Page Contents

At its 42nd meeting held on 05.10.2020, the GST Council suggested that a registered person with a gross turnover of up to five (5) crore would be authorized to make a return on a quarterly basis, along with monthly tax payment, effective from 01.01.2021.

Effective Date – The scheme will be introduced with effect from 01 January 2021.

In the event that the total turnover exceeds 5 crore ropes in any quarter of the current financial year the registered person shall not be liable for the scheme in the next quarter.

Migration

Ans: Yes, a registered person can move back to the option of submitting a monthly return when he has opted for the QRMP scheme.

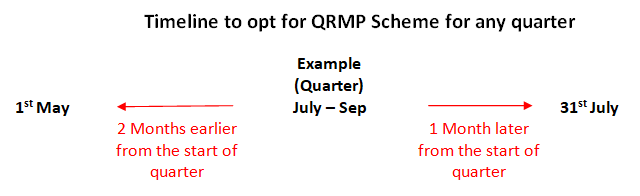

The provision to opt-out of the scheme for a quarter will be accessible from the first day of the second month of the previous quarter to the last day of the first month of the quarter.

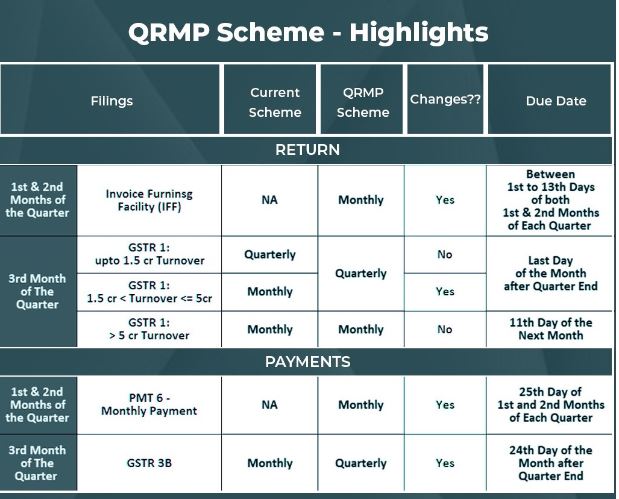

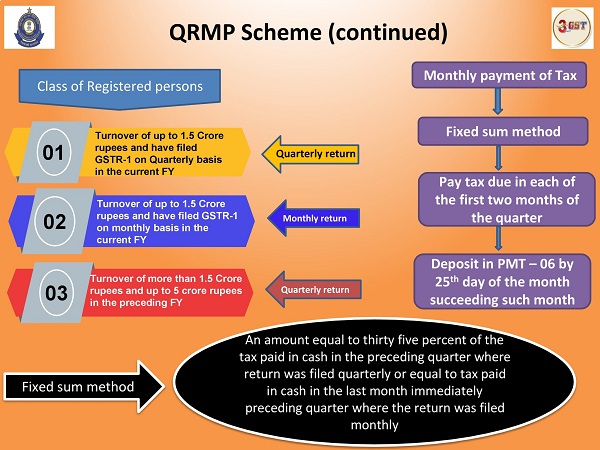

| Sr. No. | Kind of Registered persons | Monthly Tax payment | Class of Returns |

| 1. | Sales of up to INR 1.5 Crore and have filed GSTR-1 on a QTRly basis in the Present Financial Year | Fixed sum method | Quarterly return |

| 2. | Sales of more than INR 1.5 Crore and up to INR Five crore in the last Financial Year | Deposit in PMT — 06 by 25th day of the month next such month | Quarterly return |

| 3. | Sales of up to INR 1.5 Crore and have filed GSTR-1 on monthly basis in the Present Financial Year | Pay tax due in each of the first two months of the quarter | Monthly return |

Notes: Clarification in respect of applicability of Dynamic Quick Response (QR) Code on B2C invoices and compliance of notification 14/2020- Central Tax dated 21st March 2020- Clarification on applicability on QR Code Notification 14/2020

Ans: The registered person under the QRMP scheme will be allowed to pay the tax due to each of the first two months of the quarter by depositing the due sum in FORM GST PMT-06 on the twenty-fifth day of the month following that month.

When generating the villain, taxpayers should choose “Monthly payment for quarterly taxpayers” as the explanation for generating the villain. Process for calculating the monthly payment of the tax the taxpayer is eligible to use one of the following 2 choices given below for the monthly payment of the tax in the first two months:

| 1. Fixed sum method | 2 Self-assessment System |

| · A taxpayer who’s already made a quarterly return in the preceding quarter may decide to pay 35 percent of the tax paid in cash in the previous quarter. · An share of thirty-five percent of the tax paid in cash in the previous quarter where the return was filed quarterly or equal to the tax paid in cash in the last month preceding the quarter where the return was submitted monthly. · The facility will be made accessible on the portal to generate a before the callan in the form of GST PMT-06. · Non-availability of monthly tax payment facility: monthly tax payment by this form will not be applicable to registered persons who did not provide the return for the entire tax immediately prior that month. The full tax period shall be the tax period in which the person is registered on the first day of the tax period to the last day of the taxable period. | · The registered individual may pay the tax due by taking into account the tax liability for inward and outward supplies and the tax credit available. · In order to enable the determination of the available ITC for a month, a self-produced input tax credit estimate has been made accessible for each month in FORM GSTR-2B.

|

Ans: Applicability of late fees

Ans: The option to make use of the QRMP Scheme is GSTIN wise and therefore separate persons as specified in Section 25 of the CGST Act (different GSTINs on the same PAN) have the option to make use of the QRMP Scheme for one or more GTINs.

In other words, some GSTINs for that PAN may opt for the QRMP Scheme and the remaining GSTINs may not opt for the Scheme.

A new scheme for quarterly returns with monthly payments [QRMP] will be implemented as from 1 January 2021 on the recommendation of the GST Council.

Under this scheme, taxpayers whose Aggregate Annual Turnover (AATO) is up to Rs. 5 Cr in the past financial year and current financial year will have the option of filing their return/statement-FORM GSTR-1 and FORM GSTR-3B on a quarterly basis with a clear payment call for the first two months of the year.

The requirements and advantages of this scheme are set out in the attached document. Link – A new scheme for quarterly returns with monthly payments [QRMP]

As per the details available to us, your AATO is up to Rs. 5 Cr in the previous financial year. In order to encourage a seamless transition to the new system, you have defaulted to a monthly frequency under the new scheme.

If your AATO has not reached Rs. 5 Cr in the current year and you would like to opt-in for a new scheme, you can do so by logging in to the GST Portal and navigating to Services > Returns > Opt-in for quarterly returns.

Ans: Invoice Furnishing Facility (IFF) is a service offered to quarterly taxpayers to submit their outward supply information within first 2 months of the quarter (M1 and M2). This facility will be equivalent to FORM GSTR-1, but will enable only the below tables to be submitted:

Ans: No, Invoice Furnishing Facility is an optional facility for quarterly taxpayers only.

Ans: No, the possibility of Invoice Furnishing Facility uploading information will end after the 13th of the month. Any remaining invoices may be filed using the Invoice Furnishing Facility of the following month or in the quarterly form GSTR-1.

Ans: Yes, all invoices submitted by you via Invoice Furnishing Facility will be submitted in the form GSTR-2A and GSTR-2B of the recipient.

Ans: No, there’ll be no late fee for late filing of IFF, as the taxpayer will not be permitted to file IFF after the completion date.

Ans: The pre-requisites for IFF filing are:

Ans: The review is generated automatically by the GST Portal at a duration of <30 minutes>. If you want to see the description instantly, after adding invoices, you can also generate the description by clicking the GENERATE IFF SUMMARY button.

Even so, the summary can only be generated at a time interval of 10 minutes. If you try to generate an overview earlier than 10 minutes, you will notice an error message at the top of the page.

Ans: Yes, you can review the PREVIEW Invoice Furnishing Facility button available at the bottom of the GSTR-1/ Invoice Furnishing Facility page to view the details that you entered in the Invoice Furnishing Facility form.

Ans: You can display the filed IFF forms under the ‘View Filed Returns’ and ‘Track Return Status’ options.

Ans: You can submit the details by clicking the SUBMIT box at the bottom of the GSTR-1/IFF page.

Ans: The submit button will freeze invoices uploaded to the GSTR-1/IFF for that particular month. You will not be able to submit any additional invoices for that month. If you have missed adding any invoices, you can upload those invoices over the next month.

Ans: No, the filing of the IFF file / GSTR-1 form is similar to the filing of any other return form.

Ans: You can use either Submit with DSC or File with Electronic verification code options to file the IFF file / GSTR-1 form.

Ans: Small taxpayers who file their GSTR-1 returns on a quarterly basis may use the Invoice Furnishing Facility.

It is important to remember that if a taxpayer does not choose to upload invoice details through the IFF, he/she must upload all invoice details to the GSTR-1 return for the 3 months of the quarter.

Ans: The details mentioned are to be provided by small taxpayers if they opt for the Invoice Furnishing Facility:

Ans: Since the Invoice Furnishings Facility is optional for quarterly GSTR-1 filers, the GST platform may provide an opt-in timeframe for the same.

Once the small taxpayers opt for it, the GST portal would provide these quarterly filers with this facility for the first 2 months of the quarter. Invoices should be submitted to IFF from the 1st to the 13th of the following month.

So for now, the IFF format has still not been notified and we can anticipate notification of the format and way in which the invoice data will be uploaded soon. There has also been no clarification as to whether or not an offline tool will be given.

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

Can an Employer Introduce New Rules After Standing Orders Come Into Force? Many employers believe that once an organization grows,… Read More

Madras High Court on GST Fraud Notices under Section 74 – Key Takeaways The Madras High Court, in Fastenex Private… Read More

ITR Filing AY 2026-27: Eligibility, Documents Required, Due Dates & Penalties for Non-Filing Who Must File ITR for Assessment Year… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}