Indirect tax Updates: Recent Updates in GTS law Compliance

In the middle of a covid crisis, several agencies expect GDP to fall in most major economies. India could be one of the slowest growing economies in Q2 of 2020-21. India’s growth in Q1 was the steepest among the G-20 countries.

- The economy has begun to open up on GST collections, post-lock-down due to Covid, and so tax collections are also on an increase.

- GST collections began to rise from July 2020 and were in the range of Rs. 87000 to 105000 crores. In October 2020, GST collected crossed Rs. 1 lakh crore and was Rs. 105155 crores.

- While the GST collections in November 2020 may also show + 1 lakh crore due to the festive season.

- Recently, the Chairman of the 15th Finance Commission claimed that GST is not a perfect tax structure in India due to a path-breaking reform and needs improvements along with rationalisation of rates.

- He has also proposed eliminating exemptions and enhancing the standard of technology and matching invoices.

More read : Reasons for the Movement of Goods under the GST

The effective date of changes in section 39 of CGST Act, 2017

- The Central Government has appointed the 10th day of November 2020, as the date from which adjustments in the provisions of section 39 (1, 2, and 7) made by Finance Act, 2019 of Act shall come into force. These changes relate to the furnishing of returns under the QRMP Scheme.

Following Changes have been made in CGST Rules, 2017 in relation to returns (Rule 59, 60, 61, 61A and 62)

GSTR-1 related

- Quarterly return filers can file their 1st and 2nd month B2B invoices in Invoice Furnishing Facility on or before 13th of 1st month in next quarter

- Total value for such B2B invoices is capped to 50 lakhs pm

- No need to report invoices again in GSTR-1 if already reported in IFF

- The deadline of GSTR-1 for quarterly submission is 13th of 1st month in next upcoming Quarter

- HSN/SAC codes shall be mandatorily in GSTR-1 ( <5Cr- 4 digit, >5Cr- 6 digit)

GSTR-2 related

The invoices reported in IFF shall be made available to recipient in their GSTR-2A/2B as follows:

| Details | FORM | Part of FORM GSTR 2A |

| Non-resident taxable person | GSTR-5 | Part A |

| Input Service Distributor | GSTR-6 | Part B |

| Tax deducted at source | GSTR-7 | Part C |

| The tax collected at the source | GSTR-8 | Part C |

| Integrated tax paid on the import of products or goods brought in domestic Tariff Area from Special Economic Zone unit or a Special Economic Zone developer on a bill of entry | | Part D |

GSTR-3B related

- Rule 61(6) was introduced to provide a deadline for filing GSTR-3B for the months of October 2020 to March 2021 as 20th of next month if TO > 5 Crores

- Quarterly return filers shall deposit tax in electronic cash ledger for 1st and 2nd months on or before 25th of next month.

Extension of deadline for GSTR-1

The new deadline for filing form GSTR-1 has been notified w.e.f. 01st January 2021

| Monthly / Quarterly | Due Date |

| Monthly | 11th of the succeeding month. |

| Quarterly | 13th of the succeeding month. |

Class of persons for QRMP Scheme

- A registered individual whose aggregate turnover exceeds five crore rupees for a quarter of the financial year shall not be eligible for a quarterly return as of the first month of the succeeding quarter.

- Taxpayers who have furnished returns for the October 2020 tax year on or before 30 November 2020 shall be considered to have opted for the monthly or quarterly tax cycle in compliance with sub-rule (1) of Rule 61A of those regulations, as follows:

√ Turnover <= 1.5 crore and GSTR-1 on Qtly basis in CFY- Qtly

√ Turnover <= 1.5 crore and GSTR-1 on Monthly basis in CFY- Monthly

√ Turnover >1.5 crore rupees and up to 5 crore rupees in the preceding financial year- Monthly

During the period from the 5th day of December 2020 to the 31st day of January 2021, a registered individual can change the default option electronically on a common portal.

This has been effective since 01.01.2021.

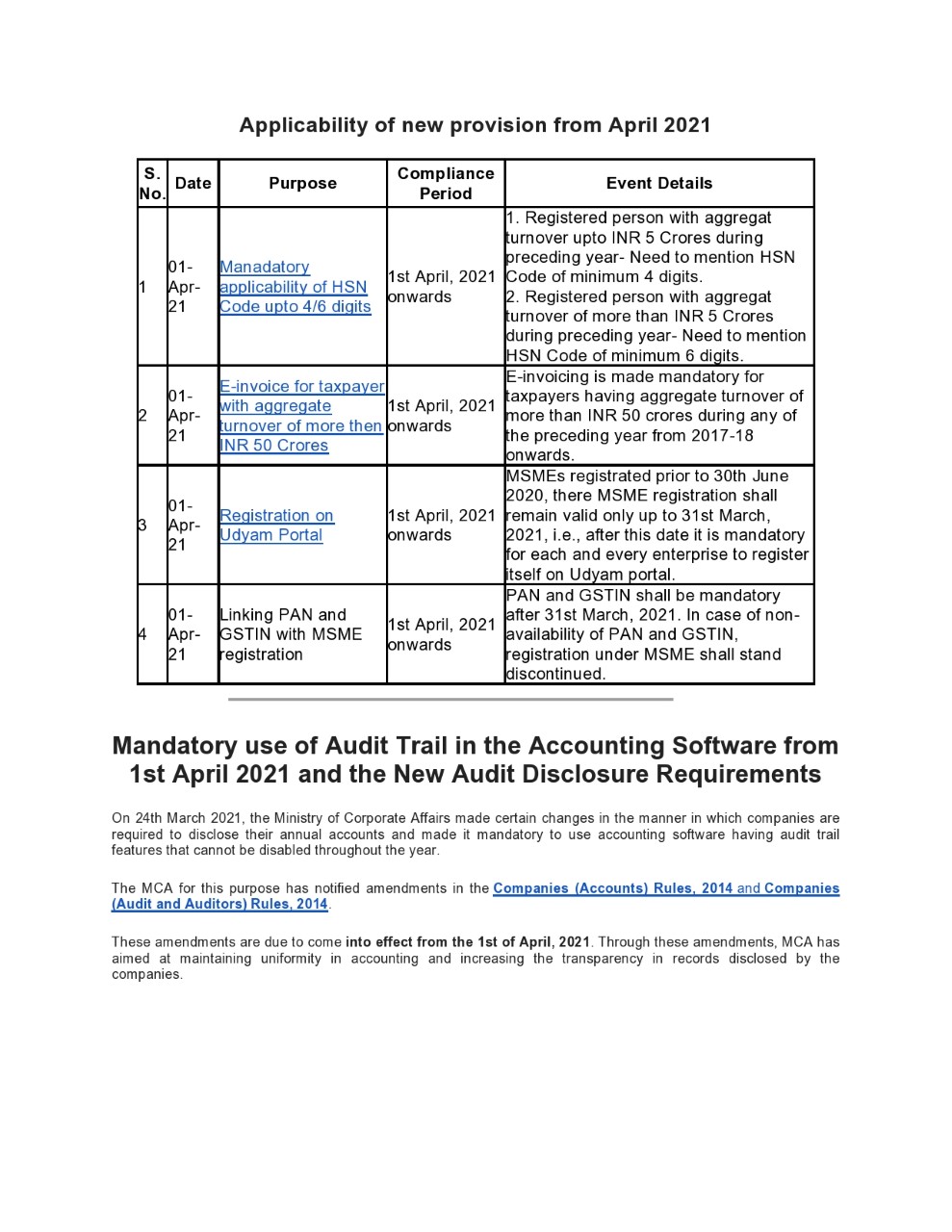

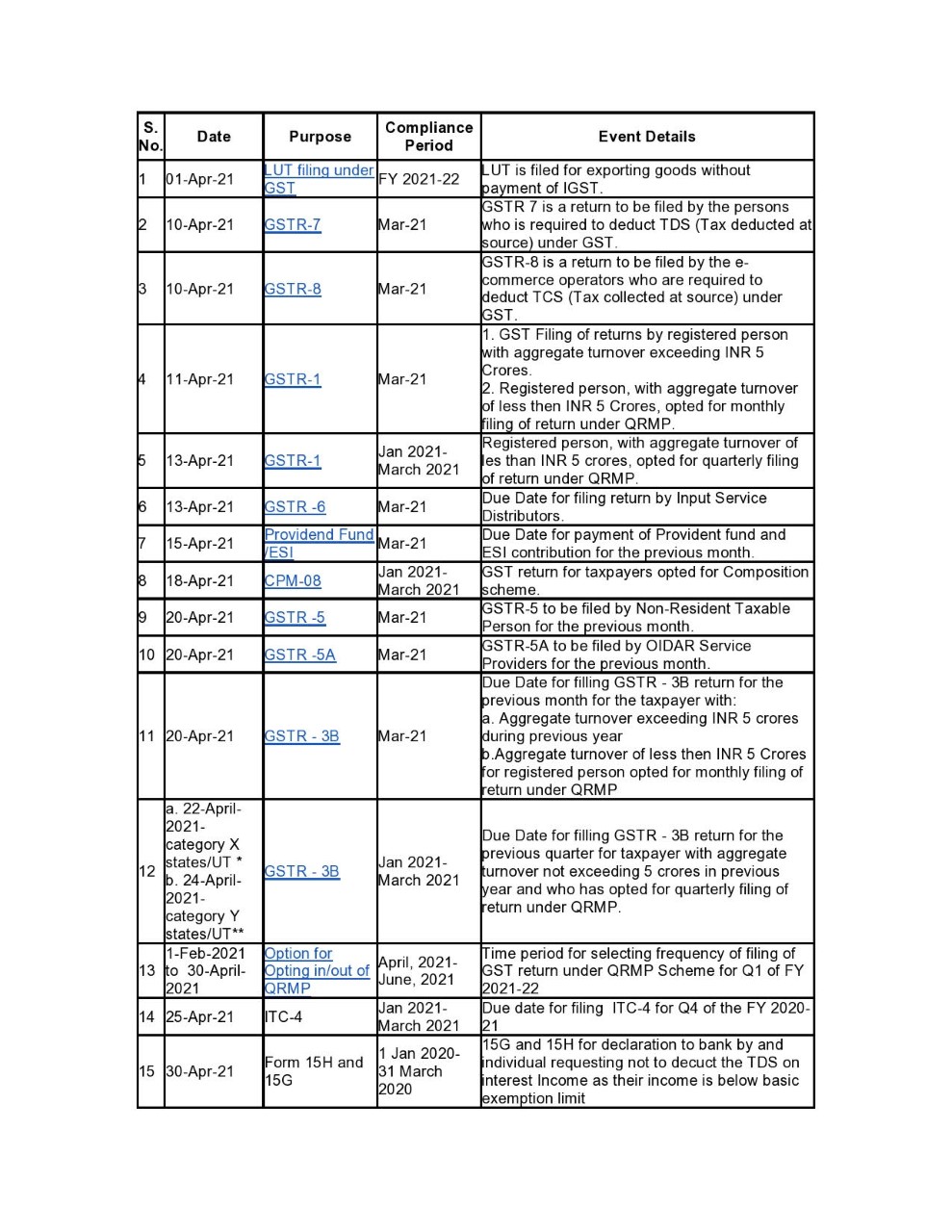

Compliance Calendar April 2021

Other Update :

- A taxpayer can file an appeal against an order passed by an appellate authority or against an advanced ruling by an appellate authority on the GST portal. He even has the option to file an application with the appellate authority in the case of rectification of a mistake in order passed.

- For affordable housing GST rate reduced from 8% to 1% & for other housing from 12% to 5%.

- Definition of affordable housing: 90 sq. Meter for non-metro & 60 sq. meter. For metro area. Cap on Cost of house to be qualified as affordable kept at Rs 45 Lakh for both non-metro and metro areas.

- A GST registration number can be obtained without the same. New businesses who are in the process of obtaining bank accounts can simultaneously proceed with GST registration, thus saving time.

- Claiming of ITC and amendment of B2B invoices of 17-18 are re-opened up till March 2019.

- Users can now amend B2B invoices of FY 2017-18. The facility to amend the GSTR-1 details of FY 17-18 was closed on filing the September 2018 return. The same has been made available while filing returns for the months of January to March 2019. Input tax credit of FY 2017-18 that was omitted and hence unclaimed up till September 2018 can be claimed now up to March 2019 as well.

- This was a much-needed remedy for taxpayers who made errors reporting any invoice in the past, or previously missed out claiming genuine credit.

- For composition taxpayers, there is a simpler way to reply to show cause notices(SCN) now. This is in the case of a show-cause notice being issued for compulsory withdrawal from the composition scheme, and if proceedings are initiated against the composition taxpayer, he now has the option to reply to show cause notices on the portal.

E-way Bill Updates:

- E-way bill data can be imported for GSTR-1.

- The E-way bill (EWB) and the GST portal has now been integrated. The same gets automatically imported for the B2B and B2C (large) invoices sections as well as the HSN-wise-summary of outward supplies section. Users only need to verify the data and proceed.

GST Updates on 11.02.2021

- Today is the date of filing of GSTR-1 for the month of January-2021 (Turnover exceeding Rs. 1.5 cr or opted to file a monthly return).

- CBDT issues the Procedures Instructions to be supported during the Search Operation.

- E-Way Bill is compulsory where the value of each Invoice is individually lower than 50k but, totally exceeds 50k, says Kerala High Court.

- Directorate General of GST Intelligence- Gurugram arrests a man for fraudulently using the ITC of Rs 376 cr via Seven Fake Firms.

- GST @ 18 % Rate applicable to the manufacture of tanks: UP AAR.

- Institute of Chartered Accountants of India wants FM to withdraw the Budget proposal to do aside with the GST audit: Source Business Standard.

- We have made clear that thousands of crores of rupees collected in tax (GST) actually occurred because of the chartered accountants… it was not self-reporting, but also because the CA carried out the audit and told the company to pay the tax in Form 9,” said Atul Kumar Gupta, President, Institute of Chartered Accountants of India.

- The budget provision in clause 101 of the Finance Bill 2021 seeks to omit section 35(5) of the CGST Act in order to remove the legal requirement for annual audited accounts & the reconciliation statement submitted by given professionals.

- Whereas the rule is intended to improve the doing business, the Institute of Chartered Accountants of India stated in a letter to the Ministry of Finance and the Office of the Prime Minister that it would make early detection complicated.

Read our articles:

Rajput Jain & AssociatesRajput Jain & Associates is a Chartered Accountants firm, with it's headquarter situated at New Delhi (the capital of India). The firm has been set up by a group of young, enthusiastic, highly skilled and motivated professionals who have taken experience from top consulting firms and are extensively experienced in their chosen fields has providing a wide array of Accounting, Auditing, Taxation, Assurance and Business advisory services to various clients and their stakeholders.

Rajput jain & Associates, a professional firm, offers its clients a full range of services, To serve better and to bring bucket of services under one roof, the firm has merged with it various Chartered Accountancy firms pioneer in diversified fields.

We have associates all over India in big cities. All our offices are well equipped with latest technological support with updated reference materials. We have a large team of professionals other than our Core Team members to meet the requirements of our prospective clients including the existing ones. However, considering our commitment towards high quality services to our clients, our team keeps on growing with more and more associates having strong professional background with good exposure in the related areas of responsibility.

{kind=link}

{kind=link}