Page Contents

There is some person in a business who does not do the business regularly and they have done not any fixed place of business.

The GST act provisions and rules are different from them are different from the normal taxpayers under GST. Even their registration process is also different.

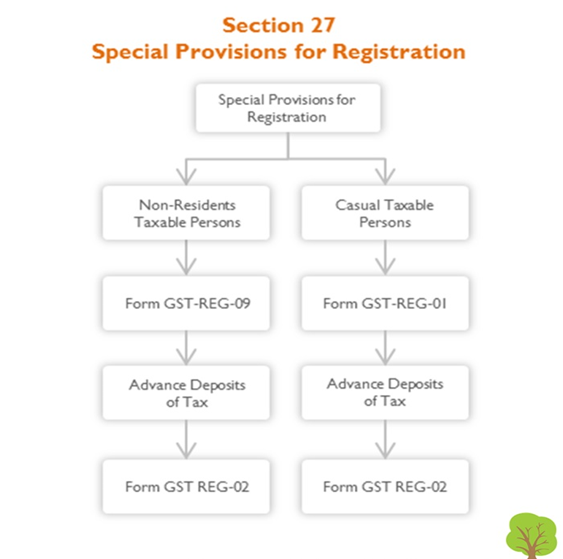

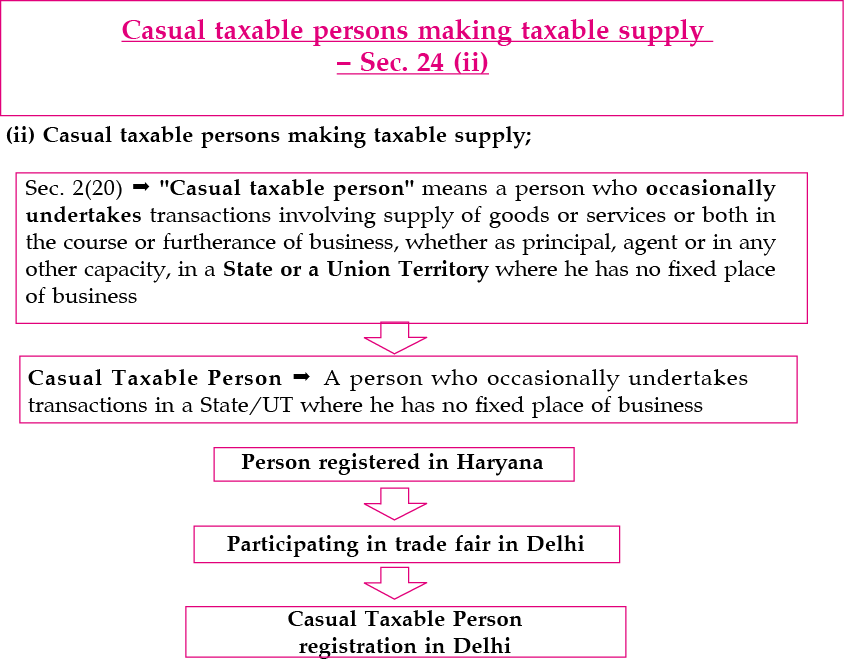

A casual taxable person is the one who occasionally undertakes the transaction. They make the transaction from the place where they have no fixed place of business. They can act as a principal or agent as well.

Some persons who is not resident of India and they do not have any place of business in India. But they occasionally undertake transactions temporarily.

They also get registration temporarily like the casual taxable person. The GST act provisions and rules are different from them are different from the normal taxpayers under GST. These are called non-resident taxable persons.

presently only FORM GSTR-1 and FORM GSTR-3B is filled.

FAQ ON GOODS AND SERVICES TAX

Query: is any threshold limit apply to casual taxable persons and non-resident taxable persons for registration?

Answer: No, there is no threshold limit apply to a casual taxable person and non-resident taxable person for registration.

Query: -composition scheme applies to the casual taxable person and non-resident taxable person?

Answer: No, the composition scheme applies to casual taxable persons and non-resident taxable persons.

Query:– can a casual taxable person and a non-resident taxable person take registration can take registration after the commencement of business?

Answer: No, casual taxable person and non-resident taxable person need registration before the commencement of business.

Query: Please clarify what is the taxable event under GST?

Answer: The taxable event under GST shall be the supply of goods and/or services made for consideration in the course or furtherance of business. The taxable events under the existing indirect tax laws such as manufacture, sale, or provision of services shall stand subsumed in the taxable event known as ‘supply’.

Query: One of my clients is already registered under Vat law and Service Tax law. Whether he has to obtain fresh registration under GST law?

Answer: No. GSTN shall migrate all such assessees or dealers to the GSTN network and shall issue GSTIN number and password. They will be asked to submit all requisite documents and information required for registration in a prescribed period of time. Failure to do so will result in the cancellation of the GSTIN number. The service tax assessees having centralized registration will have to apply afresh in the respective states wherever they have their businesses.

Read our articles:

Query: If the appellate or revisional order goes in favor of the assessee, whether a refund will be made

in GST? What will happen if the decision goes against the assessee?

Answer: The refund shall be made in accordance with the provisions of the earlier law only. In case any recovery is to be made then it will be made as an arrear of tax under GST.

Query: Whether any person, who is not liable to pay GST or not liable to get registered himself, can voluntarily get himself registered?

Answer: Yes. The person can get himself registered voluntarily even though he is not liable to be registered and all provisions of this Act, as are applicable to a registered taxable person, shall apply to such person.

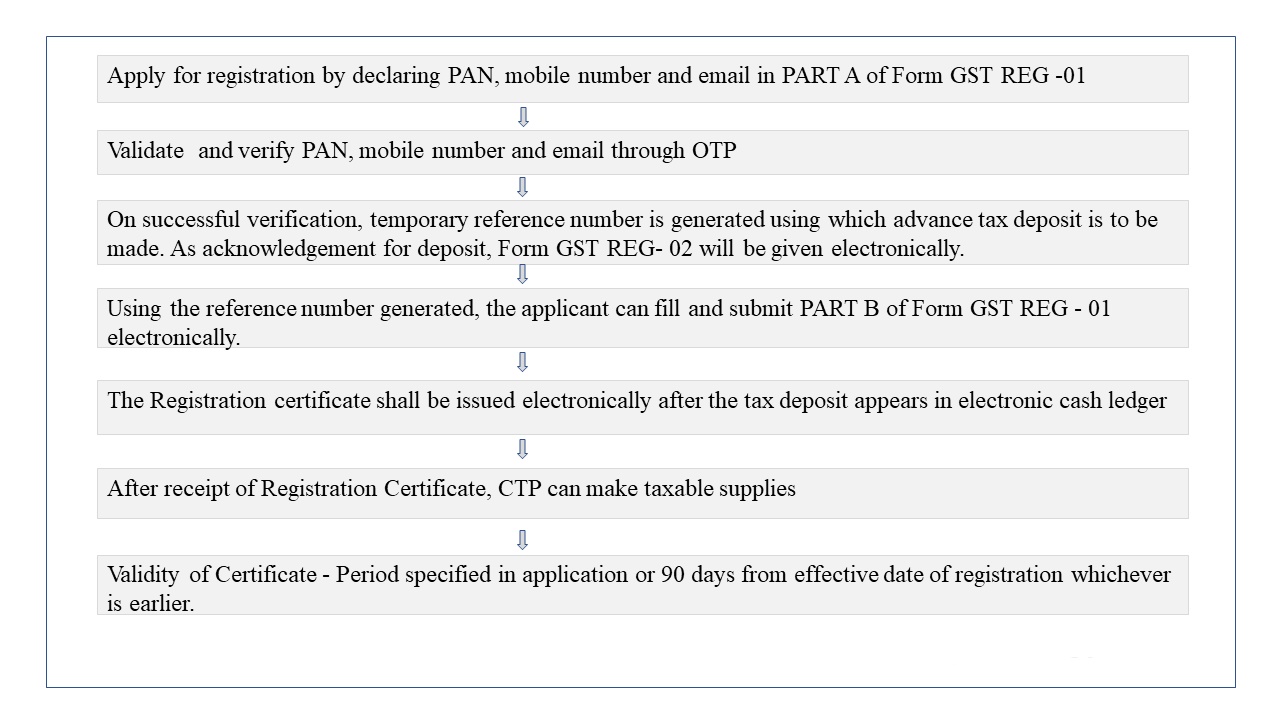

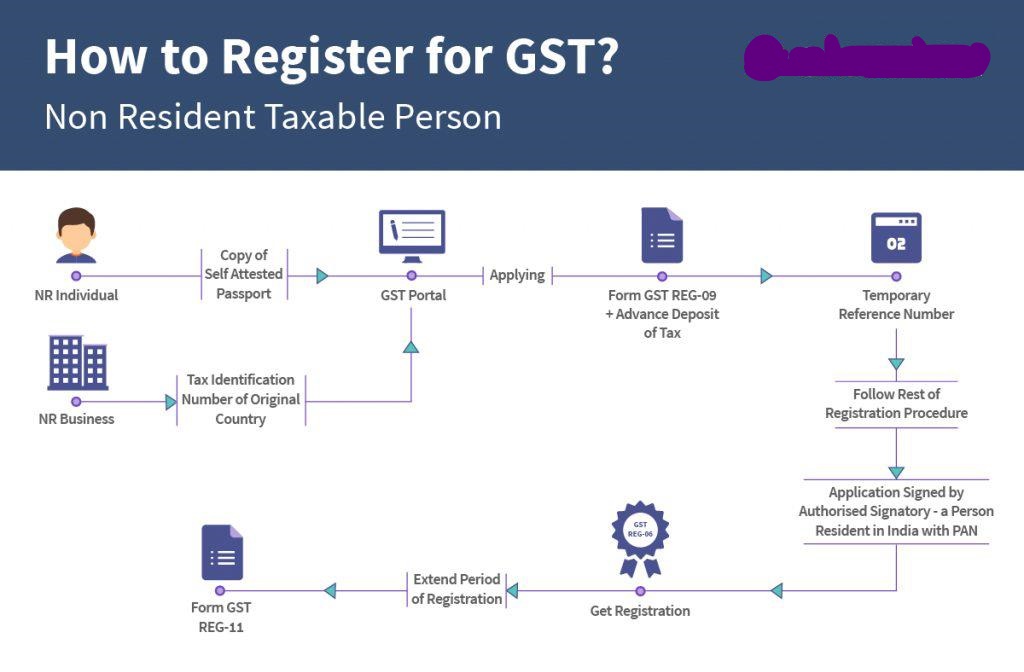

Query: Please explain the procedure for registration of a non-resident taxable person?

Answer: Every Non-resident taxable person is required to submit an E-application for registration in Form –GST REG 10 at least 5 days prior to commencement of the business. Such person shall be given a temporary identification number by the Common Portal for making an advance deposit of tax under section 19A and the acknowledgment in Form GST REG-2 in shall be issued thereafter.

Query: If a person, who has taken voluntary registration, can seek cancellation of his registration?

Answer: Any person who has taken voluntary registration can also seek cancellation of his registration but not before one year of such registration. There should be a gap period of 1 year from effective registration in case of voluntary registration.

Query: Whether a person is eligible for an input tax credit on inputs from the date when he applies for registration or from the date when registration is granted. Please clarify.

Answer: The person is eligible for an input tax credit on inputs held in stock and inputs contained in semi-finished or finished goods held in stock from the date when registration is granted.

Query: what are included as “Place of Business” under GST ?

Answer: Place of Business includes the following places:-

(a) Place of ordinary business

(b) Warehouse, Godown & other places for storage goods or place to provide services

(c) Place of Maintenance of Books of accounts

(d) Place of any agent conducting the business

Query: Sir if a person is operating in two different states, with the same PAN, Can he obtain a single Registration under GST?

Answer: No, every person who is liable to take a Registration will have to get registered separately for each of the States where he has a business operation and is liable to pay GST.

Query: Is there any provision for a taxable person to pay tax on a provisional basis under GST law?

Answer: Yes, a taxable person can make payment on a provisional basis but only after the permission of the Proper Officer & only in such cases where he is unable to determine:

Query: Whether an agreement to supply goods at future date can be considered as a contract of supply for the purpose of GST? How will hire purchase transactions to be treated?

Answer: The definition of ‘supply’ in Model GST law includes all forms of supply of goods made or agreed to be made for consideration. Thus, an agreement of supply at a future date will constitute an agreement of supply of goods.

Query: Can a taxpayer use a digital signature in the GSTN registration?

Answer: Taxpayers have the option to sign the submitted application using valid digital signatures (if the applicant is required to obtain DSC under any other prevalent law then he will have to submit his registration application using the same). For those who do not have a digital signature, alternative mechanisms will be provided in the GST Rules on Registration.

Query: A person has one place of business in Delhi with a turnover of Rs. 13 lakhs and other places of business in Manipur with a turnover of Rs 4 lakhs. What would be the threshold limit in this case for registration?

Answer: In this case, the person’s aggregate turnover in the state of Delhi will be Rs. 17 lakhs (i.e. Rs 13 + Rs 4 lakhs) which is less than the threshold limit of Rs 18 lakhs. Thus he is not liable for registration in Delhi. But he is liable for registration in Manipur as the aggregate turnover exceeds the threshold limit of Rs 9 lakhs.

Query: What is the difference between Annual returns & Final returns?

Answer: Yes, an Annual Return has to be filed by every taxable person who is registered and paying tax as per the normal or compounding scheme. Final Return has to be filed only by those registered taxable persons who have applied for cancellation of registration. This has to be filed within three months of the date of cancellation or the date of cancellation order.

We look forward to your valuable comment www.carajput.com

FOR FURTHER QUERIES CONTACT US:

W: www.carajput.com E: singh@carajput.com

T: 9-555-555-480

Summary of the Proposed Amendments to the IBBI Liquidation Regulations (2026) The document proposes major changes to India's liquidation… Read More

India has consistently maintained that the power to enact laws rests exclusively with its Parliament, acting within the framework of… Read More

Alternative (lower) tax regimes are available to assessees other than individuals/HUFs under the Income Tax Act. What does it mean?… Read More

ITR Filing Assessment Year 2026-27: Due Dates, New ITR Changes, Revised Return Rules & Compliance Guide The due dates for… Read More

Tax Audit at a Glance: Important Points for Futures & Options Traders Income Tax Treatment of Futures & Options Traders… Read More

Common Misconception of Crypto taxation in India Crypto Futures Contracts A crypto futures contract is a legal agreement between two… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}