Page Contents

Input Tax Credit refers to the amount of tax, which a taxpayer pays on

the inputs purchased, for providing outward taxable supplies.

Such an amount of ITC can be used to set off as against the outward tax liability, thereby reducing the outward tax to be paid in relation to taxable supplies.

Such a credit for input tax is the essence of GST. ITC helps in eliminating the cascading effect and thus reduces the events of tax on tax.

When you person buys any good/service from a registered dealer, they need to pay certain amount of taxes on the same.

Now, when the said purchased, goods are further sold, the person collect tax from their customer.

Now, while depositing the amount of tax collected from the customer, the supplier can set off the amount of tax paid at the time of purchase and make the payment of the balance amount of tax.

Since a single tax in the name of GST is levied all across India, the suppliers do not face any problem in claiming the ITC and there would be a seamless flow of credit, throughout the chain of supply.

Any person, registered under GST, can claim the amount of ITC, provided all the following conditions are fulfilled –

More read: GST Return compliances calendar- Nov 2020

It is provided that ITC can be claimed only where the goods or services availed have been made for making further taxable supplies, in the course or furtherance of business.

Thus, ITC shall not be available in respect of supply of goods/services made for personal use, Exempt supplies, and supplies in respect of which ITC is specifically disallowed.

In the pre-GST era, there were different indirect taxes, all over India, and the rates were also different in every state/UT. Thus, the availability of ITC was very difficult, and because of this, there was a cascading effect.

However, after the introduction of GST, all the taxes were subsumed under one tax named GST, and the rates were uniformly charged all over India.

GST involves the following class of taxes –

CGST is levied in respect of intra-state/UT supply of goods or services or both.

2. State Goods and Services Tax (SGST)

SGST is levied in respect of intra-state supply of goods or services or both.

3. Union Territory Goods and Services Tax (UTGST)

UTGST is levied in respect of intra Union Territory supply of goods or services or both.

4. Integrated Goods & Services Tax (IGST)

IGST is levied in respect of inter-state supply of goods or services or both.

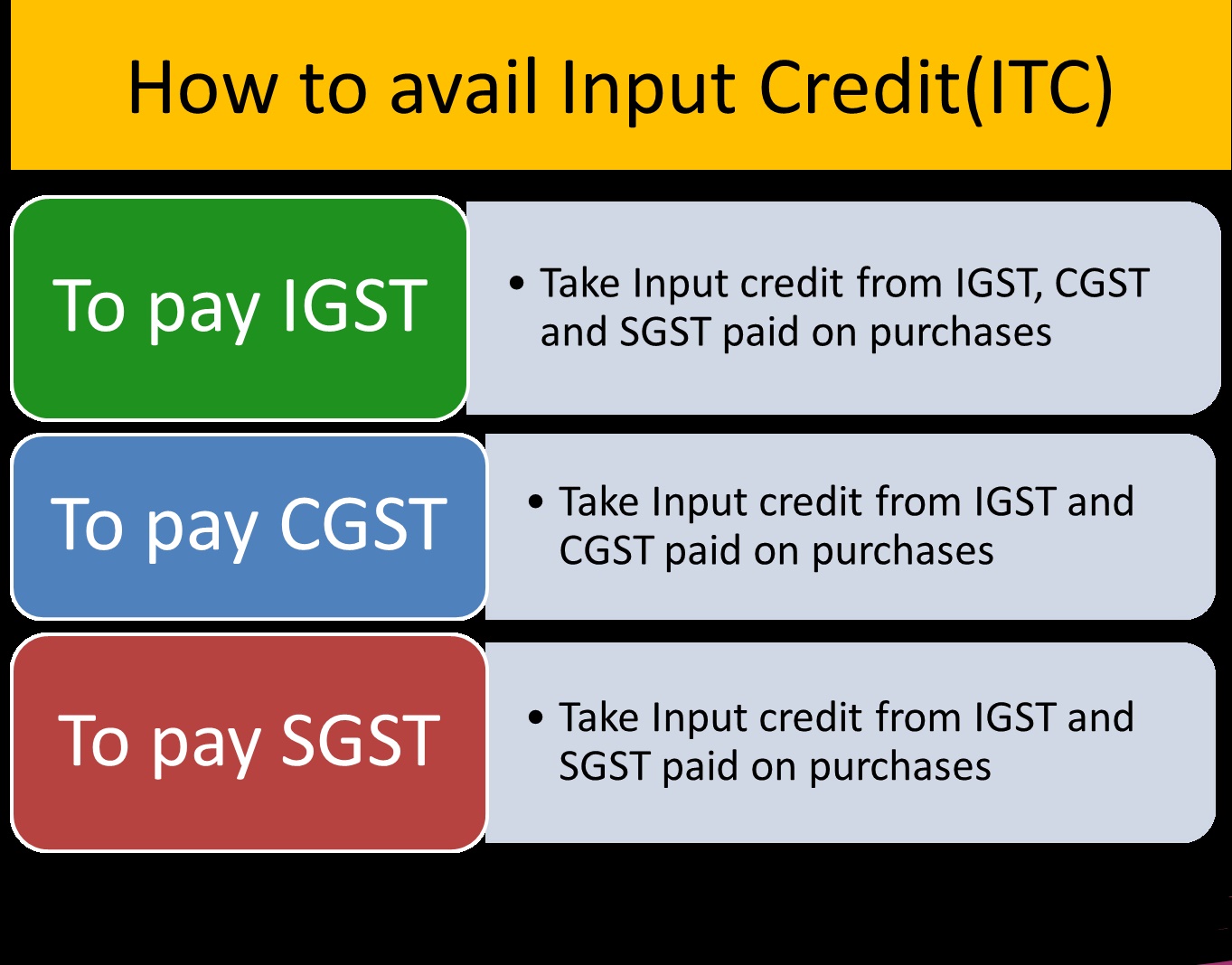

| ITC IN RESPECT OF | INITIAL UTILIZATION | BALANCE UTILIZATION |

| CGST | CGST | IGST |

| SGST/UTGST | SGST/ UTGST | IGST |

| IGST | IGST | CGST OR SGST/ UTGST, IN ANY PROPORTION. |

To avail the benefit of input credit, the taxpayer is required to furnish the amount of ITC, in their monthly GST returns which is provided in Form GSTR-3B.

A taxpayer can claim the amount of ITC on a provisional basis, by filing the form GSTR-3B, and the said provisional amount shall be allowed up to 20% of the eligible ITC, as mentioned in the auto-generated GSTR-2A return.

With effect from 9 October 2019, a taxpayer is allowed to claim only 20% of the eligible ITC as provided in GSTR-2A, as provisional ITC.

As discussed earlier, ITC can be claimed only where the goods or services availed have been made for making further taxable supplies, in the course or furtherance of business.

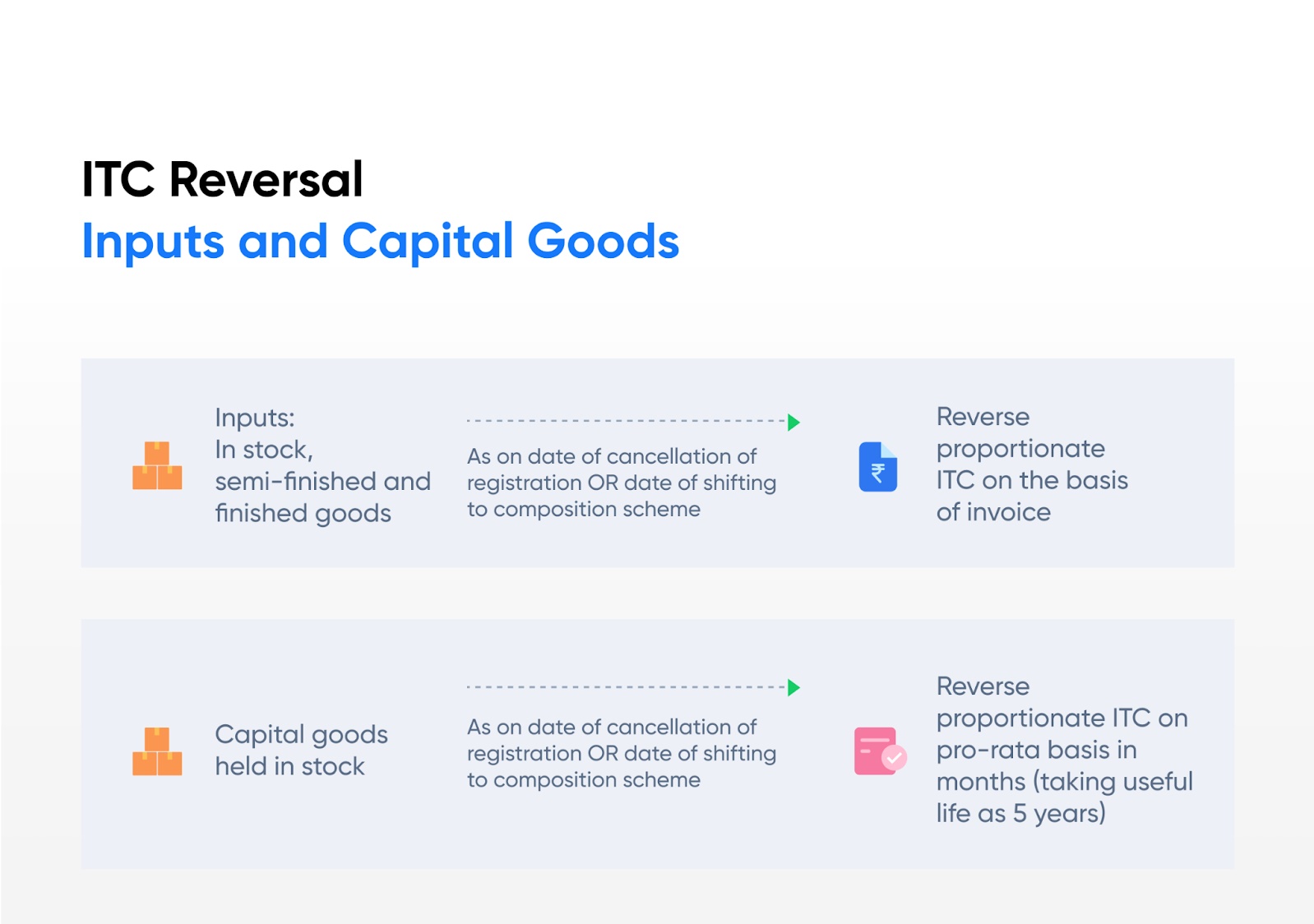

Thus, where ITC is availed in respect of supply of goods/services made for personal use, Exempt supplies, and supplies in respect of which ITC is specifically disallowed, the same be liable for reversal.

ITC shall also be reversed under the following situations –

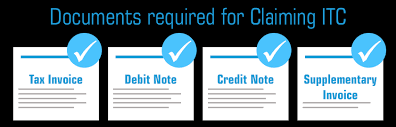

The taxpayer is required to be in receipt of the following documents, to avail the credit of ITC –

As per the GST Act, a taxpayer is eligible to claim ITC in respect of IGST and GST Compensation Cess paid on the import of goods. However, the same shall not be available in respect of Basic Customs Duty (BCD) paid.

For availing the ITC of IGST and GST Compensation Cess, the importer is required to provide their GST Registration number (GSTIN) in the Bill of Entry.

Once the same is provided, the Customs EDI system will inter-connect with the GST portal and the ITC will be validated.

It is commonly seen, that a principal manufacturer supplies goods, in the form of raw material, to their job workers, for further processing and manufacturing of final good.

In such a case, the principal shall claim the ITC in respect of goods supplied to job worker, provided the goods are sent to job worker, either from principal’s place of business, or is directly delivered by the supplier.

However, the ITC will be valid, provide such goods are received back by the principal within the prescribed time period, which is of 3 years in case of capital goods, and 1 year in case of other goods.

ISD can be termed as the head office (mostly) or a branch office or any other office, registered under the same PAN number.

Such ISDs collect the input tax credit on the purchases made on all India PAN basis and will then distribute the same to the respective recipients under different heads of GST like CGST, SGST/UTGST, IGST or Compensation cess.

| S. NO. | PARTICULARS | ALLOWED OR DISALLOWED UNDER GST |

| 1. | MOTOR VEHICLES & OTHER CONVEYANCE | ALLOWED, WHEN SUPPLIED IN THE NORMAL COURSE OF BUSINESS OR IS USED FOR THE FOLLOWING TAXABLE SERVICES – A. TRANSPORTATION OF PASSENGERS. B. TRANSPORTATION OF GOODS. C. IMPARTING TRAINING ON MOTOR DRIVING SKILLS |

| 2. | FOOD & BEVERAGES, OUTDOOR CATERING, BEAUTY TREATMENT, HEALTH SERVICES, COSMETIC & PLASTIC SURGERY | ALLOWED, PROVIDED THE SAME IS MADE FOR MAKING FURTHER TAXABLE SUPPLIES OR IS PROVIDED AS A PART OF COMPOSITE SUPPLY. |

| 3. | MEMBERSHIP OF CLUB OR FITNESS CENTRE OR HEALTH CENTRE | NOT ALLOWED |

| 4. | CAB RENTING SERVICE, HEALTH INSURANCE AND LIFE INSURANCE | ALLOWED, PROVIDED – A. MADE OBLIGATORY BY THE GOVERNMENT, FOR THE EMPLOYERS TO PROVIDE IT TO THEIR EMPLOYEES. B. THE SAME IS MADE FOR MAKING FURTHER TAXABLE SUPPLIES OR IS PROVIDED AS A PART OF COMPOSITE SUPPLY. |

| 5. | TRAVEL BENEFITS TO EMPLOYEES. EG: LEAVE TRAVEL ALLOWANCE | NOT ALLOWED |

| 6. | WORKS CONTRACT SERVICES, SUPPLIED IN RELATION TO THE CONSTRUCTION OF AN IMMOVABLE PROPERTY | ALLOWED, PROVIDED – 1. THE SAME IS SUPPLIED FOR THE CONSTRUCTION OF PLANT & MACHINERY. 2. IT IS SUPPLIED AS INPUT FOR ANOTHER WORKS CONTRACT SERVICE. |

| 7. | GOODS AND/OR SERVICES FOR CONSTRUCTION OF IMMOVABLE PROPERTY, WHETHER TO BE USED FOR PERSONAL OR BUSINESS USE. | NOT AVAILABLE |

| 8. | GOODS/ SERVICES ON WHICH GST HAS BEEN PAID UNDER THE COMPOSITION SCHEME | NOT AVAILABLE |

| 9. | GOODS/ SERVICES RECEIVED BY A NON-RESIDENT TAXABLE PERSON | ALLOWED, PROVIDED THE GOODS/SERVICES ARE IMPORTED BY THE NON-RESIDENT TAXABLE PERSON |

| 10. | GOODS/ SERVICES USED FOR PERSONAL CONSUMPTION | NOT AVAILABLE |

| 11. | GOODS WHICH ARE LOST/ STOLEN/ DESTROYED/ WRITTEN OFF/ DISPOSED OF BY GIFT/ FREE SAMPLE | NOT AVAILABLE |

| 12. | ANY TAX PAID DUE TO A. NON-PAYMENT OF TAX, ORB. SHORT PAYMENT OF TAX, ORC. EXCESSIVE REFUND | NOT AVAILABLE |

| 13. | ITC UTILISED OR AVAILED BY WAY OF A. FRAUD, OR B. WILL-FULL MISSTATEMENTS, ORC. SUPPRESSION OF FACTS | NOT AVAILABLE |

NOTE – ITC shall be available in respect of purchases made, provided the same is used to provide further taxable supply of goods/services or both in the course or furtherance of business.

MORE UPDATES;E-Commerces Platform under GST

MORE UPDATES:Composition levy scheme under GST

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

Exemption limit under Long-Term Capital Gains computation in 115BAC Vs Classic 112 Income tax Basic Exemption Limit Under Income Tax… Read More

Top Reasons Why Startups Prefer the Pvt. Ltd. Company structure Starting a business is exciting—but one of the first and… Read More

Complete Overview Legal Entity Identifier (LEI) A Legal Entity Identifier (LEI) is a 20‑digit unique alphanumeric code used to identify… Read More

No Interest Deduction Allowed Against Dividend Income (Budget 2026 Update) Investors in stocks and mutual funds, particularly those who use… Read More

CBDT’s NUDGE Initiative Driving Compliance (AI vs. Tax Evasion) Meaning of NUDGE: NUDGE stands for Non-Intrusive Use of Data to… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}