Overview on GST applicability on E-commerce Sale

- E-commerce (electronic commerce) is the buying and selling of goods and services, or the transmitting of funds or data, over an electronic network, internet or online social networks. The purchasing and sale of goods and services over the internet is e-commerce. E-commerce may be a replacement for brick-and-mortar stores, but some companies prefer to retain both. Almost all can be obtained today via e-commerce.

For all the E-commerce transaction there must be the following three parties involved :

- ECO i.e. E-commerce Operator

- Buyer

- Sel7ler

Types of E-commerce

Business-to-Business (B2B):

- This type of e-commerce involves all kinds of electronic transactions between two business entities that take place. The exchange may be either services or products. Companies using services from other companies and manufacturers selling their goods to wholesalers are the most popular business models that are B2B.

- A B2B business form needs more investment in capital. They negotiate with fewer clients extensively to customize their goods and services according to their clients’ requests. Of course, pricing practices are competitive. Each consumer, however, receives personal care about their specific requirements, and thus, if the standard is preserved, further renewals and returns can be expected.

Business-to-Consumer (B2C) :

- One of the most basic methods of E-Commerce is the B2C E-Commerce model. It implies a contractual partnership between a corporation and its clients, as the name suggests. Most of these firms, therefore, are commercial in nature. Some of them may be suppliers of services.

- Each year, this type of company generates more and more revenue by selling products of almost all kinds, including groceries, crafts, hardware, software, fashion-related products, and many more. This also suggests, however, that this market is highly competitive. It offers a lot of data and choices to clients.

Consumer-to-Consumer (C2C) :

- C2C business communicates electronically, usually via a third party, between two customers. In return for offering a forum where the seller can present their goods and a buyer can recruit their interest or requirements, the third-party receives a percentage or fixed commission. As long as all parties comply with the rules and regulations laid down, the third party typically does not engage in the dealing process.

Consumer-to-Business (C2B):

- Basically, C2B companies include freelancers and individuals who sell owned products to companies (who can buy and sell them or retain them) but have not set up a company for themselves, can sell their work through this form of business operation. Needless to mention, electronically, all the transactions occur.

Business-to-administration (B2A):

- It’s includes all transactions between businesses and public administration performed online. This is a field that includes a wide range of services, particularly in areas such as finance, social security, jobs, legal documents and registers, etc. With investments made in e-government, these types of services have grown significantly in recent years.

Consumer-to-administration(C2A):

- E-commerce includes all electronic transactions between citizens and the government. The C2A e-commerce model enables the user to post their questions and directly request information from their local governments/authorities about the public sector. This offers a simple way to create contact between customers and the state Taxes (filing tax returns), wellness (scheduling an appointment using an online service), and paying higher education tuition are examples of C2A.

Finally, the Types of transaction under E-commerce is classified :

- Between Seller & ECO – Provision of the market place

- Between Seller & Buyer – Sale of Goods ;

Goods and Services Tax shall be levied on both of the above transactions:

MEANING OF E-COMMERCE IN GST

- The Chapter defines an ‘electronic commerce operator’ to mean a person who owns, operates, or manages an electronic platform engaged in facilitating the supply of any goods/services or in providing any information or any other incidental services.

E-commerce operator

- Electronic commerce operator: shall include every person who, directly or indirectly, owns, operates or manages an electronic platform that is engaged in facilitating the supply of any goods and/or services or in providing any information or any other services incidental to or in connection therewith but shall not include persons engaged in the supply of such goods and/or services on their own behalf.

The implementation of these requirements has forced the online salters to adopt the GST regime. Some of the following compliances are:

GST Registration requirement

FOR E-COMMERCE OPERATOR

- Registration under GST is mandatory for all e-commerce operators irrespective of the sales turnover. Hence, prior to commencing business as an e-commerce operator or within 30 days of commencing business, all e-commerce such as .flipkart, Amazon or Snapdeal must obtain GST registration

FOR SELLER

- Persons undertaking a supply through e-commerce operators are also required to obtain GST registration irrespective of sales turnover.

- As par notification 65/2017 dated 15-11-2017 the Central Government, on the recommendations of the Council, hereby specifies the persons making supplies of services, other than supplies specified under subsection (5) of section 9 of the said Act through an electronic commerce operator who is required to collect tax at source under section 52 of the said Act, and having an aggregate turnover, to be computed on all India basis, not exceeding an amount of twenty lakh rupees in a financial year, as the category of persons exempted from obtaining registration under the said Act.

No GST registration limit:

- The Government has set a limit for all business owners. An organization is liable to register for goods and services tax once this limit has been breached. Registration of the GST applicable under the GST. If the taxpayer crosses the threshold. However, in the case of E-Commerce sellers*, such a limit does not apply.

- Many of the important aspects that need to be clearly understood are:

- Get your GST registration done as quickly as possible.

- Plan your supply chain management and storage requirements carefully.

- Implement such platforms, technologies that will allow your business to be GST compliant.

What are specified services u/s 9(5) of the Central Goods & Services Tax Act, 2017?

| Sr No | Nature of Service | Supplier of Service | Who is liable to pay Goods and Services Tax |

| 1 | Services by way of housekeeping, such as plumbing, carpentering, etc | Any person except who is liable for registration under section 22(1) of the Central Goods And Services Tax Act, 2017 | E-commerce operator |

| 2 | Transportation of passengers by motorcar, a radio-taxi, maxicab and motorcycle | Any Person | E-commerce operator |

| 3 | Providing accommodation in hotels, guest houses, inns, clubs, campsites or other commercial places meant for residential or lodging purposes | Any person except who is liable for registration under section 22(1) of the Central Goods And Services Tax Act, 2017 | E-commerce operator |

Summary table below shall be helpful to understand the Provision:-

| Description of Supply | Person liable to pay GST | Threshold Limit exemption applicability | Registration mandatory (Yes/No) |

| Passenger Transportation Services Supply | E-Commerce Operator-RCM Applicable | Not required | Not required |

| House Keeping Services Supply | E-commerce Operator- RCM Applicable. Once Supplier is liable to get registered, Supplier shall be liable to pay GST | YES | Yes (only when turnover Cross INR 20,00,000/-) |

| Supply of Accomodation Services | E-commerce Operator- RCM Applicable. Once Supplier is liable to get registered, Supplier shall be liable to pay GST | YES | Yes (only when turnover exceeds INR 20,00,000/-) |

| Goods Supply | Supplier of Goods-Forward Charge Mechanism Applicable | No | YES |

| Services Supply | Supplier of Services-Forward Charge Mechanism Applicable | Yes | Yes (only when turnover exceeds INR 20,00,000/-) |

APPLICABILITY OF COMPOSITION SCHEME

- No advantages under the Composition Scheme: the majority of these sellers registered with market operators are small businesses.

- The Government has launched a composition scheme in accordance with GST law. This scheme is mainly intended to reduce the burden of compliance on small and medium businesses.

- Under this scheme, firms are required to submit quarterly returns instead of monthly returns and pay taxes at nominal rates of up to 2%. Click here to learn more about the Composition Scheme.

- Fortunately, the GST reform explicitly excluded e-commerce firms from this framework. and GST law has excluded e-commerce businesses from this scheme

TAX COLLECTION AT SOURCE (TCS) MECHANISM ON E-COMMERCE IN GST

- TCS at source by Marketplace Operator: Under the new legislation, marketplace operators are required to subtract a percentage as the seller’s GST liability and to deposit it with the govt. This framework is referred to as “Tax Collection at Source (TCS)” under the GST Act. Ultimately, the marketplace seller will have to file a monthly GST return to claim the TCS credit accumulated by the marketplace operator. This would also have an impact on the liquidity and cash flow of such sellers.

- Since all marketplace operators already have finalized a first-level analysis of the impact of GST on everyone’s operations, marketplace vendors are still completely ignorant of these rules. Tax is collected by the e-commerce operator when a supplier supplies some goods or services through its portal. TCS is calculated and deducted at the rate of 1% of the net value of the goods or services supplied through the e-commerce operator.

TAX COLLECTION AT SOURCE(TCS) DOES NOT APPLY :

- TCS provisions do not apply where GST is payable under reverse charge mechanisms. The provisions of the TCS also do not apply in the case of exempt supplies. TCS is not available when you are selling your own goods through the electronic platform.

The commission charged From the suppliers:

- E-commerce portals charge a commission from different suppliers. It amounts to support services, falling within tariff heading 9985 and attracts GST at a rate of 18%. E-commerce portals are needed to be registered obsessively in accordance with Section 24(ix) of the CGST, 2017, and to pay GST on the amount of the commission collected, without applying for any limit exemption.

- The tax shall be levied on invoices levied against the supplier of goods or services, and such suppliers may make use of the ITC levied on the GST if they are anything else qualified.

RATE APPLICABLE ON E-COMMERCE

- The e-commerce operator must deduct TCS at the rate of 1% from the supplier and remit the same as TCS to the Government. The TCS remitted by the e-commerce operator will be provided as credit to the supplier.

Transactions in which two or more E-COMMERCE are involved.

- In such cases, each transaction needs to be treated separately and examined according to the provisions of Section 52 of the CGST Act, 2017. The TCS will be deducted accordingly

- E-commerce operators are required to file GSTR-8 every month and file a GST annual report. In the monthly GSTR-8 return, e-commerce operators must provide details of outward supplies of goods or services made by sellers through the platform and the amount of TCS collected.

- Details furnished by e-commerce operators will be made available to each of the suppliers in Part C of FORM GSTR-2A

DUE DATE OF GSTR-8

- GSTR-8 return must be filed by E-Commerce Operator on or before the 10th of every month. E-Commerce operators must provide details of outward supplies of goods or services or both made through it

- E-commerce operators are also required to file an Annual TCS Statement by the 31st December of every financial year.

Latest updates

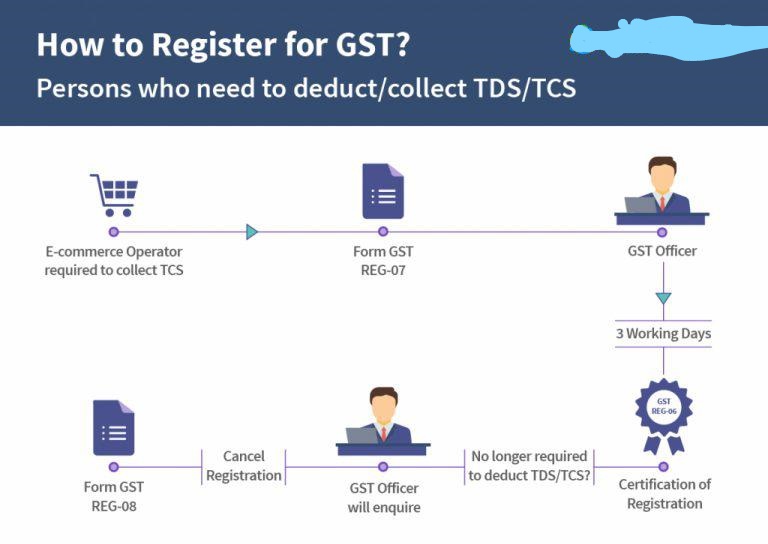

- Any person who is needed to deduct TDS or collect TCS will submit an electronic application for registration, duly signed or verified by EVC (electronic verification code), using the FORM GST REG-07 on the Common Portal; either directly or from the Facilitation Centre notified by the Commissioner.

- After verifying, the proper officer shall issue the registration and issue the registration certificate in FORM GST REG-06 within 3 working days from the date of submission of application.

- Service providers will now be allowed to undertake inter-state sales of up to Rs.20 lakhs without obtaining GST registration. Further, this is exemption is also available for service providers supplying services through an e-commerce operator * e-commerce sellers do not need to register if overall sales are less than Rs. 20 lakh. Notification No. 65/2017 – Central Taxes dated 15.11.2017

- Consequently, persons providing services other than those referred to in Section 9(5) of the CGST Act are really only required to register and collect GST if their turnover exceeds the threshold.

- If your services are listed in Section 9(5) of the CGST Act, the threshold limit shall apply, however, until such time as the E-commerce Operator is responsible for paying, i.e. the requirement of a reverse charge mechanism.

FAQ on e-commerce GST registration in India

Question: Any person wants to sell shoes through Amazon and flipchart. Then is it covered under E-commerce?

Ans : Yes covered under e-commerce

Question: What documents required to get GST Registration?

Ans: Common Documents needed under e-commerce GST registration in India

-

- Photograph of Owner/Authorized Signatories.

- Email ID & Mobile Phone No

- Copy of PAN Card.

- Copy of Proof of Place of Business.

- Proof of Appointment for Authorized Signatories.

- Bank Account Details.

- List of Goods & Services provide e-commerce

- DSC (Digital Signatures).

Question: Is GSTR- 8 Applicable?

Ans: GSTR 8 applicable

- The supplier supplies goods through an e-commerce portal and the e-commerce portal provide services to the supplier. Both transactions are distinct transactions and are subject to GST in their own nature.

- In summary, though it’s not easy to conclude such a wide-ranging issue, GST is, in my view, one of the greatest fiscal reforms our nation has witnessed. It is a unified tax system in a federal country like India.

- While compliance with GST has expanded for the e-commerce industry, still it enhances the market for local suppliers as they can sell at the same tax rate in any state, it will encourage more sellers to go online and to provide the smartest services to people.

- In simplistic words, it can be acknowledged that the State would be possible to produce revenue from this sector, but there are some practical consequences, but then as a whole introduction of Gst on e-commerce is favorable.

- Even though we are at a very early stage in the introduction of gst. But marketplace sellers may not have a lot more time luxury and it is recommended to be proactive in your business practices on the transformation to GST.

- At just the final moment of the round, I have to say that this write-up will help in understanding the GST on e-commerce and the GST roll-out may lead to higher compliance for e-commerce players but, along with it all, it would provide transparency and boost income for the Country.

Permission of Booking Post Offices & Foreign Post Offices that correspond with them in accordance with Postal Export (Electronic Declaration & Processing) Regulations, 2022

Specific suggestions should be sought for your special situation.

This blog is written by Swatantra Kumar Singh & can be reached at singh@carajput.com or at Linked linkedin.com/in/swatantra-singh-84849519

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}