Page Contents

NBFC is totally governing & regulated by the Reserve Bank of India Act 1934. Non-Banking Financial Company facilitates banking-related services like investment services, financial services, risk pooling & contractual savings.

NBFCs (Non-banking financial Co) are financial companies that provide banking services but do not hold a banking license.

They are not permitted to take deposits from the public. But all activities of these institutions are still subject to banking rules.

NBFCs give most types of banking services, such as credit facilities, TFCs (Term Finance Certificate), loans, money market trading, private education funding, retirement planning, stock, share underwriting, and other obligations.

These institutions also provide wealth management, such as portfolios managing of stocks & shares, discounting services. e.g. advice on mergers and acquisitions activities and instruments discounting.

A Non-Banking Financial Company cannot accept demand deposits;

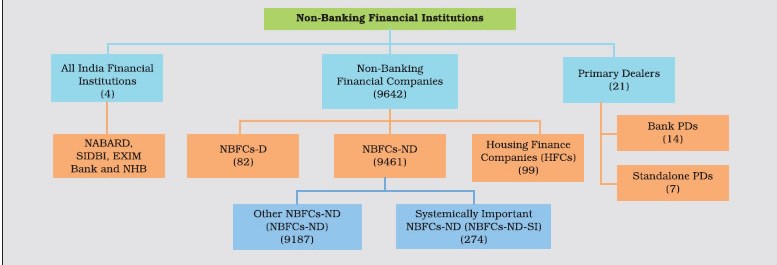

The No of Non-Banking Financial Company has increased considerably over the last few years, with venture capital companies, retailers, and industrial companies entering the lending business.

Non-banking institutions also frequently encourage investment in prepare feasibility studies, industry studies or market studies for companies & also in real estate.

Nevertheless, they are generally not allowed to take deposits from the general public & have to find other ways of financing their operations, such as the issuing of debt securities.

RBI issued draft directions for the prohibition of abuse in the fixed income markets, stating, among other things, that market participants, either acting independently or in collusion, shall not undertake any action with the intention to manipulate the process of calculation of a benchmark rate or reference rate.

The Reserve Bank of India has issued a notification regarding the Co-origination of loans by Banks and NBFCs for lending to the priority sector.

In case you interested in exploring the financial market in India?

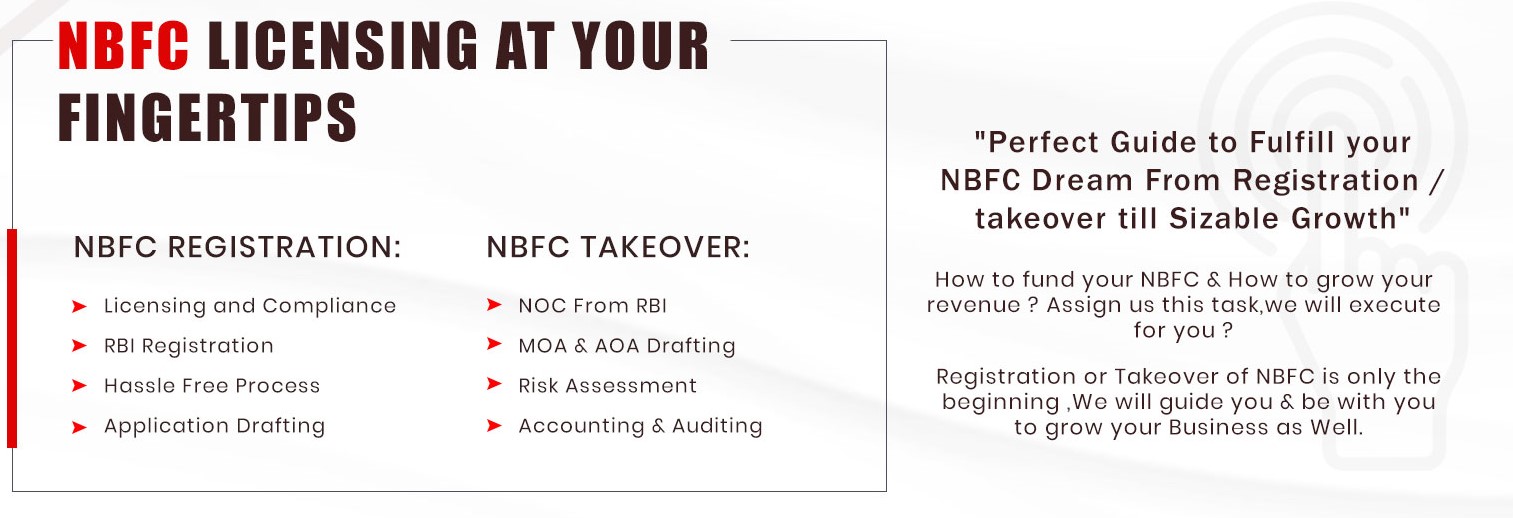

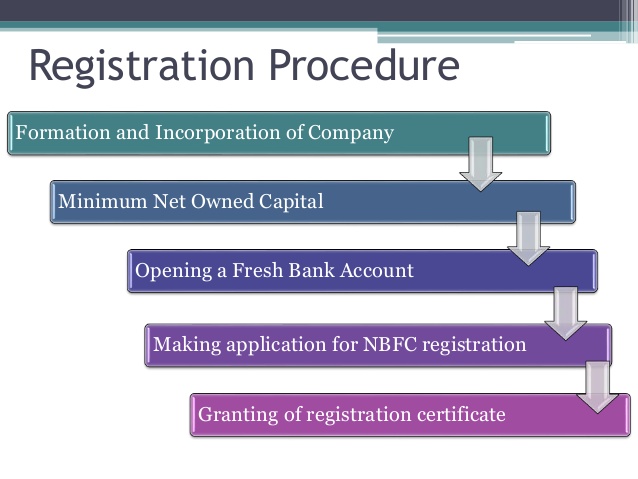

Basic Steps for filling the For Non-Banking Financial Company (NBFC) Registration: Application Process & Requirement for NBFC registration

The applicant must submit an application to the RBI. Once logged in to the secure site of the Reserve Bank, click on one of the excel sheets and download the application form.

Fill in the accurate name of the Regional Office (RO) in the “C-8” field of Annexure-I Identification Particulars in the given Excel form.

Related links are there:

Payment of Scurity to MSME according to LAW

Micro Small and Medium Enterprises

Top Taxation Relaxation to MSMS

Cheer for SMEs and manufactures

Once the form has been filed, the company will receive a unique Company Application Number against the Company Registration Application that has been filed website.

The applicant must obtain a printout and must submit the same form, including the Company Application Reference Number, in addition to the basic documents to the Regional Office of the Reserve Bank of India concerned.

It must be noted that Necessary documentation should also be attached to the RBI website (COSMOS).

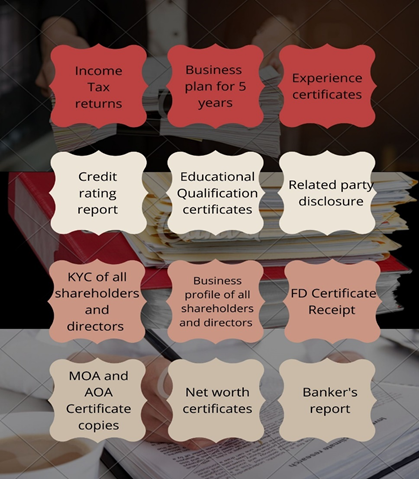

Application must complained the following documentation:

If the Reserve Bank has any queries regarding the NBFC application submitted, it may issue a notice.

One must be both quick and successful in replying to the query otherwise there is a possibility that the request will be rejected.

Contact the most competent team at www.carajput.com for the best technical support and inquiry. Acknowledge the problem-free process and get the right support in all financial aspects.

Allowances & Perquisites under Income‑tax Rules, 2026 for OLD tax regime The Income‑Tax Rules, 2026, notified by the Central Board… Read More

GST Implications on Sale of Old Vehicles vis‑à‑vis Sale of Other Used Capital Goods Some Tamil Nadu AAR judgments that… Read More

Major Changes Proposed & Impact of Corporate Laws (Amendment) Bill, 2026 A major reform initiative, the Corporate Laws (Amendment) Bill,… Read More

Product brand value with artificial intelligence video editing tool. What’s an artificial intelligence video editing tool? An artificial intelligence video… Read More

How to Secure Ideal NRI FD Rates Online in 2026 Fixed Deposits (FDs) have been a popular investment option for… Read More

LIST OF GOODS FOR WHICH E‑WAY BILL IS NOT REQUIRED Goods Exempt from E-Way Bill (Rule 138(14) – GST) GST‑exempt… Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}