FOREIGN SUBSIDIARY COMPANY

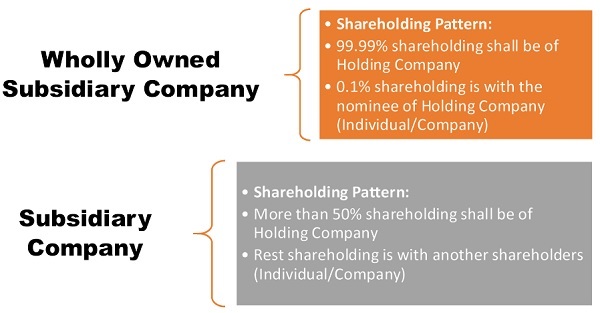

- A foreign subsidiary is any company, where 50% or more of its equity shares are owned by a corporation that’s incorporated in another foreign nation.

- The said foreign company in such a case is termed the company or the parent company.

- For a corporation to be a far-off subsidiary in India, the corporate itself must be incorporated in India. It doesn’t matter which country the parent company is incorporated in.

FOREIGN COMPANY COMPLIANCES

- An India-based subsidiary of any Foreign Company [as defined under section 2(42) of the Indian Companies Act, 2013] may have to perform the subsequent three categories of statutory compliances with Indian regulatory authorities:

- Periodic Compliance

- Annual Compliance

- Event Based Compliance

Additionally, the kinds and nature of those compliances rely on the assorted factors

-

- Type of company and its incorporation,

- Industry type and its market size,

- The number of its employees,

- Annual sales turnover.

- Now, In India, the compliance regime has been made very strict particularly since the promulgation of the new Indian Companies Act of 2013 .

- Every one amendments made thereto within the cases of delayed compliances or failures in statutory compliances advocates for heavy fines, penalties, and punishments including imprisonment.

- Also, the categories and nature of those compliances do depend upon the kind of company and its incorporation, industry type, its market size, the amount of its employees, and its annual sales turnover.

- Now, particularly since promulgation of the businesses Act 2013 and every one amendment made thereto thus far, the compliance regime in India has been made very strict and rigorous, and advocates for heavy fines, penalties, and punishments (including imprisonment) within the cases of delayed compliances or failures in statutory compliances.

- Compliances are supported many aspects of the corporate. One must understand what all compliances are alleged to be met consistent with the sort of company that’s incorporated, the industry of operations, annual turnover, number of employees.

- A remote company is defined under section 2(42) of the businesses Act, 2013, such an organization must follow regulations and rules established under multiple legislations and orders such as:

FOREIGN SUBSIDIARY COMPLIANCES IN INDIA

- All companies established in India must follow the principles and regulations founded by the govt. this can be in effect, no matter whether Indian or Foreign entities or citizens own the businesses.

- The sole difference between the 2 is that foreign-owned subsidiary companies have more rules and regulations to treat compared to Indian owned companies.

- A company where 50% or more of its equity shares are owned by a distant company may be a foreign company. The foreign company in such case is named the company or the parent company.

- Compliances are supported the corporate that’s incorporated. Hence, it’s necessary to grasp what compliances are purported to be met in keeping with the kind of the corporate, the operations of the industry, annual turnover, number of employees, etc.

- Foreign subsidiary companies are mandatorily required to keep up compliance in keeping with the taxation Act, Companies Act, Transfer pricing guidelines, and FEMA guidelines.

- The foreign subsidiary compliance includes taxation filing with the revenue enhancement department, annual return with the ministry of corporate affairs, and other filings with the authorities just like the bank of India or the securities and exchange board of India (SEBI).

- All the businesses even foreign subsidiaries will must befits other Indian tax regulations just like the TDS, GST regulation, PF regulation, ESI regulations, and others.

- The compliance requirement for a remote company would differ supported the industry, state of incorporation, number of employees, and sales turnover.

Foreign Direct Investment of up to 100% is allowed into an Indian private Ltd. and Ltd. for many of the arena.

The number of FDI in India has increased manifold over the previous couple of years thanks to a booming economy and welcoming environment for foreign investors.

Essential Compliances for Foreign Subsidiary Company in India

- The following are the more important compliances that should be met by the foreign subsidiary as per Section 380 and 381 of the businesses Act, 2013.

- In Form FC-1 under Section 380: The FC-1 form is very important because the form has got to be filed within thirty days of the incorporation of the subsidiary in India.

- Shape isn’t to be submitted alone, it must be in the course of the desired files, certifications etc. from other regulatory bodies in India like the RBI.

- In case of Form FC-3 under Section 380: this way must be submitted to the respective Registrar of Companies (ROC) depending upon where the corporate is incorporated in India.

- A shape must contain the small print of the areas where the business goes to conduct operations additionally because the financial records of the corporate.

- Form FC-4 under Section 381: this manner is anxious with the annual returns of the corporate. it’s to be filed within sixty days from the tip of the preceding year.

- Financial statements: the corporate should submit financial statements on its Indian business and operations. This must be submitted within six months of the top of the year.

- They have to contain: – Statements on the transfer of funds – Statements of earnings repatriated – Statements on related party transactions like statements on sales, transfer of property, purchases etc.

- Audit of accounts: All accounts of the foreign subsidiary must be audited by a Practicing comptroller. These accounts should be properly arranged and made available by the corporate for the audit.

- Authentication and translation of documents: All the documents that are submitted by the corporate to the ROC must be validated by a practicing lawyer in India.

- These documents also must be translated into English before its validation and submission.

COMPLIANCES UNDER INCOME TAX ACT AND GST ACT

There are three styles of compliances supported the intermittency of those compliances:

-

Periodic Compliances:

Periodic compliances are compliances that must be met by the corporate on a periodic basis.

Unlike annual compliances, this sort of compliance happens in regular intervals multiple times a year. These compliances may have to be met on a quarterly or a half-yearly basis.

-

Annual Compliances:

Annual compliance to be done by foreign company through out the year. Annual compliances are compliance that must be met once each year.

once a year the corporate has got to meet these compliances mandatorily.

As an example, the corporate needs to do the subsequent every year: – GST filings – TDS filings under the revenue enhancement Act – Compliances under RBI – Compliances under SEBI’s rules and regulations – Annual Financial Statements

-

Event-based Compliances:

As mentioned earlier, there are three sorts of compliances; one among them is event-based. this suggests that these compliances are only mandatory just in case of a specific event or action of the corporate.

There are two event-based compliances under the RBI regulations and FEMA guidelines, they are:

- FC-TRS: This concerns the transfer of foreign subsidiary company’s shares between an Indian resident to a non-resident investor or vice-versa.

-

- Such a transfer could also be done by way of sale or gift. Under the Foreign Direct Investment policies, such a transaction is required to be reported within sixty days from the date of the transfer.

- Duty of filing this kind rests upon the Indian resident, or the investee company because the case could also be.

- This is often irrespective of whether the Indian resident is that the transferer or the transferee.

- The reporting of transfer of shares between Residents and Non-residents and vice- versa is to be made and may be reported within 60 days from the date of receipt/date of payment of the number of considerations.

While filing the above form, the following documents shall be attached –

-

- Relevant regulatory approvals and relevant extracts of the transfer agreement,

- The Transfer Consent letter undertaken between the donor and donee,

- Declaration by Non-resident within the prescribed format

- Consent letter between buyer and seller or just in case of sale/ purchase on the exchange, the contract note should be attached.

- Valuation certificate

- Non-resident declaration

- Where the sale is undertaken by a non-resident, an acknowledgment of FC-GPR/ FC-TRS as required in respect of the capital instruments being sold

- FIRC /Outward remittance certificate and KYC

2. FC-GPR: this is often concerning the remittance received by the shareholders of an overseas company

-

- The shape specifies the mode of transfer of the remittance by the corporate to its shareholders. FC-GPR-In FC-GPR, the foreign inward remittance concerning the difficulty of share capital to the foreign investor is reported.

- Shape specifies the assorted mode of payment for the consideration received from investor through banking channel, NRE / FCNR, Escrow A/c, Swap, etc.

- The banking channels are generally used for such transactions. While filing the shape FC-GPR, following documents are required to be attached:

- KYC of foreign investor

- Company Secretary Certificate

- Declaration by the authorized representative of the Indian company as per FEMA.

- Valuation certificate from SEBI registered Merchant Banker / accountant /Cost accountant or the other person as authorized under FEMA 20(R)

- Foreign Inward Remittance Certificate

- Other documents as applicable on case-to-case basis.

IMPORTANCE OF OTHER COMPANY & OTHER INCOME TAX COMPLIANCES

Company Act:

- It is mandatory for an overseas subsidiary to satisfy all compliances as there is severe consequences if they fail to try too so.

- Failure to fulfill required compliances may end in the corporate being fined, being levied penalties and might also cause criminal charges with imprisonment under relevant provisions of applicable law(s).

- The subsequent are the penalties that will be levied against an organization for not meeting their compliances:

-

- Notwithstanding anything given under Section 391, if a distant company is found to own contravened any provisions under Chapter XXII of the Act, the corporate is punished by way of fine that shall be no but Rs 1 lakh and should extend up to Rs 3 lakh.

- If the offence is continuous, then a fine of Rs 50,000 are going to be added for each day, the offence continues.

- Every officer of a distant company who is in default is punishable by imprisonment for a period of up to six months and/or a fine of minimum Rs 25,000, which can reach up to Rs 5 lakh.

- It’s important for an organization to satisfy all its compliances to make sure that they’re ready to continue with its business operations properly without the interference of the authorities.

Income Tax Act:

Each person engaging in an international transaction or a defined domestic transaction is required by the Income Tax Act to acquire a report from a chartered accountant in the prescribed form and submit it to the Income Tax Department.

Failure to deliver a report from a chartered accountant in the manner specified above carries a penalty of Rs. 1,000,000.

-

PENALTY FOR FAILING TO FURNISH CA REPORT

A chartered accountant’s report is essential for entities engaging in foreign transactions.

A penalty of Rs. 1,00,000 might be imposed if a chartered accountant’s report is not submitted.

-

NOT MAINTAINING DOCUMENTS PENALTY

As previously stated, entities engaging in foreign transactions must maintain the documentation indicated above. Where non-compliance exists, failure to keep such documents up to date, as well as failure to disclose or furnish disinformation, can result in a penalty of up to 2% of the transaction value.

-

PENALTY FOR NOT PRODUCING DOCUMENTS

Any individual who has engaged in overseas transactions may be required to provide any associated information or document by tax authorities during the course of any case.

Failure to provide any important information will result in a penalty of up to 2% of the transaction value for each such failure.

For query or help, contact: singh@carajput.com or call at 9555555480

Popular Articles :

{kind=link}

{kind=link}