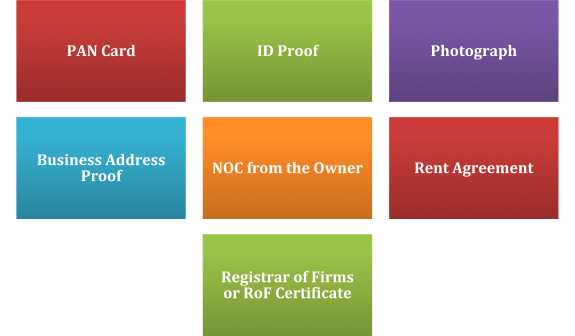

The below Accompanied by provided following attachments along with form 17

Accompanied by the provided following are:

Both forms must be e-signed by the proposed appointed partners and accredited by the ICWA, the CS or the CA or either of them must be in full-time practice. The fee to be paid varies with respect to the value of the capital contribution.

This form-14 has to be attached accompanied by:

– scan copy of the Limited Liability Partnership Incorporation Certificate.

– scan copy of the formation documents submitted in Form FiLLiP.

Each partner would be collectively and severally responsible for all the liabilities and obligations of the company that were incurred prior to such conversion. If a partner dissolves the duty, it shall be paid by the Limited Liability Partnership.

The Limited Liability Partnership must provide that period of 12 months starting on a date not later than 14 days after registration:

– a declaration that it has been converted from a corporation to a Limited Liability Partnership as of the date of registration listed and

– Name and registration number(s) of the corporation from which it has been converted in each official communication of the Limited Liability Partnership.

In the event that the Limited Liability Partnership contravenes the above clause, it shall be disciplined with a minimum fine of Rs 10,000 and a maximum fine of Rs 1,000,000. In the event of continuous default, the minimum fine shall be Rs 50 per day and the maximum amount shall be Rs 500 per day.

Now use CA Rajput’s Expert & Legal Services to register Your LLP or Conversation your LLP. Our experts can handle your LLP compliance and Company/ LLP while you are doing what you do best! Contract us for more details

Popular Articles :

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}