Page Contents

HSN CODE IS REQUIRED ON ALL B2B INVOICES FOR EVERY TAXPAYER.

HSN codes to be declared under the GST in present circumstances

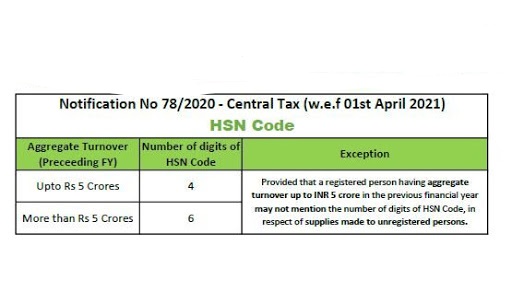

Note: A registered person with a cumulative turnover of up to 5 crores rupees in the past financial year is not required to include the number of digits of the HSN Code in a tax invoice issued in respect of supplies made to unregistered persons.

| Turnover/ Sales | Number of digits of HSN to be declared in Return or invoices |

| Up to 1.5 crore | 4 |

| 1.5 crore- 5 crore | 4 |

| More than 5 crore | 6 |

Why is HSN essential for the GST?

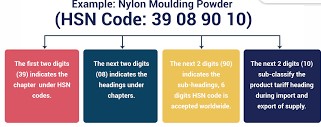

Basis of Rule 1 : Titles of sections, chapters, and sub-chapters are provided for ease of reference only. For legal purposes, refer to headings and sub-headings to drive classification.

Basis of Rule 2a : If the goods are incomplete/unfinished and have the characteristics of the finished product, classification is the same as that of the finished product. The heading shall also include removed/unassembled or disassembled parts.

Basis of Rule 2b : Any reference to a material or substance includes a reference to mixtures or combinations of that material or substance with other materials or substances. The classification of goods consisting of more than one material or substance shall take place as per Rule 3.

Basis of Rule 3a : Choosing a specific heading is preferred over a general heading.

Basis of Rule 3b : Mixtures/composite goods should be classified per the material or substance that gives them their essential character.

Basis of Rule 3c : If two headings are equally suited to the item, choose the heading that appears last in numerical order.

Basis of Rule 4 : If goods cannot be classified per the above rules, they are to be classified according to the goods to which they are most akin.

Basis of Rule 5 : Containers specifically designed for the article and suitable for long-term use will be classified along with that article, if such articles are normally sold along with such cases. For example, a camera case would fall under cameras. Packing materials and containers are also to be classified with the related goods except when the packing is for repetitive use.

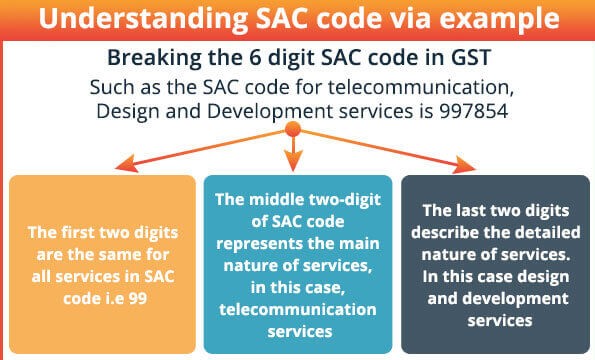

SAC codes Services Accounting Code for services along with the rate of IGST, CGST, SGAT are mention in the below Link

GST does not distinguish between trade and cash discounts. Both are treated based on their timing relative to the supply:

In GST, credit notes for trade discounts or cash discounts are tied to the original invoice, and the SAC (Service Accounting Code) or HSN (Harmonized System of Nomenclature) code used on the credit note must correspond to the one from the original invoice. Here are the key points:

If you’re issuing a credit note for discounts, ensure it directly corresponds to the original invoice for compliance and smooth reconciliation in GST filings.

Understanding Form 16, Form 16A & Form 26AS: A Complete Guide for Taxpayers When filing your Income Tax Return (ITR),… Read More

CFO Cum whole-time director? ROC Gwalior Says No in EKI Energy Services Case Corporate governance is built on the principle… Read More

Toughest Exams in India: More Than a Test of Knowledge, A Test of Character Every year, millions of students and… Read More

Statutory Compliance Calendar August 2026 August 2026 is a crucial compliance month for businesses and professionals in India. In addition… Read More

Overview Taxation of Firms & LLPs in India Key aspects of taxation of partnership firms and limited liability partnerships are… Read More

EPF Scheme 2026: Can Employers Suddenly Restrict PF Contributions to INR 1,800? A question is currently circulating across HR departments,… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}